Editor’s Note: On Tuesdays we turn the spotlight outside of Porter & Co. to bring you exclusive access to the research, the thinking, and the investment ideas of the analysts Porter follows personally.

Yesterday, we introduced you to our friend Joel Litman, who we recently spent time traveling through Croatia.

As we wrote about that trip:

Over cigars and a glass of Rakija, Joel told us all about an energy company, and although it had already doubled this year, he said:

‘I know it’s up massively already but I think it’s likely to double again.’

It’s only been a month but lo and behold, Joel was right – the stock is already up more than 60% since our trip.”

That company, Bloom Energy, is the focus of today’s Spotlight.

Below is Joel’s analysis of the energy company that he believes could become the backbone of the artificial intelligence ecosystem – providing clean, reliable, and easy-to-scale energy for the insatiable demands of AI.

Enjoy.

P.S. Joel has also extended Porter & Co. readers the opportunity to beta-test his latest system.

It’s a new approach that he says can help isolate potential 100% winners with startling accuracy. It’s already directly linked to the hundreds of stocks that have doubled in just the last six months alone.

And Porter & Co. readers can beta-test it here.

The ‘Mars Oxygen Box’ Is Powering America’s Data Centers

KR Sridhar believed his small electrical device could save stranded astronauts.

At the center of the box, he had placed two thin ceramic tiles, each coated with special ink. When fed with electricity and Martian ice, the box came alive… turning water into oxygen and hydrogen.

In theory, a few of these boxes could fill an enclosed habitat (like a biosphere) with breathable air and produce fuel for the trip home.

Sridhar developed this device at the University of Arizona back in the 1990s. And NASA engineers called it a breakthrough.

After presenting his invention to the senior staff at the Ames Research Center in Moffett Field, California, NASA earmarked it for the next phase of testing.

So Sridhar’s “Mars Oxygen Box” seemed destined to reach the planet’s life-support quarters. These spaces would have the optimal mix of gases, and be pressurized and air-conditioned to accommodate human life…

But then the Mars Exploration Program was scrapped due to ballooning costs and significant delays. NASA had to shift priorities back to low-Earth orbit. So Sridhar was left with a brilliant solution and nowhere to put it.

That’s when he had an epiphany… Instead of feeding his device electricity and water to produce oxygen and hydrogen, he would supply it oxygen and fuel to generate electricity.

Sridhar shut himself in his lab and began reengineering the Mars Oxygen Box… He ripped out expensive platinum catalysts and replaced them with cheap metal alloys. Sridhar also experimented with sand-based ceramics that could be printed like tiles. These methods would ensure a less expensive device that was easier to produce.

When he hooked up the box to natural gas and opened the air intake, it hummed softly and generated clean, steady electricity.

Sridhar had created a fuel cell that could produce power with no moving parts, combustion, or the grit and smoke of a diesel generator. Stack enough of them together, and you could power an office building, or as he would soon find out, a data center.

By 2001, Sridhar had realized that the modified device could revolutionize the energy industry. But he needed help to bring it to market… So Sridhar flew to Silicon Valley and met with venture capitalist John Doerr, the man who had backed Amazon (AMZN) and Google.

He only brought the ceramic tiles and a few drawings with him. After laying everything out and explaining the science behind his fuel cell, Sridhar asked Doerr for more than $100 million.

Understandably, Doerr was skeptical… that is, until Sridhar lit up a lightbulb using his ceramic tiles. Within minutes, Doerr was sold. The original Mars Oxygen Box became the foundation for one of the most ambitious energy startups of the 21st century.

By 2008, Sridhar’s boxes were stacked into gleaming, refrigerator-sized servers. One such server could power 100 homes or a 30,000-square-foot office running on natural gas.

They also appeared behind corporate campuses and warehouses. Google installed four of them at one of its data centers. And FedEx (FDX) used the devices to power its Oakland hub. Soon, Coca-Cola (KO), Bank of America (BAC), and eBay (EBAY) joined the customer list.

