Issue #76, Volume #2

How Shelby Davis Became a Billionaire With Only One Kind of Stock

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| At age 40, he had nothing to show for his life… 40 years later he was a billionaire… He used a simple formula that still works today… Own offsetting assets that zig when others zag… Porter will share his portfolio strategy in a video for Partners on Friday… a Big Secret holding gets a $2 billion legal win… |

Editor’s note: Today’s Journal is Part III in a special three-part series of Porter’s personal guide to great investing. These concepts aren’t the basics, like the time value of money, but instead these are the core concepts that Porter learned from his most valuable mentors, like Bill Bonner, Harry Browne, and T. Boone Pickens. We encourage you to read Part I (use other people’s money) and Part II (never lose money) before reading today’s Journal. On Friday, July 4, we’ll take a break from our normal publishing schedule and, instead, Porter will be sending a video (to our Partner Pass members) detailing exactly how he puts these ideas to work in his own $18 million personal portfolio. As long-time readers will recall, there’s no such thing as teaching. There’s only learning.

By 1948, Shelby Davis was a disappointment to everyone – including his wife.

The scion of Illinois’ most powerful political family, Davis was handed a life of wealth and privilege very few Americans can imagine, even today.

His family sent him to The Lawrenceville School in New Jersey, America’s most elite boarding school. After graduation (1926), he walked across the lawn and studied political science at Princeton University (1930). Then he received a master’s degree from Columbia University (1931). And, in the middle of The Great Depression, his family paid for him to get a PhD from the Graduate Institute of International Studies in Geneva (1934).

What did the talented Mr. Davis pursue in life with his masterpiece of a global education? A wife.

In Geneva, Shelby met Kathy – Katherine Wasserman, the daughter of America’s wealthiest textile family (Fruit of the Loom).

And so, Shelby Davis, with every possible advantage, began to make his way through the world. Family connections landed him a plum job as a European correspondent for CBS. And then he latched on to one of America’s leading politicians, Thomas E. Dewey.

Dewey, as governor of New York, was widely expected to end up as president of the United States. If so, along with everything else Davis had been given, he would have been ushered into the very highest echelon of power and influence.

Davis was Dewey’s leading political analyst and the architect of his campaign for the presidency in 1944. But the campaign ended in an epic failure. Franklin Roosevelt won an incredible fourth term. Davis was out of a job.

Governor Dewey used his power to appoint Davis to a newly created sinecure position, the “deputy” superintendent of insurance for New York. And there Shelby Davis sat, wasting life away at a made-up government job that couldn’t possibly provide the lifestyle his wife expected.

In 1947, Davis was almost 40 years old. He had virtually nothing to show for his life, except a wife and three children he couldn’t afford. It was time to get busy living or get busy dying.

Shelby Davis then commenced the most extraordinary investment program in the entire history of the capital markets. Over the next 40 years, he’d turn $50,000 into almost $1 billion.

Learning about insurance as a government regulator, Davis figured out one of the greatest secrets in all of finance: the Cantillon Effect.

In 1755, Richard Cantillon, a French economist who’d studied the great inflations of the early 1700s (John Law, the Mississippi Company, the South Sea Bubble), described how, during periods of monetary inflation, institutions like central banks and the governments benefitted by gaining access to newly created money first, before others in the economy. This allowed these favored institutions to profit handsomely as the resulting inflation lifted prices on financial assets and commodities.

Davis understood the Cold War with the Soviets meant there would be no “peace dividend” – government spending was going higher so far more inflation was coming. Davis knew insurance companies are Cantillon Effect winners: they get all of the capital they need, for free, and they get it first. Thus, insurance companies would be able to constantly front run all the resulting monetary inflation. Davis could do the math in his head: 8% to 10% a year in inflationary gains by investing the insurance premiums (known as “float”) plus 8% to 10% a year in underwriting profits would lead to very consistent, market-beating returns.

