Issue #48, Volume #2

How One Subscriber Escaped Poverty To An Oceanfront Life

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| A step-by-step guide to selling puts… The upside is big gains on invested capital… The downside is owning shares of a company you already want to buy… The options market is willing to pay a substantially higher premium for this company… Foreign banks are unloading U.S. Treasuries… |

In June, Porter & Co. will be launching the Trading Club, a new service that will guide subscribers through a series of actual trades using strategies such as put selling, covered calls, crypto buying and selling, special-situation investing, and more.

So today, Porter is turning the Daily Journal over to Big Secret On Wall Street analyst Ross Hendricks, who will be taking the lead in sharing trading methods with Trading Club subscribers… Ross walks readers through a real-time strategy that involves selling puts on a high-quality, oil-and-gas royalty company.

Here’s Ross…

In last week’s Big Secret On Wall Street, we shared a trading strategy that Porter wrote about in 2015, which is just as relevant today, describing the safest way to make a fortune in distressed markets:

“In the bond market, the key to success is avoiding default. In the stock market, the key to success is even easier: it’s to only sell puts on stocks that you’re genuinely happy to own and at a strike price that reflects an excellent value.”

Porter went on to describe how his recommendation to sell puts in shares of the high-quality jewelry brand Tiffany in February 2009 generated a 29% annualized return, while taking virtually no risk (the only downside was owning one of the world’s best jewelry brands at a deeply discounted price).

In today’s Journal, we’re going one step further and providing an actionable put-selling trade we’re recommending right now. This includes a step-by-step guide detailing a live example available in the market, which ends with one of two outcomes:

- Owning shares in one of the world’s best businesses at an 11% discount

- Earning a 28% annualized return on invested capital

It’s the closest thing you’ll find to a free lunch on Wall Street: a strategy that can consistently deliver double-digit returns on capital, where the only downside is buying a stock, you already want to own, at a discounted future price.

Of course, many investors will sadly never take advantage of options. Why? For the same reasons that prevent them from taking advantage of things like corporate bonds. It’s complex and involves more work. It requires filling out a form with your broker to get options-trading approval. And the trades aren’t as straightforward as pressing the buy and sell button as with regular stocks. For these reasons, we suspect 90% of our subscribers will never even attempt trading options.

But for the 10% who will, we’re confident you’ll become options-trading converts after seeing how it can take your investing prowess to the next level. But don’t just take our word for it. Take it from subscriber Jeff Wheeler, who wrote in last week and explained how options trading transformed his life from one of a college dropout to a comfortable retirement with an oceanfront home:

“I can now earn more income annually than I ever received in a paycheck and I do it while enjoying my morning coffee. The underwriting aspect and collecting premium up front also correlated with your advice on why insurance companies make the best investments.”

As Jeff hints at, selling options gives everyday investors the chance to become their own miniature insurance company. In the case of a put option, the seller offers the buyer insurance that protects against a decline in a stock’s price below a certain level, over a specified period of time. Thus, selling put options can be viewed as selling insurance against share-price declines to other investors. In exchange for providing that protection, option sellers collect upfront cash premiums that can then be reinvested – effectively engineering their own personal insurance float.

And it should come as no surprise that subscriber Jeff and countless others have had so much success with this strategy, given that insurance companies are the most profitable and best-performing segment of stocks we’ve ever recommended in The Big Secret.

Think Like An Underwriter

The key to success in selling options is to think like a good insurance underwriter. Above all else, this requires a contrarian mindset. The best insurers keep their powder dry during “soft” markets, pulling back on selling insurance when prices are low. And when the tide inevitably shifts, those who played defense during the soft markets have the capital to deploy during “hard” markets, when investors scramble to buy insurance at sky-high prices.

For the broader stock market, represented by the S&P 500, we can measure overall investor appetite for volatility insurance by the level of the CBOE Volatility Index (VIX). The VIX is calculated using the 30-day put-option prices for the S&P 500, thus providing a measure of the expected (or implied) volatility in the S&P 500 index over the next 30 days.

In normal environments, the VIX trades between 15 and 20. During the recent market turbulence following President Donald Trump’s Liberation Day tariff announcements, the VIX shot up to as high as 60, and, though it’s come down, remains elevated at 25 as of Friday’s close.

The VIX at 25 means that investors are paying juicy premiums for volatility insurance, making now an ideal time for putting capital to work selling puts.

We can do one better by finding individual stocks for which the market is paying even richer premiums for volatility insurance, but with two important caveats. That is,

- only underwrite the world’s best businesses we’re willing to buy and hold forever, and

- only when those best businesses are trading at attractive valuations

These are the types of stocks we focus on in The Big Secret On Wall Street. The challenge is that, in many cases, insurance against share-price volatility in world-class businesses is often discounted, because these companies often trade with less volatility than the overall market. Consider put options for a company like Philip Morris International (NYSE: PM), which currently have a 30-day implied volatility (known as the IV30) of just 21, or 14% less than the S&P 500 at 25.