Today, Sridhar is using his Mars Oxygen Box technology to feed natural gas to one of the largest gas guzzlers around…

You see, artificial-intelligence (“AI”) and cloud-computing technologies are pushing data centers into overdrive. And demand for power is skyrocketing. Tech companies need scalable, on-site solutions that are clean, dependable, and relatively safe from blackouts.

That’s where Sridhar’s venture, now called Bloom Energy (NYSE: BE), comes in. What started out as a lifeline for Mars astronauts has become a boon for modern technology.

Now, we recognize that Bloom’s stock has stayed largely flat for years. But that will soon change…

The company is ramping up production capacity and securing deals at a record pace. Not to mention, we’re nowhere near peak energy demand. That means Bloom is poised to dominate the power industry in the coming years.

Let’s dig in…

AI Can’t Wait for the Nuclear Renaissance

In a world obsessed with AI, it’s easy to forget what drives this entire tech revolution – electricity.

Every ChatGPT query, generated image, and AI model trained on billions of data points runs on massive servers. And they consume staggering amounts of energy.

Traditional data centers (which have a few hundred servers) used 4% of the U.S.’s total electricity in 2023. By 2030, that number is expected to more than double.

A single AI data center, on the other hand, has about 5,000 servers and is optimized for high-performance computing. It consumes enough energy to power a city of roughly 8,000 residents. Altogether, this has put an unprecedented strain on our energy grids.

Electricity demand in the U.S. was basically flat from 2008 to 2021. It grew by an average of 0.1% per year during that period. As AI technology has taken off, demand for power has exploded… Demand grew by 2% in 2024, and this trend will only accelerate.

As a result, the biggest tech companies are scrambling to secure consistent power solutions.

Industry experts agree that nuclear energy is the long-term solution for the U.S.’s growing power needs. As we wrote back in May, it’s cleaner than traditional sources like oil and coal, and more reliable than solar or wind.

Microsoft (MSFT) has already agreed to purchase all the power from the revived Three Mile Island nuclear reactor for the next 20 years… And the company will pay more than twice the market rate for it. Meta Platforms (META) plans to do much the same with a nuclear power plant in Illinois starting in 2027.

But not everyone can follow in Big Tech’s footsteps. Nuclear reactors take a long time to reactivate… Three Mile Island, for example, won’t be ready for another two years. Many smaller companies can’t wait that long… and most can’t afford to pay extreme rates for their energy.

To tackle the electricity needs of today, we think natural gas is the best solution…

It’s the only clean energy that can handle the current power demand from traditional and AI data centers. And Bloom Energy has found the optimal way to harness natural gas for this booming technology…

To be clear, it isn’t an exploration and production company… Bloom doesn’t collect natural gas from deep, underground reservoirs. Instead, it’s a global leader in solid oxide fuel cells (“SOFCs”).

These devices are made of rare earth elements (“REEs”), which enable electrical conductivity. They also convert natural gas, biogas (a mix of methane and carbon dioxide), and hydrogen into electricity.

Traditionally, natural gas is burned to create energy through combustion. It’s also how we extract power from coal and oil. Bloom, on the other hand, converts natural gas directly into electricity through electrochemistry…

Without getting too technical, Bloom’s SOFCs combine oxygen and natural gas in a reaction that releases electrons and ultimately creates electricity.

It’s important to note that electrochemistry doesn’t involve any combustion. This process produces no particulate pollution and virtually no water waste. It limits emissions and makes electrochemistry far cleaner than traditional techniques.

Bloom’s SOFCs are also a more reliable energy solution…

You see, Bloom’s SOFCs can be deployed directly on-site… to data centers, hospitals, and tech hubs. That’s because they’re not linked to the existing electrical infrastructure.

In other words, if severe weather or large electrical loads disrupt an energy grid, SOFCs are unaffected… Power just keeps flowing where it’s needed.

This level of reliability can also benefit telecommunications firms, media companies, food and beverage retailers, and manufacturers. Power loss in any of these markets can cost companies millions of dollars. And it’s a huge reason why…

Grid-Independent Power Is Poised for Massive Growth

Currently, 13% of all data centers use some form of on-site power, whether as a primary or backup energy source. By 2030, that figure is projected to rise to 38%.