He borrowed $50,000 from his wife’s family and acquired a small brokerage firm (Frank Brokaw & Co.), renaming it Shelby Cullom Davis & Co. The firm owned a seat on the New York Stock Exchange, which allowed Davis to borrow (on margin) at very low interest rates. He borrowed the maximum allowable margin (1.5x equity) and invested in around a dozen high-quality insurance companies. Then, as now, these businesses were poorly understood. And because the market was still recovering from the Great Depression and World War II, they were trading at very low multiples: between 3x and 4x earnings. Within a year, thanks mainly to leverage and the performance of one stock, Crum & Forster, his $50,000 portfolio grew to $234,790.

As he knew they would, insurance stocks continued to compound steadily. With the leverage he was using, Davis saw his equity compound at rates over 20% annually. He continued to reinvest the dividends. And he continued to add more and more leverage as his equity increased.

Over time, Davis learned to recognize the two characteristics of a great insurance company: excellent underwriting and efficient marketing. He’d go on to focus his portfolio in a handful of great insurance companies, like GEICO, Progressive (PGR), and Chubb (CB).

In the 1960s, American stocks began to trade at much higher multiples (the market peaked in 1966). To find better opportunities in insurance stocks, Davis traveled to Japan, where he invested in deeply undervalued insurance companies, including: Tokio Marine & Fire, Sumitomo Marine & Fire, Taisho Marine & Fire, and Yasuda Fire and Marine.

Throughout the rest of his life, Davis continued to focus exclusively on insurance, discovering new companies as they emerged like American International Group (AIG) and American Family Insurance (AFLAC). He also understood the mortgage insurance business and invested heavily in Fannie Mae because of its insurance component after its IPO in 1968.

Finally, in the 1970s, Davis invested in the best property-and-casualty (P&C) company of all, Warren Buffett’s Berkshire Hathaway.

Whenever the markets fell, Davis would double and triple down on the best companies in his portfolio, pouring in capital on margin. The strategy almost bankrupted him during the severe bear market in 1973-1974. And on Black Monday in October 1987, his portfolio lost $125 million. His reaction? He bought aggressively.

When the market rebounded, his wealth soared. By 1988 his net worth had ballooned to almost $400 million, landing him on the Forbes 400 list of the wealthiest people in America.

When Shelby Davis died in 1994, his portfolio had achieved a compound annual growth rate of 23% for an incredible 47 years. His net worth was just shy of $1 billion. And by the time his wife died in 2013, the portfolio was worth several billion. Hopefully, she wasn’t disappointed in him anymore.

Shelby Davis is the best demonstration of the third rule of great investing: compounding over the long term. You must compound your capital consistently, at the highest rate possible, for as long as possible.

Shelby Davis is the only truly outside, passive investor who’s ever made more than $1 billion in the equity markets solely with his own capital. His track record is as good as Warren Buffett’s, but he made his fortune exclusively with his own account. And, unlike Buffett, he was never an activist investor. He simply used margin to buy ultra-high-quality businesses that he knew were virtually certain to compound at much faster rates than inflation.

It’s a simple formula that still works today.

The key to it? You must make sure you’re investing in businesses that will compound capital at a high rate.

One simple way to do so is following Shelby Davis’ example and invest in high-quality insurance companies, like the kind we recommend to our subscribers in The Big Secret On Wall Street.

To date, the average annual return on our recommended insurance stocks is 33.2% – without any losing positions.

Another way to do so is to look for companies that pass the Rule of 40 test.

Take two critical data points: earnings growth and return on equity and add them together. If the resulting number is over 40%, then the business is an elite compounder.

If a business can grow its operating earnings (we use EBITDA – earnings before interest, taxes, depreciation, and amortization – as a reference point) at 20% a year while earning a 20% return on equity, it’s producing Rule of 40 quality results.

Look at Kinsale Capital (NYSE: KNSL), for example. As paid-up subscribers to The Big Secret know, Kinsale is one of our highest-rated insurance companies. Over the last year it has produced a 30% return on equity, which is extraordinary for an insurance stock. And it’s grown its operating profits (EBITDA) at 18.6%, producing a Rule of 40 total of 48.6.

Not many companies can maintain these kinds of extraordinary results year after year. But there are some. A few that have done so consistently the last few decades are: Apple (AAPL), Microsoft (MSFT), Coca-Cola (KO), Philip Morris International (PM), McDonald’s (MCD), Nike (NKE), Moody’s (MC), S&P Global (SPGI), Mastercard (MA), Yum! Brands (YUM), NVR (NVR), Alphabet (GOOG), and Williams-Sonoma (WSM).

