Issue #6, Volume #1

| In today’s Journal we take on a seemingly impossible task. How can we improve the performance of Harry Browne’s Permanent Portfolio by 3x, without increasing the risk of this legendarily low-beta approach to investing? (See Wednesday’s Daily Journal for background on the Permanent Portfolio.) |

Three Things You Need To Know Now:

1. We’re at risk of seeing more inflation, despite the weakening economy. Following Wednesday’s big move lower (50 basis points) in the Fed Funds Target Rate, speculative stocks rallied while U.S. long-dated Treasury bonds fell in price, as long-term interest rates moved higher. The iShares 20 Year+ Treasury Bond ETF (TLT), which tracks the price of long-dated Treasury bonds, fell from $101.50 at the time of the announcement to $98 over the next 24 hours, which is a huge move for bond prices, as the entire yield curve (even the two-year rates!) increased as the yield curve steepened sharply. Normally, when the economy is slowing, defaults and unemployment are rising, investors tend to sell stocks and move into bonds for safety. Likewise, when the Fed begins cutting interest rates, bond prices usually rally and rates fall. But right now, seeing that the government has no ability to regulate its spending (growing the national debt by $1 trillion every 100 days!), investors are deciding that corporations (which can increase prices with inflation) are a safer bet than our bankrupt government’s bonds. This is a sea-change in investor behavior… and it could be the beginning of a massive inflation-driven bubble in equities. As we wrote in yesterday’s The Big Secret on Wall Street, we could see a “melt-up” in stock prices instead of a normal recession and bear market.