The global fuel cell market as a whole is expected to grow 26% per year through 2030.

Bloom is a compelling player in this space because its SOFCs are both scalable and easy to set up. They’re compiled into stacks that can be expanded (or minimized) based on a customer’s specific energy needs.

That means Bloom can power a wide range of facilities… from small data centers or semiconductor plants that use between 5 and 10 megawatts (“MW”) per year… to large-scale data centers that exceed 100 MW of usage.

Most important is how quickly Bloom can scale this energy output… It takes a nuclear power plant 10 to 20 years to go from planning to operation. The company’s fuel cells, on the other hand, can be fully operational within 90 days.

Clearly, Bloom offers a unique combination of products and services…

SOFCs make up 74% of Bloom’s total sales. The rest comes from the installation and maintenance of fuel cells and the sale of electricity itself.

Individual fuel cells within a single Bloom server have an initial useful life of around five to eight years. That’s how long these products are functional and economically beneficial. With proper maintenance, though, a full system can run for decades.

This is why clients often sign long-term agreements with Bloom… to consistently maintain and replace the components that make up their energy systems. The best part is, these services allow Bloom to generate revenue without having to sell additional fuel cells.

Furthermore, the company owns the hardware it installs on-site. And customers contract with Bloom to buy the power it produces.

This mix of services generates stable cash flow even after Bloom sells its initial fuel cells. And as demand for grid-independent power has grown, the company has started proving its mettle…

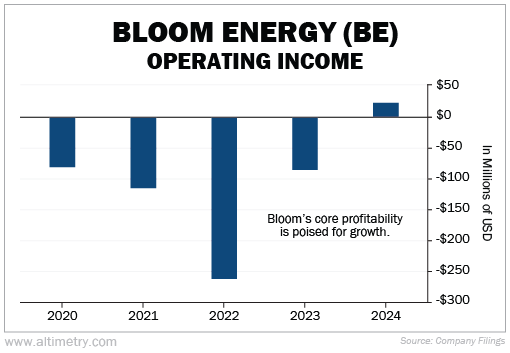

Between 2020 and 2024, Bloom’s revenue has nearly doubled, from $794 million to $1.5 billion. The company’s operating income (which reflects core profitability) is even more impressive… It has risen from negative $81 million to $23 million in that same period. Take a look…

Thanks to the AI boom, Bloom is selling and managing enough energy systems to cover its fixed costs and make money on an as-reported basis.

All signs point to more growth…

Bloom currently has a $2.5 billion backlog… That’s nearly two years’ worth of sales at its current sales rate (measured over the past 12 months).

In order to keep up with this work, plus growing demand, Bloom is expanding its footprint… The company opened its second manufacturing facility in 2022, nearly doubling the size of its production space.

What does this mean? Bloom produced roughly 200 MW of electricity in 2024. It now has the capacity to deploy up to 1 gigawatt (1,000 MW) of power each year. That’s almost as much as the total power Bloom has produced in its entire history.

Simply put, it has a lot of room to grow with minimal investment going forward.

It’s also important to note that Bloom’s two main production facilities are located in the U.S. Given the unpredictable tariff environment, businesses prefer to operate on American soil.

And as we mentioned earlier, Bloom needs REEs to construct its fuel cells. So it’s crucial to understand where the company sources these materials…

Bloom acquires REEs like zirconia and scandium from European and Asian countries. While these markets are subject to tariffs, Bloom doesn’t source these elements from China, which is facing some of the steepest tariffs.

The bottom line is, Bloom is well positioned to solve the most critical problem in the AI era – how to deliver massive power quickly, cleanly, and reliably.

Bloom’s SOFCs and related services offer unique solutions for its clients. And as the company scales and demand for electricity continues growing, Bloom is becoming more dominant in the energy space.

The problem is, investors don’t believe Bloom can be profitable in the long term. We can look at its flawed as-reported accounting to explain this disconnect…

Wall Street’s Fog

Based on generally accepted accounting principles (“GAAP”), Bloom doesn’t look like a business that’s primed to benefit from AI tailwinds.