As I’ve built my own portfolio, I’ve matched Rule of 40 businesses (and companies that I believe will become Rule of 40 businesses) against non-correlated assets: gold and bonds.

This strategy – of owning offsetting, non-correlated financial assets that “zig” when these stocks temporarily “zag” – has allowed me to build a portfolio that has much less volatility than the market (beta: 0.83). That enables me to use margin safely to greatly increase my returns – currently up 55% year-to-date.

The combination of high returns and low volatility produces an incredible Sharpe Ratio: 2.20. Sharpe ratios above 1.0 are the holy grail of investors, as they mean you’re getting more return than you’re taking in risk.

No, this isn’t normal. But it’s exactly what you must do if you want to be a great investor.

For Partner Pass members, when you look at my portfolio’s construction (in the video I’ll send you on Friday), please notice that I have balanced my operating company investments (about $7 million in capital) equally with bond market allocation (via insurance companies) and my investments in gold.

To become a Partner Pass member and get access to my video and everything else that we publish at Porter & Co., call this number: 844-933-9986.

This combination of very consistent earnings from great insurance companies (and the “ballast” of the bonds on their balance sheets) plus the stability of gold is juxtaposed against the higher growth potential of Rule of 40 operating companies, producing exceptional results.

I’ll admit, the way I’ve combined the things I learned from Harry Browne (the permanent portfolio’s non-correlated, low-volatility structure) along with the lessons of Shelby Davis (the incredible advantage of insurance companies in an inflationary environment), and Warren Buffett (a focused approach with a small number of ultra-high-quality companies) isn’t anything I’ve ever seen before.

But, I bet when Shelby Davis tried to explain what he was doing to other investors back in 1948, they didn’t understand it either.

Tomorrow, Marc Chaikin Is Closing The Doors

Presented by Chaikin Analytics

Until tomorrow, you can claim one FREE year of Marc Chaikin’s new “EQ” Power Gauge and essentially six free months of Chaikin’s Breakthrough Investor as part of a special Charter invitation. It’s a brand-new product with an underlying system that could help you double your money by foreseeing the biggest earnings beats, BEFORE they occur, especially in AI and high tech. Doors close on this Charter offer tomorrow.