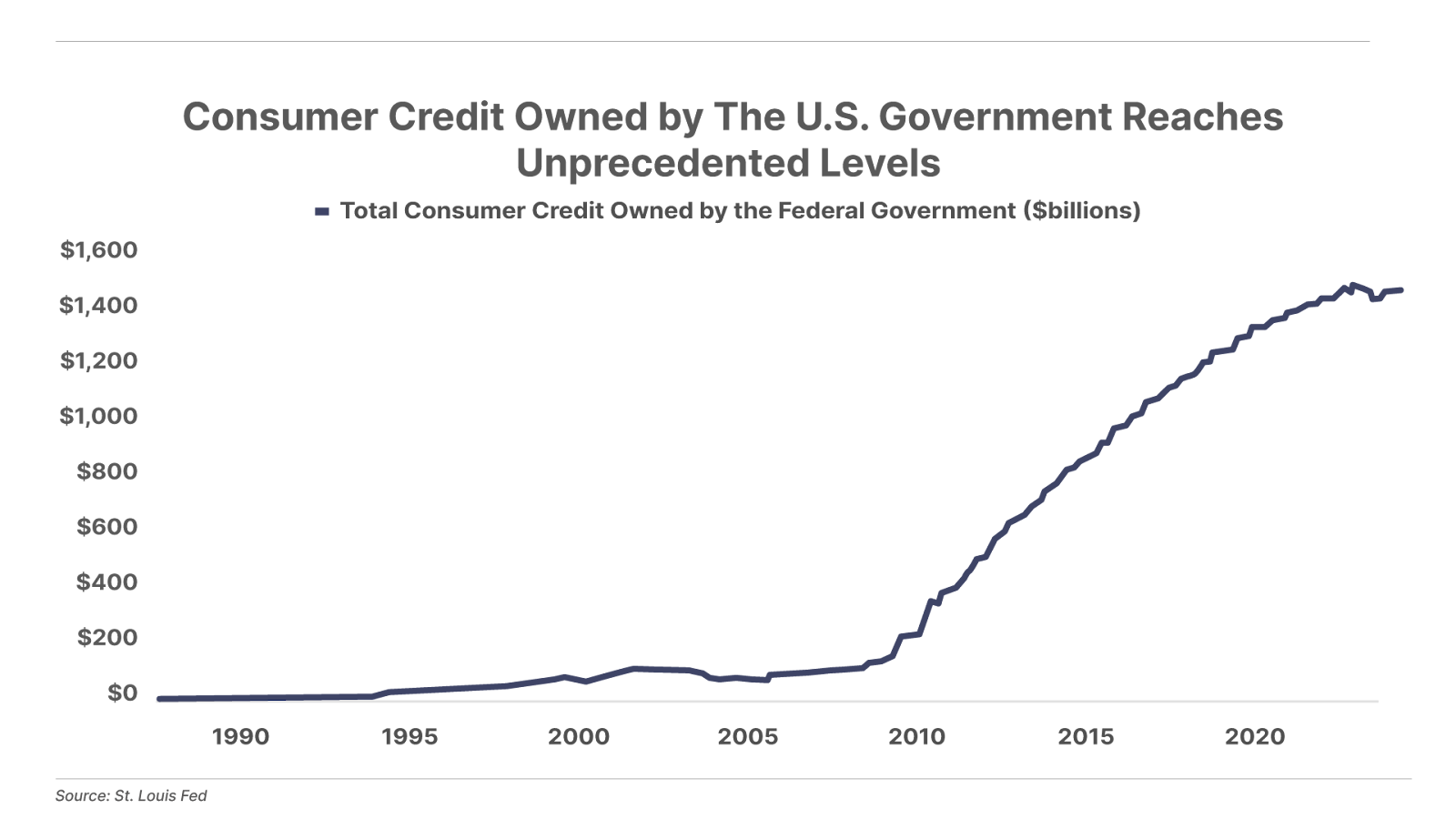

2. This kind of market action isn’t actually good news, even though most investors will probably cheer. We now have an entire economic system that’s based on constantly expanding money and credit. It’s an economic Lake Wobegon, where every capital program (and foreign war) is better than average. But in the real world, most of our government’s huge expenditures lead to ashes, like “lending” $1.5 trillion to college students to earn worthless degrees (see graph below). Or loaning hundreds of billions of dollars to “ninja” home buyers – an acronym for borrowers with no income, no job, and no assets. Or spending $2.3 trillion (!) financing a 20-year losing war in Afghanistan, “the graveyard of empires”: a stone-age country with 37% literacy and a history of tribal violence. When these enormous “mal-investments” occur, rather than seeing the people responsible for them suffer through default, bankruptcy, and infamy, we continue to just print more money to bail them out. Doing so devalues the savings and wages of “Main Street” Americans, while enriching an elite group of bankers and politicians – the very people most responsible for these enormously wasteful bad investments. This process will destroy the middle class. It will lead to a collapse of our nation’s values and norms. And it will lead, eventually, to a monetary collapse.