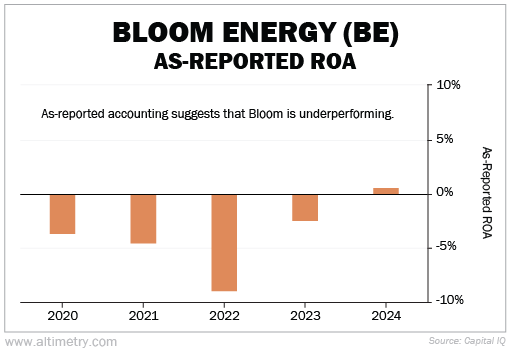

As we highlighted earlier, Bloom only became profitable from an as-reported perspective last year. Prior to 2024, the company’s annual as-reported return on assets (“ROA”) averaged negative 5%.

And last year, the company barely generated positive returns, with an as-reported ROA of around 1%. Take a look…

Still, those figures are well below the company’s 5% breakeven point.

So according to GAAP accounting, Bloom isn’t the next big thing in energy. It’s a business struggling to keep the lights on.

Uniform Accounting, on the other hand, tells us a different story…

Understanding Bloom Energy’s True Potential

Uniform Accounting insights show us at least four ways the GAAP numbers are massively misstating Bloom Energy’s profitability and cash-flow potential…

1. Misunderstanding of stock-option expenses. It doesn’t take any actual cash from the company’s operations to issue stock options to employees. Options may dilute the stock for shareholders… But this is in no way a negative for operating cash flow.

Because of the way stock options are treated in as-reported accounting, Bloom’s earnings, earning power, and operating cash flows all appear lower than they are in reality.

2. Interest expenses. The amount that a company pays on its debt has nothing to do with its operations. Under Uniform Accounting, we remove this number as an irrelevant cost that shouldn’t impact profitability.

3. Research and development (R&D) capitalization. Under GAAP, companies treat R&D as a yearly expense. They measure it the same way they measure paying for employees or raw materials. In reality, R&D is a multiyear investment into the future. So treating it as an expense makes ROA look worse than it is.

4. Excess cash. When times are good, Bloom has more cash on its balance sheet than it needs to run the business. As-reported metrics include all cash in calculations like ROA. We remove all cash except what the business needs to operate.

When we make these and other adjustments to Bloom’s financials, it’s clear that the business is stronger than as-reported metrics suggest.

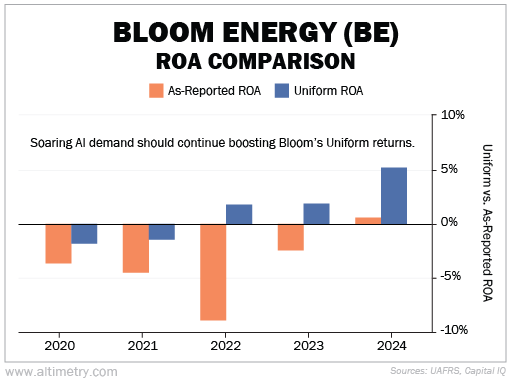

After cleaning up Bloom’s accounting, its true profitability becomes obvious…

While the company posted negative Uniform ROAs in 2020 and 2021, Bloom generated positive returns in 2022. The company’s new production facility, along with growing demand for AI technology, boosted its scale and helped the business become profitable.

Since then, Bloom has continued performing well. Its Uniform ROA has climbed from 2% in 2022 to 5% today. Take a look…

Bloom has proved that it can consistently generate positive returns. In fact, the company’s Uniform ROA has improved in each of the past five years.

Simply put, Bloom is becoming more sought-after as demand for reliable electricity grows.

Remember, the percentage of data centers using grid-independent power is set to nearly triple in the next five years. And Bloom’s profitability should follow a similar trend.

Yet the market is underestimating just how profitable this business can become…

What Investors Are Missing About Bloom Energy

Bloom offers industry-leading solutions that supply data centers with reliable power. However, investors are doubting how dominant this business will become in the next five years.