The ideal candidate we’re looking for is a wonderful “forever” business with very little long-term risk at current prices, but one with a share price that trades with higher volatility.

The Option-Selling Sweet Spot

For this trade, the candidate we’ve selected comes from the current The Big Secret On Wall Street portfolio: Viper Energy (Nasdaq: VNOM), an oil-and-gas royalty company we recommended in September 2022. In that issue, we explained how Viper’s incredible acreage position in the heart of the Permian basin makes it one of the highest-quality energy companies in the world. And as a royalty company, it’s also incredibly capital efficient, because Viper never invests in drilling holes into the earth. Instead, it owns and leases the land that other companies drill on, in exchange for a royalty fee on the production.

Viper has generated a 62% total return since our September 2022 recommendation, or 20% annualized. We believe the company can continue compounding capital at similar rates for long-term investors willing to hold the business through the commodity price cycle (i.e., five to10 years). Over this time horizon, we believe the shares come with little risk of a significant price drop.

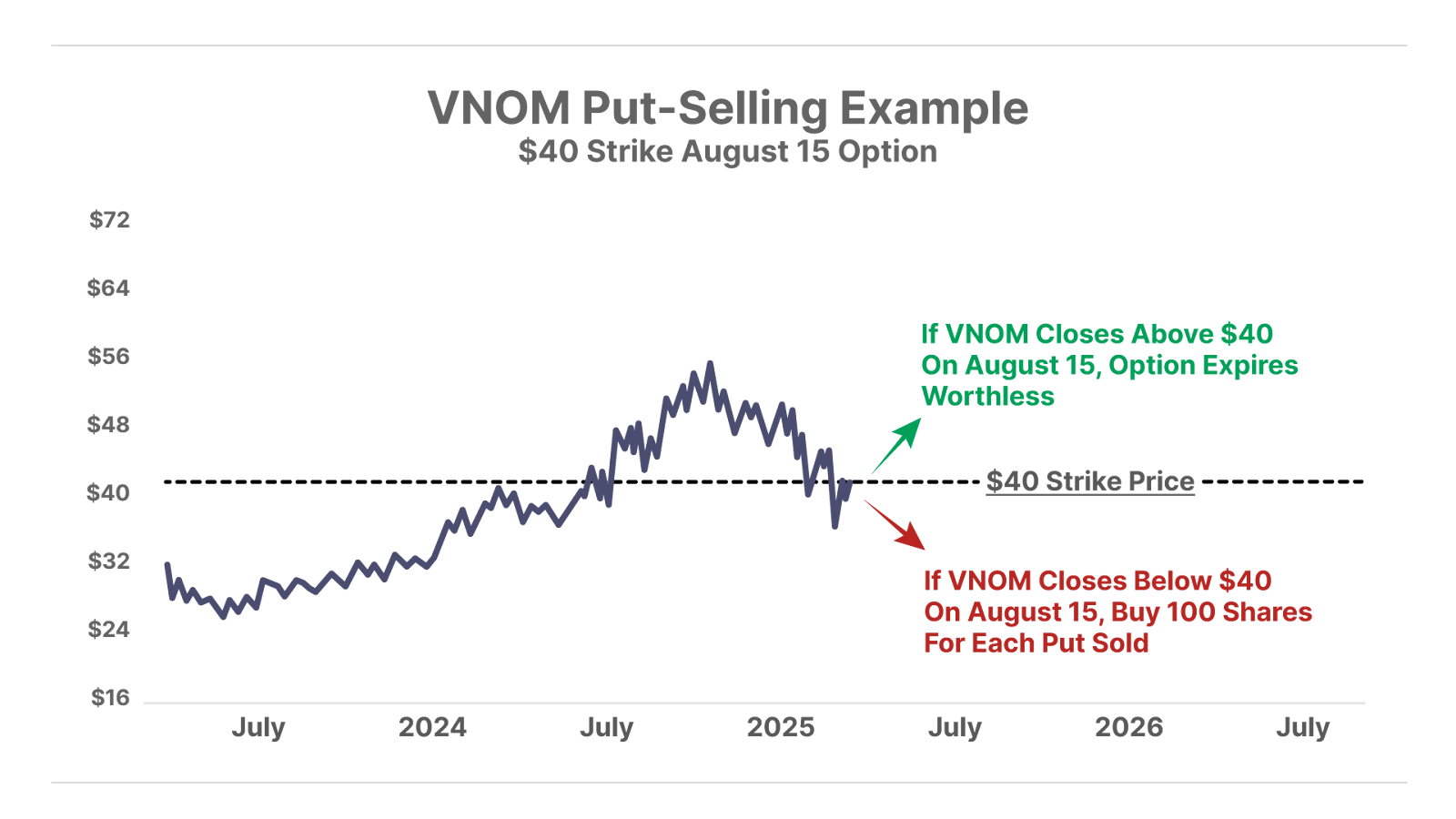

But because Viper is technically considered an “oil stock,” the share price can experience short-term price fluctuations driven by the erratic swings in the price of oil. Over the past few months, as oil prices fell more than 20% from $80 to $63 per barrel, VNOM’s share price declined 25% to $41.58 as of Friday’s close.