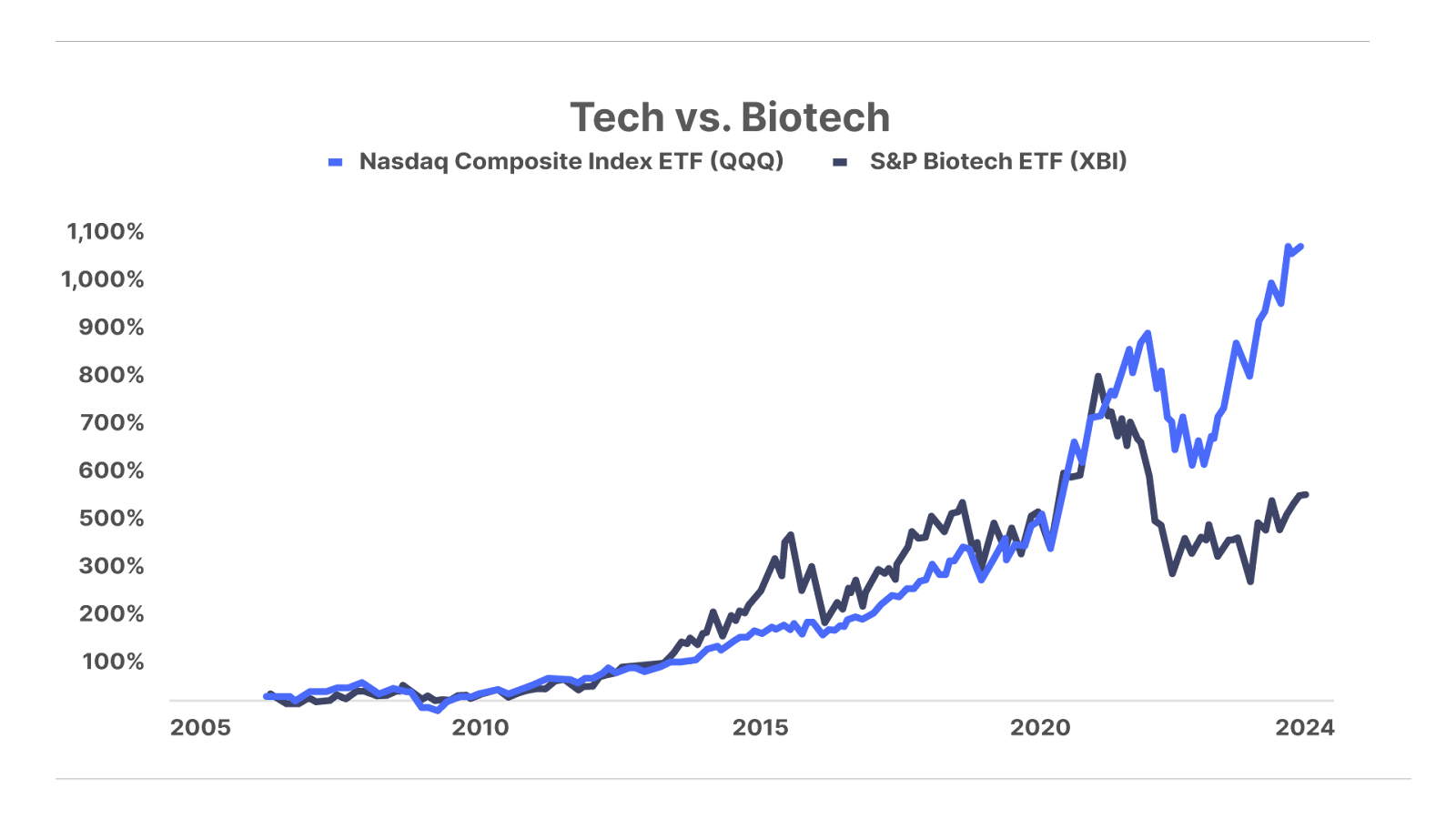

3. The coming biotech boom. As we’ve been saying since the beginning of this year (and as the chart below shows), there’s a huge gap between the market performance of tech stocks (represented by the Nasdaq Composite Index below) and biotech stocks (the S&P Biotech ETF). Ironically, it’s in biotech where new artificial-intelligence (“AI”) technologies promise the biggest potential gains. We believe the Fed’s 50-basis-point rate cut sets the stage for a massive rally in biotech stocks. If you haven’t yet seen Erez Kalir’s research in our Biotech Frontiers advisory, know that his recommendations this year are up 19.4% on average, with a 75% win rate. It’s a very safe bet that biotech shares will end up showing our best returns this year.

One more thing…

This morning, Microsoft (MSFT) announced that it is partnering with Constellation Energy (CEG), which will spend $1.6 billion to restart the Three Mile Island nuclear-power plant in Harrisburg, Pennsylvania. The increased amount of energy we’re going to need over the next five years to sustain the AI build-out is staggering. As subscribers know, we’ve been way ahead in our reporting on the growth in nuclear-power demand, with our top nuclear recommendation BWX Technologies (NYSE: BWXT) up 72% (!) in less than two years.

A Deeper Dive Into Our Portfolio Strategy

In Wednesday’s Daily Journal, I told you about my old friend Harry Browne and his brilliant idea for building portfolios that can win in any economic environment. Harry’s idea was deceptively simple. He suggested a four-part portfolio: 25% in stocks, 25% in bonds, 25% in gold, and 25% in cash.

Ray Dalio took these ideas and built Bridgewater Associates, creating the world’s biggest hedge fund. Most people don’t understand how Bridgewater has delivered such outstanding returns for so many years with its Pure Alpha fund.

Here’s the secret.

Dalio figured that because Harry’s portfolio had much less volatility than the S&P 500 (known in financial jargon as beta), it could be leveraged safely to produce market-beating returns (known as alpha).

So, Dalio built two funds. His All Weather fund used virtually the same allocations as Harry’s Permanent Portfolio, without any leverage. All Weather allocates 30% to stocks, 40% to bonds, 15% to intermediate duration fixed income, 7.5% to commodities, and 7.5% to gold. We know the results, roughly, from All Weather, because there’s a mutual fund, The Permanent Portfolio (PRPFX), that’s also followed Harry’s basic allocation since 1989. Over the past 10 years, it has produced average annual returns of 6.5%, for a total return of 90%. And it’s done so with extremely low volatility, just a little more than half the S&P 500’s volatility.

(Finance nerds like to use complex Greek jargon to represent pretty simple math concepts. So, for volatility, aka “beta,” they compare a portfolio to the S&P 500’s volatility. So, a “beta” of 1.0 means the fund has the same volatility as the S&P 500. A beta of 2.0 means it has double the volatility. The Permanent Portfolio has a beta of 0.60 – a little more than half the volatility of the S&P 500.)

When you measure the return of the strategy relative to its volatility, you end up with what’s called a Sharpe Ratio. The Sharpe Ratio measures returns per unit of volatility. The Permanent Portfolio, because of its very low beta (0.60), means you’re getting 1.67 units of return per unit of risk. That’s a very efficient way of making money in the markets. Anything above 1.0 is a very good result – and is very rare.

Dalio took this supersafe portfolio and applied leverage to it, to move the beta (the volatility) up to the market’s level. If you know that Harry’s portfolio has a beta of 0.6, then if you apply leverage of, say, 50%, you’ll increase the volatility by 50%. You’ll then have a fund with a beta of 0.9 – still less volatile than the market. But because the portfolio has such a high Sharpe Ratio, you’ll see the annualized returns increase to far above the market return. Leveraged 50%, Harry’s portfolio will earn almost 2x the market’s return! And that’s how Dalio built what he calls Pure Alpha, which is the best selling-hedge fund of all time.

But… I’m about to show you how to do even better.

Dalio produced market-beating results, but only by increasing volatility. I’m going to show you how to increase Harry’s returns by 3x, without increasing your risk, at all, and without using any leverage.