We can see this through our Embedded Expectations Analysis (“EEA”) framework…

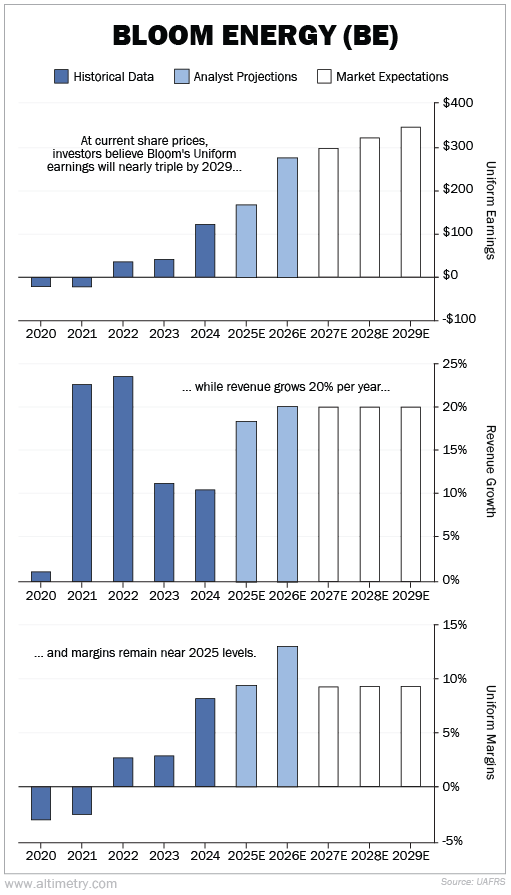

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to justify what the market is paying for it today.

The market understands that Bloom is operating in the booming electricity sector. Investors expect revenue to grow 20% each year through 2029… That’s less than the fuel-cell market’s estimated 26% growth rate worldwide.

At the same time, the market only expects Bloom’s Uniform margins to improve slightly in the next five years, from 8% to 9%.

This translates into Uniform earnings growth of $220 million – from $120 million in 2024 to $340 million by 2029.

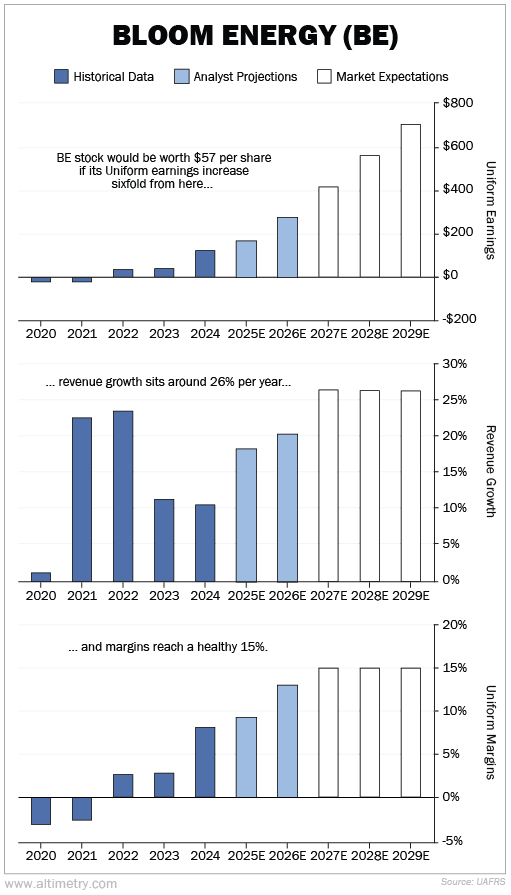

This estimate is too pessimistic… and Wall Street analysts agree. They project that Bloom’s Uniform margins will improve from 8% in 2024 to 13% in the next two years.

The company’s Uniform margins could climb even higher… They could reach 15%, based on its economies of scale. In other words, we can expect better margins as new sales surpass the fixed costs associated with increased production.

Think about how larger power-equipment players, like Ireland-based Eaton (ETN), produce Uniform margins that match or exceed these levels.