Three Things To Know Before We Go…

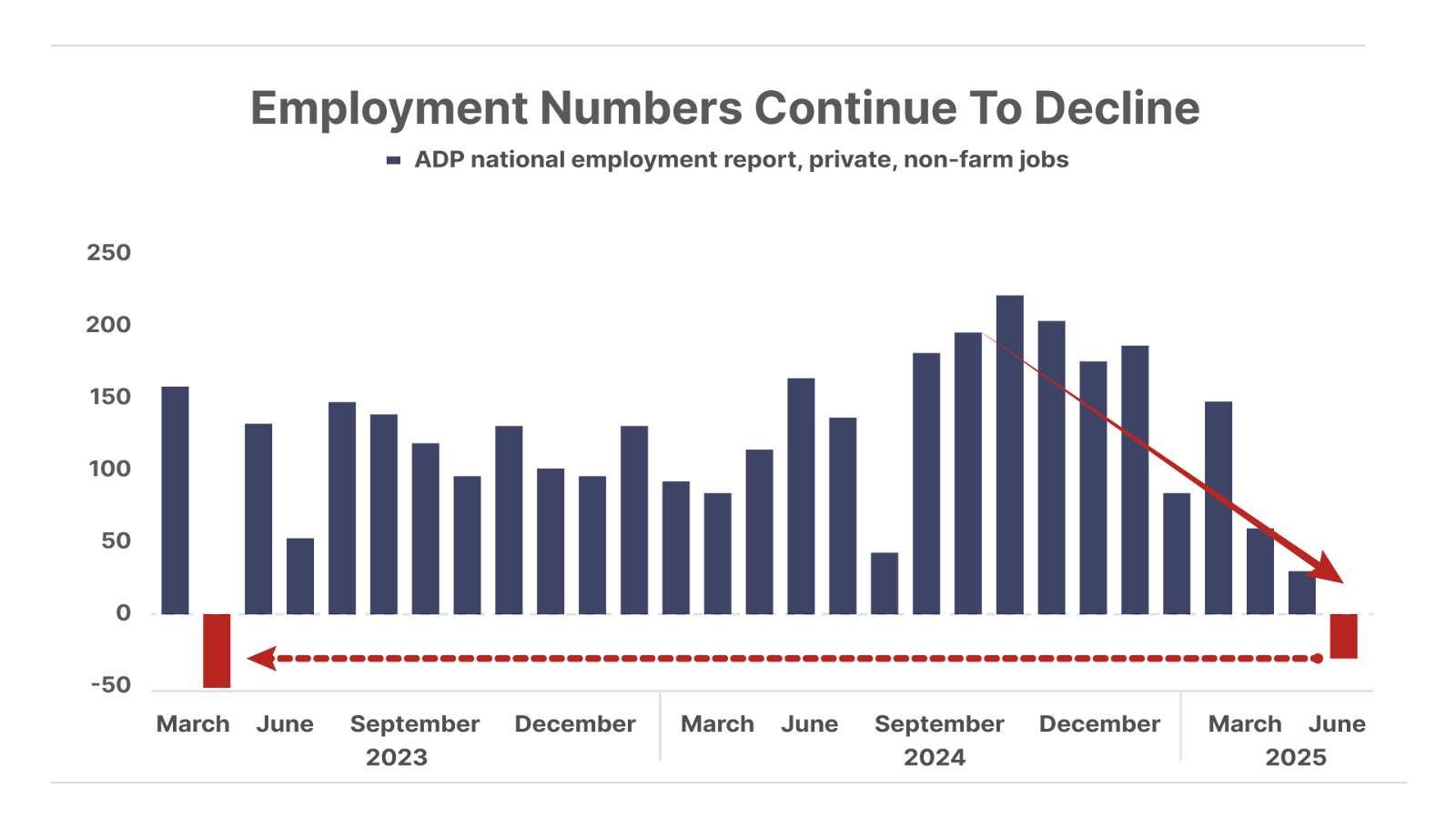

1. More signs of job-market weakness. This morning, payroll processor ADP reported U.S. private businesses reduced the number of jobs last month for the first time in over two years – companies eliminated 33,000 jobs in June, the first monthly decline since March 2023. Payroll growth has now been trending lower since last October, and fallen in seven of the past eight months. Yet the stock market is at an all-time high.