And, here’s the irony. You can absolutely build this portfolio. It only requires buying four low-cost ETFs. This is an All Weather approach to investing that will beat the markets, that will protect you from any market outcome, and that doesn’t require any trading whatsoever. In other words, this is the ultimate investment solution.

And watch what happens. No one will do this. Not. A. Single. Person. “Horse, meet water,” as I like to say.

How I’ll Do It

There are two ways to create alpha (market beating, risk-adjusted returns). The first way, as Harry Browne and Ray Dalio have proved, is by building supersafe portfolios and applying leverage. But the other way is simply finding investment vehicles that have both low beta (low volatility) and economics that are inherently more efficient than the market. In other words, the alpha of the portfolio I’m going to show you how to build isn’t created by portfolio leverage, it’s created by the operating leverage of the businesses inside the portfolio.

And there’s a flaw inherent in both Harry and Dalio’s low-risk portfolios: they have way too much allocated to government bonds, an asset class that’s increasingly plagued by inflation. Combined, fixed income and cash makes up 50% of the allocation in the Permanent Portfolio and 55% in Dalio’s All Weather. Below is a five-year chart of the kinds of bonds these funds have big exposure to. This is the long-dated U.S. Treasury ETF (TLT), which shows a decline from $170 four years ago to about $80 at the end of 2023. When the “safe” part of your portfolio declines by more than 50% over four years, there’s a problem.

My plan to improve on the performance of Harry’s Permanent Portfolio and Dalio’s All Weather portfolios is:

- Move the 25% equity allocation into the kinds of businesses that produce superior results over time – well-established, capital efficient businesses with consistent revenue growth. These are the businesses that you’ve seen us recommend to investors for decades. You’ll find these stocks in our current portfolio. Look for the operating businesses (not the fixed income or the ETFs) that we have ranked as #1 or #2.