Similarly, an industry leader like Bloom should be able to grow its top line in tandem with the broad fuel-cell industry, at 26% per year.

At these levels, its Uniform earnings are projected to reach $702 million by 2029. This translates into a stock price of $57 per share… or 125% upside from today’s prices.

Embedded Expectations vs. Fundamental Potential

Market Expectations at Current Price

Bloom Energy at $57 per Share

Bloom is filling the vital need for power as the AI revolution gains momentum. It provides grid-independent energy that can be built and expanded quickly, as needed.

With nuclear solutions still years away, Bloom’s SOFCs present the ideal short-term option. So as demand for electricity increases, Bloom’s future looks bright.

Better yet, longtime subscribers know we previously teamed up with our corporate affiliate Chaikin Analytics to curate a list of what we call “Perfect Stocks.”

It consists of misunderstood companies with plenty of upside potential… that have also triggered “bullish” or “very bullish” ratings in the Chaikin team’s Power Gauge tool.

We’re excited to report that Bloom qualifies as a Perfect Stock today. It’s another reason we believe in this stock.

We just need to make sure management is well positioned to make the most of this opportunity.

Management Is Paid to Grow the Business in Key Areas

Looking to the DEF 14A and Financial Red Flags for Warnings

Buried deep in the company’s annual proxy statement is what’s known by its legal name as the DEF 14A. Most of the proxy is boilerplate, but the company is legally required to reveal how management is paid.

Not only does it show how much these executives are paid… it also details how they’re paid. Specifically, it tells us whether management’s compensation focuses on the right issues.

Bloom Energy co-founder and CEO KR Sridhar’s salary accounts for just 1% of his total compensation. Annual cash bonuses make up 2% of his pay, with the lion’s share coming from long-term equity awards.

For the rest of management, salary makes up 5% of pay. Annual bonuses add another 5%, with 90% of compensation coming from long-term bonuses.

Management’s short-term compensation is based on a mix of operating income, gross margin, and revenue growth. Long-term awards are based on product revenue growth and product gross margin.

Overall, this is a solid framework. Management’s short-term compensation will encourage profitable growth for Bloom. And its long-term bonuses will focus the team on the company’s largest and most important revenue source – SOFCs.

Encouraging product revenue growth and margin improvements will lay the foundation for long-term service-based revenue and higher earnings. Given that most of management’s compensation comes from equity awards, we’re confident that management is aligned with shareholders, which should maximize our returns.

Now we know that management should be motivated to take the company in the right direction. But we still need to look at how confident the team is in Bloom Energy today.

For this, we’ll turn to our Earnings Call Forensics (“ECF”) analysis.

We use advanced audio technology to analyze management’s voices on earnings calls. Our software measures inflections in the speakers’ speed of speech, tone, hesitation levels, and even changes in “breathiness.”

Then it compares that against their spoken words and the numbers to generate two types of markers – “questionable” and “confident.” It gives us a window into sentiment, as well as how operations are going.

We kept an eye out for a few topics in Bloom’s first-quarter earnings call…

- Tariffs

- Revenue growth

- Macro tailwinds and headwinds

- Data-center customer growth

Bloom’s management generated a “questionable” marker when discussing short-term economic pressure. This suggests that the team may be concerned about potential headwinds, like tariffs.

That said, management repeatedly stated it was confident in the overall AI megatrend… and the tailwinds it generates for the business.

We’ll continue paying close attention to the company’s financials in the next few quarters. But like Bloom, we don’t think any near-term blips will disrupt overall market trends in AI and power demand.

Folks, the AI revolution is undeniable. Data centers are sprouting all over the country, as tech companies build out their latest AI models. And as more data centers crop up, these firms need to figure out how to power them.

That’s where Bloom comes in. Demand for electricity is soaring. And Bloom offers clean, reliable, and easy-to-scale solutions, plus the services needed to maintain them.

Right now, we have a great opportunity to invest in a business that’s becoming the backbone of the AI ecosystem. We recommend you…

To get Joel’s recommended entry price, sign up here.