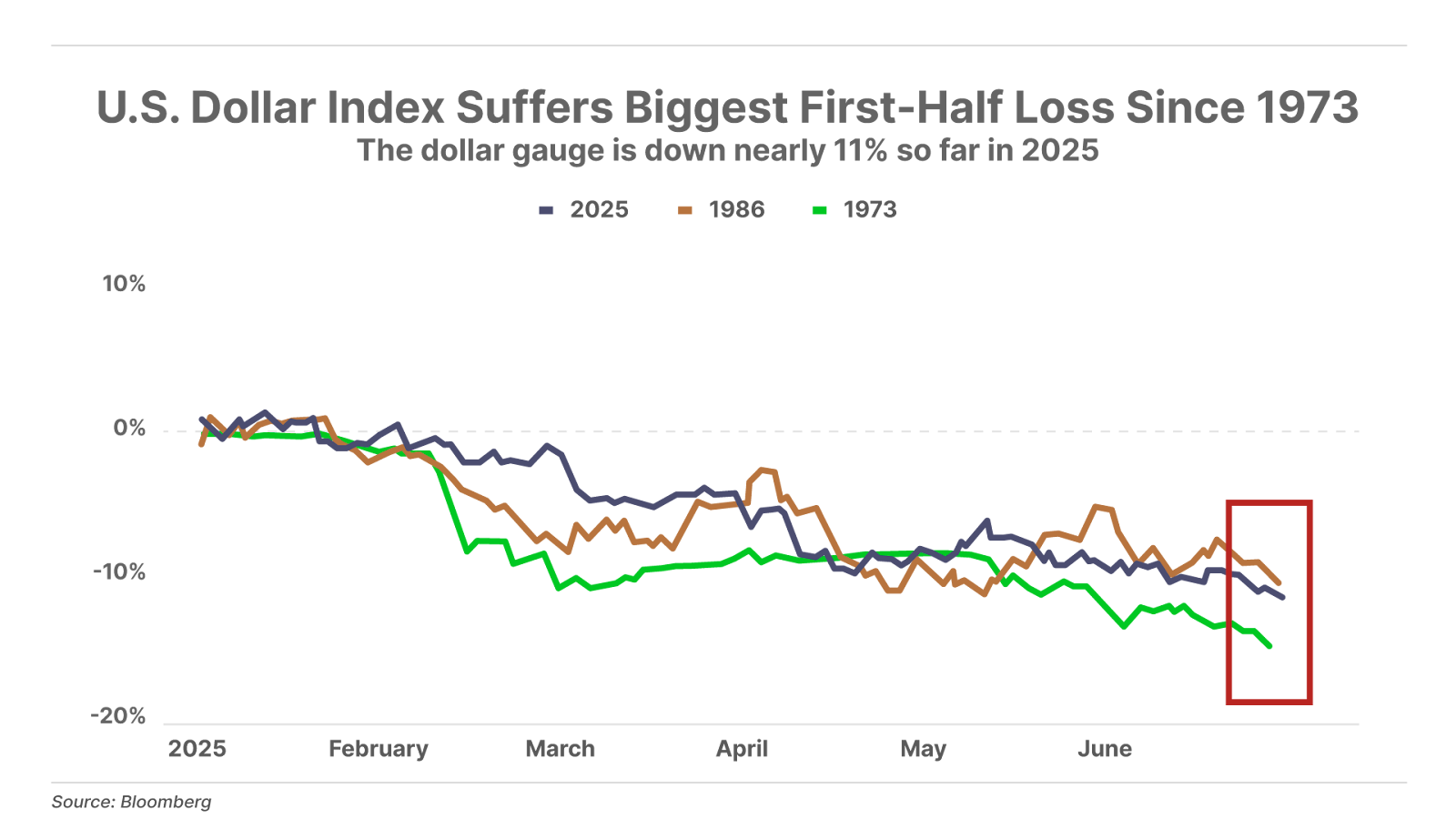

2. The U.S. dollar nears bear market territory. The Dollar Index (DXY) is down 10.8% – its worst first-half performance since 1973, when the gold-backed Bretton Woods system ended. This marks six consecutive months of declines, matching the longest downtrend in 80 years and the steepest six-month drop since 2009. Meanwhile, gold has surged 29% this year, underscoring its role as a hedge against currency instability. While a weaker dollar can ease the burden of the U.S.’s massive debt, it also raises import costs and undermines purchasing power. If the dollar’s decline continues, it could threaten its status as the world’s reserve currency.