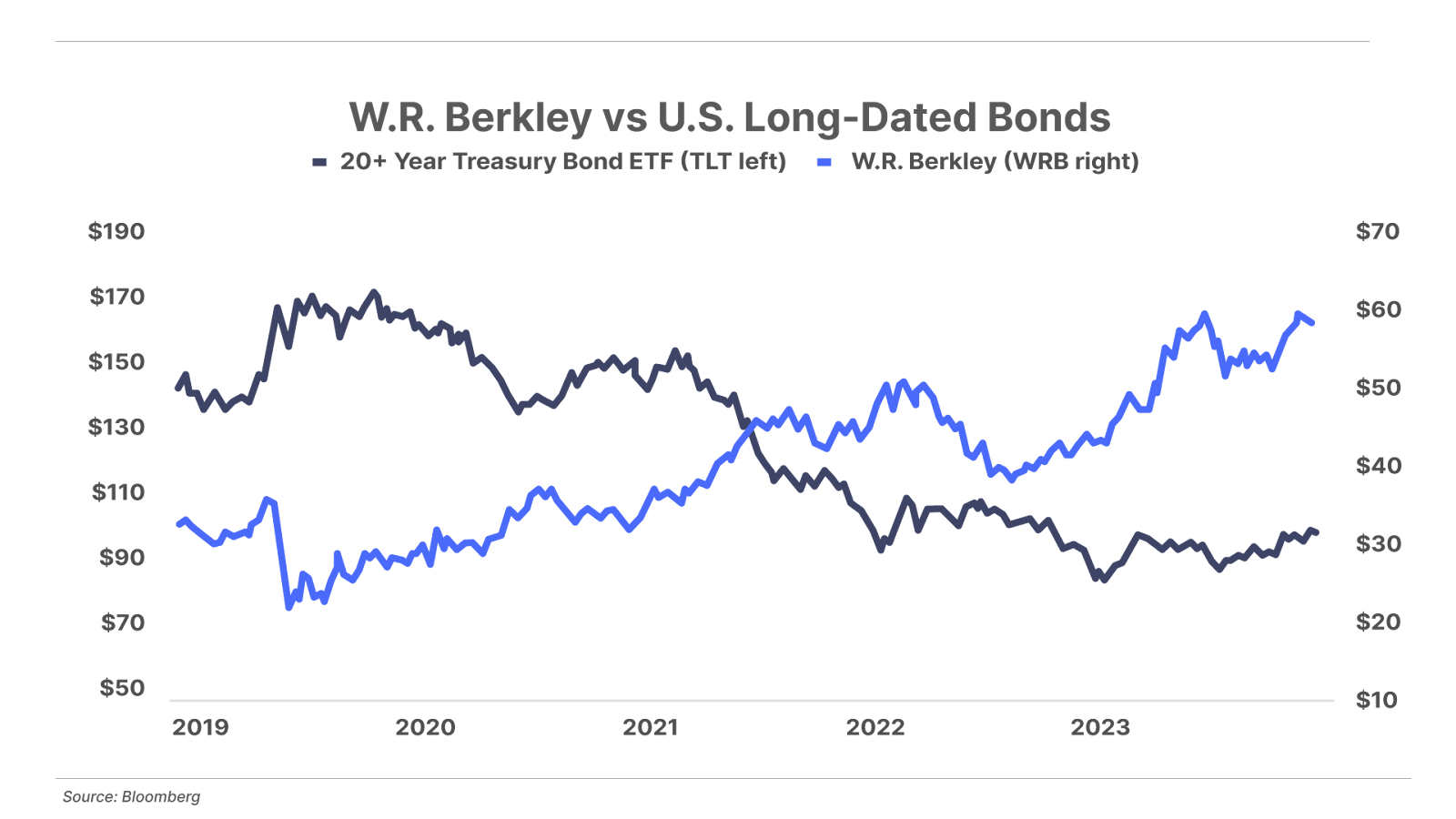

- Replace the 25% bond portion of the portfolio with our high-quality property and casualty (P&C) insurance companies. These companies are, essentially, giant piles of bonds, fed by customer premium payments, that are actively managed by pros and generate additional returns through underwriting. These firms produce incredible risk-adjusted returns and offer high-quality bond management, for free. While the share prices of these firms will not be quite as stable as actual fixed income, they are much less volatile than most stocks because of the size of their bond portfolios. In fact, I would argue that through the active management of their bond portfolios, it’s safer to own insurance companies than to own bonds directly. For example, when William Berkley saw what the government was doing during COVID, he got his insurance firm, W.R. Berkley (NYSE: WRB), out of long-dated bonds and into short-term notes, avoiding huge losses when bonds collapsed in 2022. You can see the impact of that active bond management in the chart below. As you’d expect, Berkley (in blue) was closely correlated with the 20+ Year Treasury Bond ETF, but when COVID hit, Berkley suffered a short, sharp drop (along with virtually every other stock) but then recovered quickly and has outperformed the bonds massively. (I recently wrote about P&C companies in the Daily Journal.)

- Hold gold and Bitcoin, not only gold. Today, that’s easier than ever thanks to both gold and Bitcoin ETFs.

- Have a large cash position. Where I agree with Harry most strongly is having a large cash portion in the fund. Yes, it will be a drag on performance, but having cash on hand when there’s a market panic will pay huge dividends over time, enabling you to buy high-quality companies at bargain prices. I’d recommend actively managing the cash portion of the fund, using a variety of valuation metrics to determine if the market (overall) is cheap, fairly priced, or overvalued (like I believe it is today). You’d adjust your cash allocation to 25% when stocks are really expensive and take that down to 15% when they’re priced normally and then down to 5% when there’s a crisis, or, like in late March 2020 (at the COVID bottom), when they’re at decade lows.