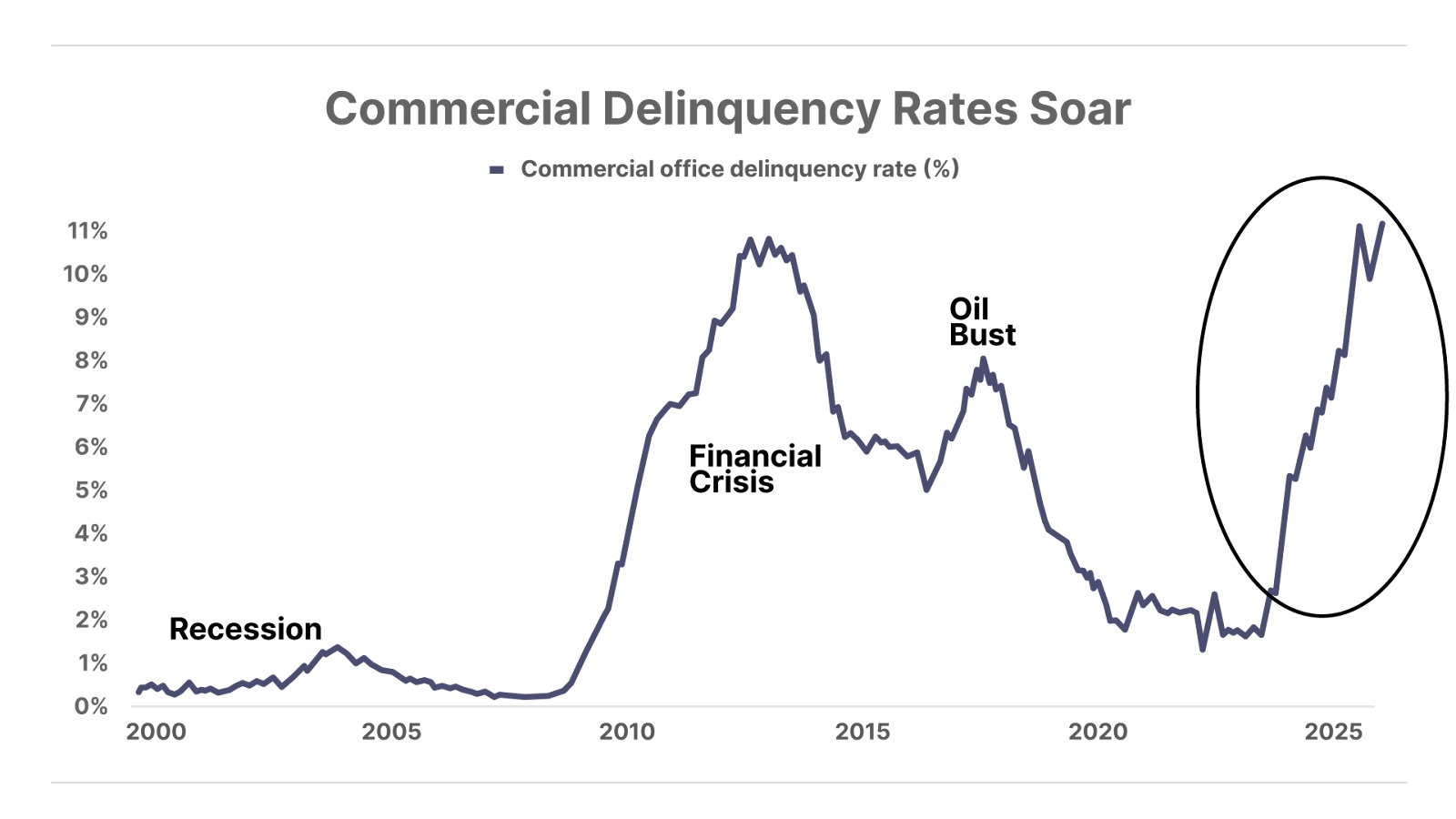

3. Commercial real estate bust accelerates. Delinquency rates for commercial mortgage-backed securities among office real estate properties reached 11.1% – an all-time high, surpassing peak levels reached during the Great Financial Crisis. With interest rates remaining relatively high, and occupancy rates for office space still low, there’s little hope for relief in this troubled sector of the economy.

And One More Thing… An Asymmetrical Opportunity

The most asymmetric opportunity we’ve ever seen. One of the portfolio holdings in The Big Secret On Wall Street and The Trading Club is on the winning side of the largest judgment ever awarded against a foreign country in the history of the U.S. legal system. For nearly two years, this foreign government has refused to pay up. But on Monday, a U.S. judge ordered the recalcitrant government to hand over its stake in a major oil company as security to ensure payment.

The company’s share of this payment is about $2.4 billion, yet its current market cap is less than $3 billion. So despite an 11% gain in its share price this week, we believe Mr. Market is missing what could be the most asymmetric opportunity we’ve ever come across.

To get access to this recommendation and our latest update on the company, click here to join The Big Secret On Wall Street.

Poll Results… Do You Invest With Leverage?

On Monday in the Daily Journal, we asked readers about their use of leverage in investing… and 36% said they “rarely use leverage,” 32% said they “have never used leverage but are willing to try.” Of those taking the survey, 17% said they use leverage regularly, and 15% never use it and never will.

For Partner Pass members, please let me know what you think about my portfolio after you see the video I’ll send on Friday. What would you do differently? Let me know: [email protected]

Good investing,

Porter Stansberry

Stevenson, Maryland

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.