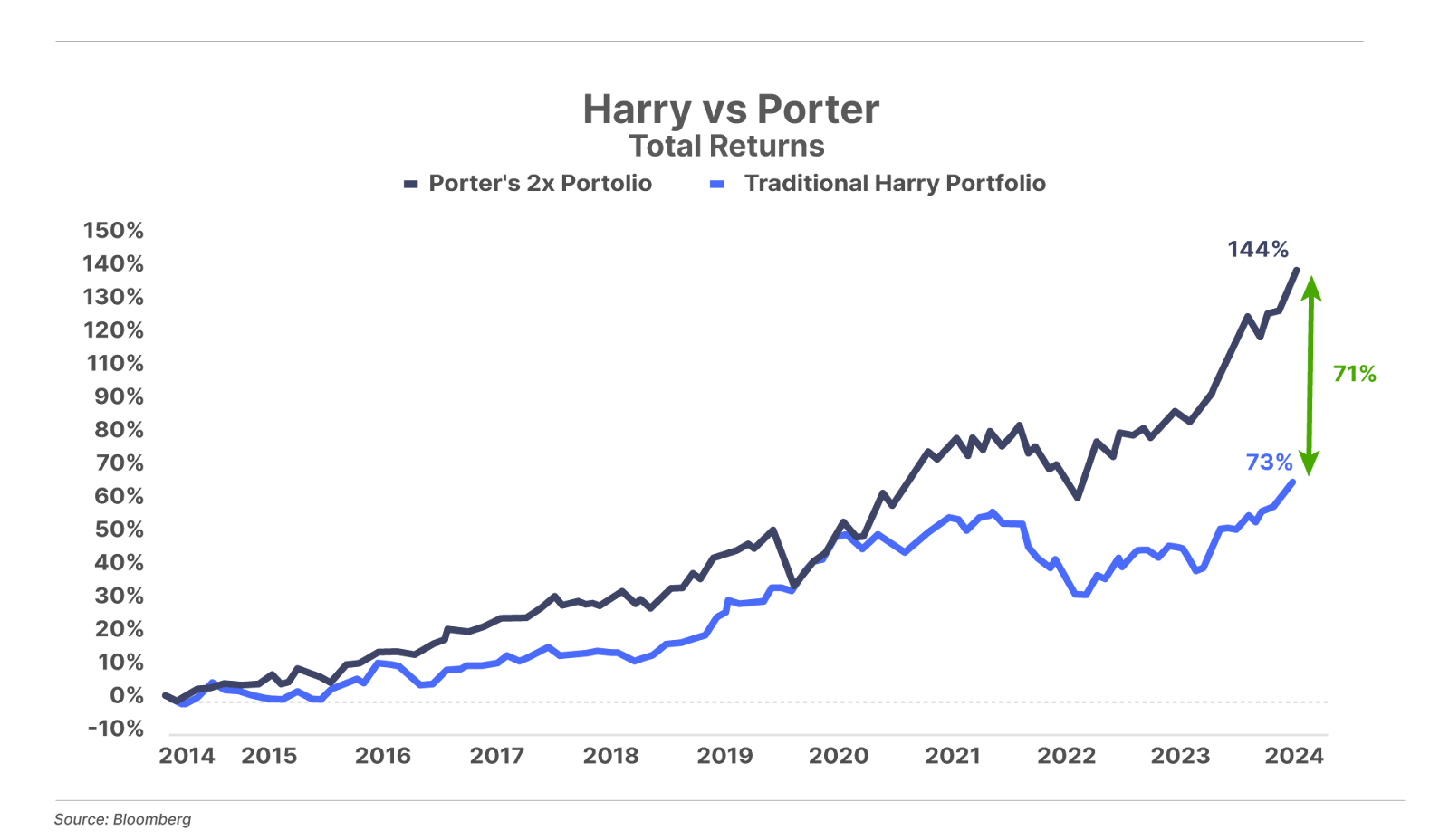

How My Strategy Stacks Up to Harry’s

If you want to build Harry’s traditional portfolio, it’s very easy to do.

Your 25% equity position would be the S&P 500 ETF (SPY). Your 25% bond allocation would be to the U.S. long-dated Treasury bond ETF (TLT). Your 25% gold allocation would go into the gold ETF (GLD). And your 25% cash allocation would be to the U.S. short-term note ETF (SHY).

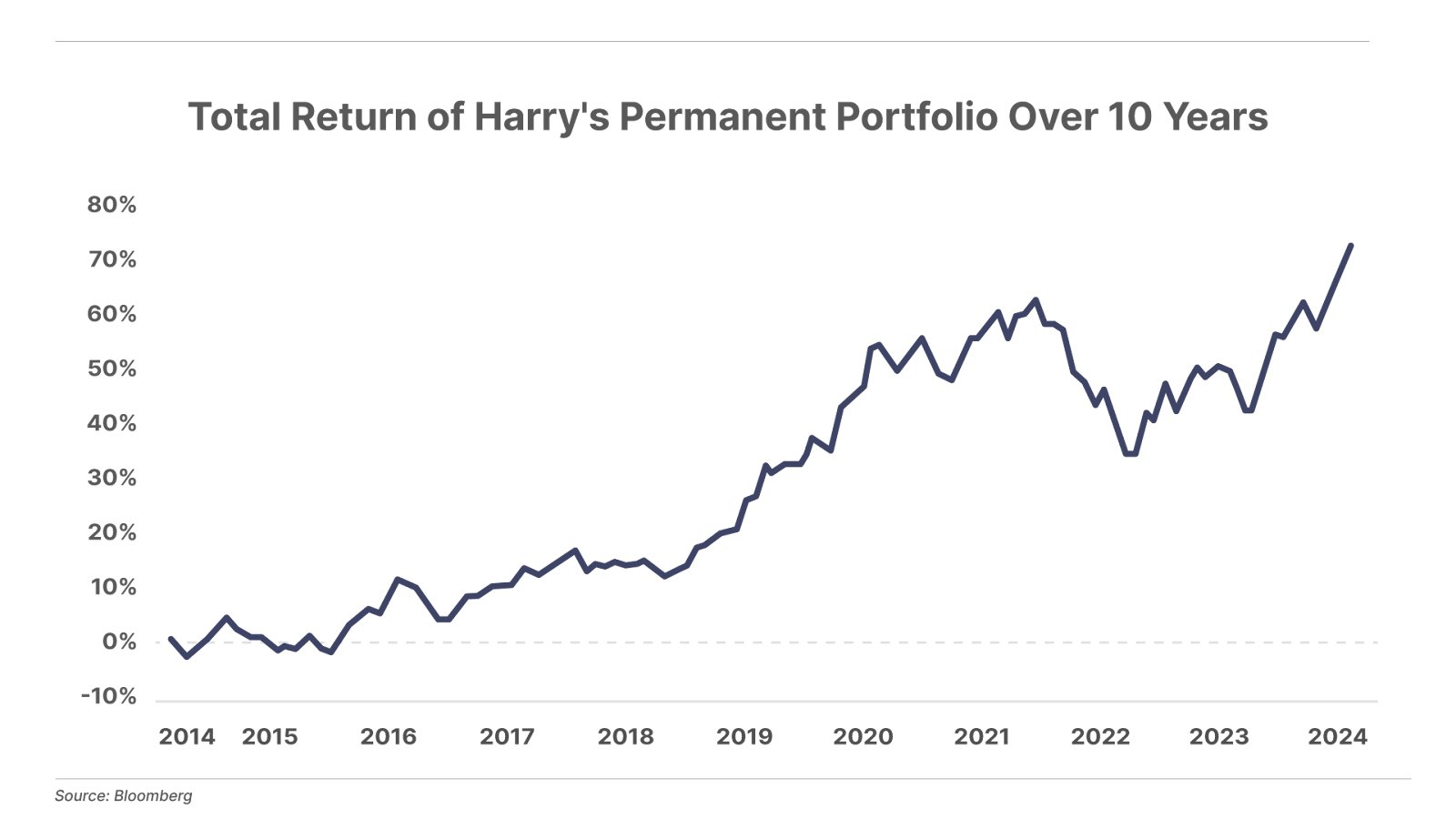

Here’s what that performance looks like over the last decade:

To build my Permanent Portfolio, instead of buying the S&P 500, pick an actively managed ETF that selects for quality businesses with growth, like iShares MSCI USA Quality Factor ETF (QUAL). This ETF uses an algorithmic approach to hold the companies that have both the most amount of growth and the highest-quality earnings (the most capital efficient). Its largest holdings today are: NVIDIA (NVDA), Apple (AAPL), Microsoft (MSFT), Eli Lilly (LLY), Visa (V), Mastercard (MA), Meta (META), UnitedHealth (UNH), Costco Wholesale (COST), and Johnson & Johnson (JNJ).

Next, instead of buying a bond ETF, you’d buy an ETF that owns a basket of high-quality P&C insurance companies, like the Invesco KBW Property & Casualty Insurance ETF (KBWP). This fund simply owns the biggest P&C firms. I’m not a big fan of many of the companies that it owns, but it’s the only ETF that’s focused strictly on P&C insurance. (For subscribers, we can add a lot of alpha here by picking only the best underwriters.)

Next, instead of buying only gold, you’d split the allocation between a gold ETF (GLD) and Bitcoin (BTC-USD), putting 12.5% of the portfolio into each. Today, buying Bitcoin has never been easier because there are several ETFs to choose from. The one with the lowest fees (0.19%) is the Franklin Templeton Digital Holdings Trust (EZBC).

And, finally, for the cash portion of the fund (25%), stick with the U.S. short-term note ETF (SHY).

If you bought that exact portfolio 10 years ago, you would have generated 9.4% average annual returns – that’s nearly 2x returns – with less volatility than the Permanent Portfolio. The Porter Permanent Portfolio has a beta of 0.51 – it’s less than half as volatile as the stock market, producing a Sharpe Ratio of 2.46. Your maximum drawdown, during the COVID panic, would have been -21.8%.

Those are amazing results – and keep in mind, that includes holding 25% cash the entire time. The formula is simple: invest in great businesses, use P&C insurance to manage your bond allocation, buy both gold and Bitcoin, and hold plenty of cash.

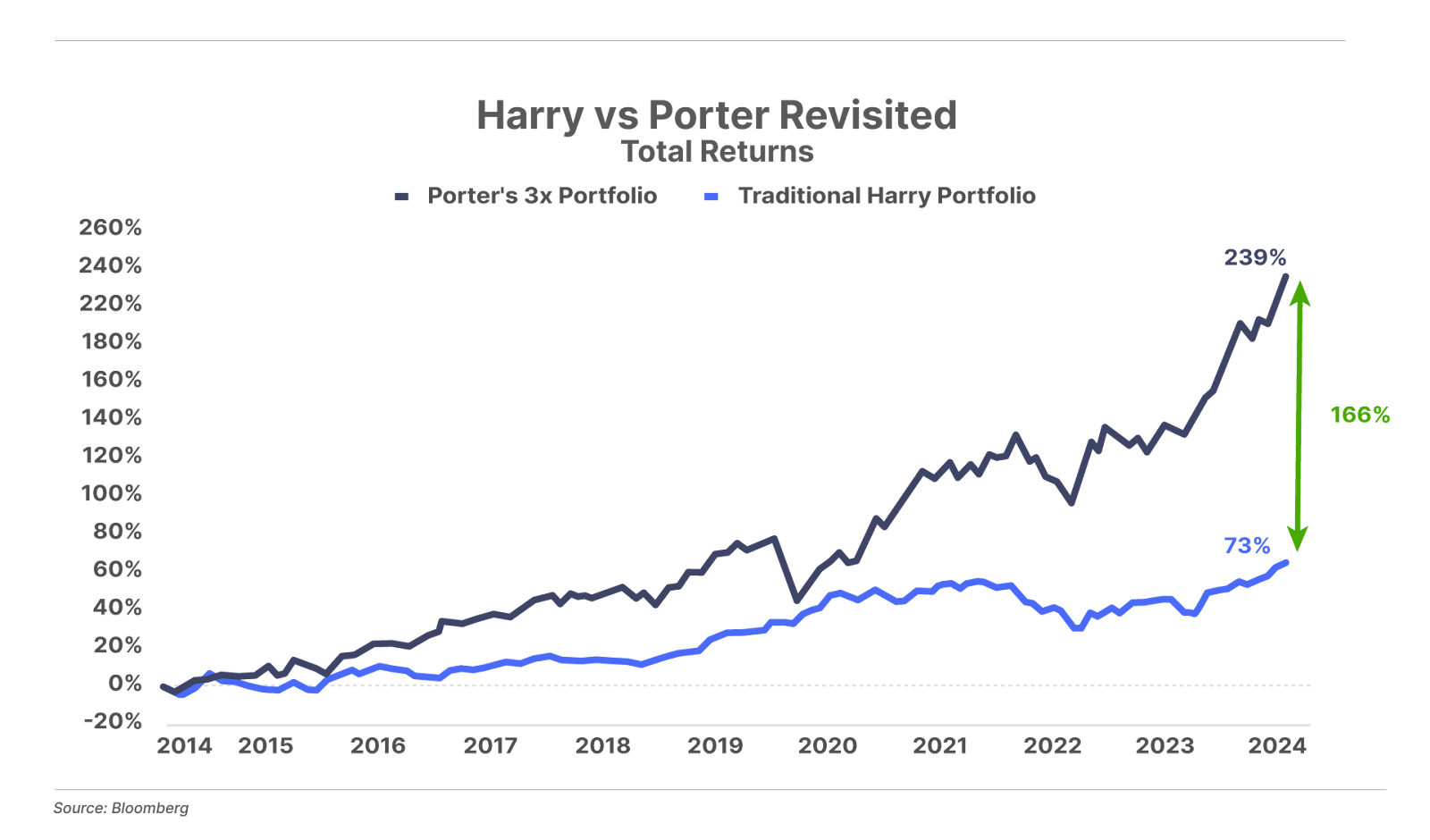

But, wait, didn’t I promise that I was going to build a portfolio that’s 3x better than Harry’s? Sure, this is really good… but it’s only a little better than 2x Harry’s results. Looks like I’ve failed.

Well, not really. If you can stand a little more volatility, you could easily leverage the fund I’ve built here and produce results that are 20% or more annually with volatility that’s still less than the stock market’s.

Or, you can do something even simpler. Just get rid of the cash in the portfolio and replace it with more bonds, but use bond portfolios that are managed by insurance firms. If you replace the cash allocation (25% to SHY) with more allocation to the insurance firms (move KBWP to 50%), you end up with an incredible portfolio. Sure, you’re fully invested, so you’ll have to come up with more cash to add to the portfolio during market panics, but the dynamics of this portfolio are impossible to beat. With an allocation of 50% KBWP (insurance) / 25% QUAL (stocks) / 25% GLD and Bitcoin, over the last 10 years you would have seen average annual returns of 13% (total return 239%), with 0.71 beta and a Sharpe Ratio of 2.83.

That is, of course, exactly how Warren Buffett ran Berkshire Hathaway in its heyday: high-quality stocks plus P&C insurance. And, not surprisingly, this portfolio delivers Buffett-like returns: 13% a year with low volatility.

And… here’s the best part. For our subscribers, we can add even more alpha by picking only the best P&C stocks, buying only the highest-quality operating companies (which is what we do in The Big Secret on Wall Street), and by actively managing the amount of cash we’re holding. We can also add a lot of “smart” leverage, by buying distressed debt at the right time in the market cycle.

I’ll be unveiling my version of this portfolio (with allocation to individual stocks) at our upcoming conference on Wednesday, September 25.

Okay, go ahead: tell me exactly how I’ve got this all wrong and why this kind of investing isn’t going to work: [email protected]

Good investing,

Porter Stansberry

Stevenson, MD

P.S. In this week’s Porter & Co. Spotlight, we brought you a second piece by Tom Dyson, who Porter calls “the greatest investor you’ve never heard of.” In it, Tom talks about how to best prepare yourself for what he believes will be an upcoming cascade of crises… and he passes on a way to insulate your portfolio from weakness in the U.S. dollar. Read more here.