At this price, the business trades dirt cheap at just 15x last year’s free cash flow and less than 10x this year’s expected free cash flow. That’s an incredible value for a business of Viper’s quality, and a deep discount to the 26x free cash flow multiple of the S&P 500. Meanwhile, Viper’s 6% dividend adds an extra sweetener compared with the 1.3% dividend in the S&P 500.

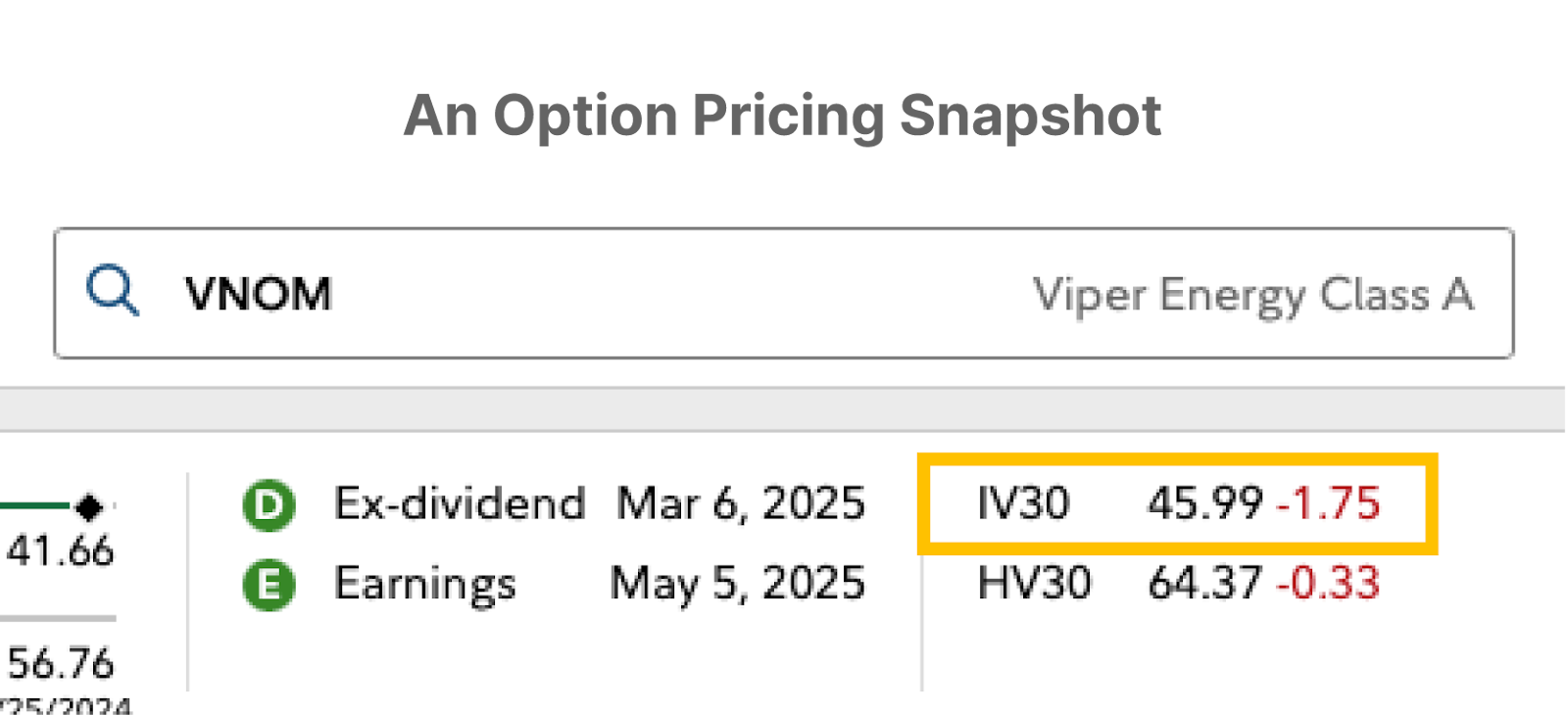

And in our view, the long-term downside risk to VNOM’s share price is substantially less than that of the S&P 500 at current prices. And yet, the options market is willing to pay a substantially higher premium for protection against VNOM’s share price. The snapshot below shows the 30-day implied volatility in Viper options prices (IV30) at around 46 as of Friday’s close, or 84% higher than the 25 level for S&P 500 as expressed in the VIX:

So to summarize our initial underwriting process so far: we have identified a wonderful and durable long-term business whose shares are trading at a deeply discounted valuation, making for a low-risk investment. Meanwhile, investors are paying higher options premiums to protect against downside risk in the share price – risk that we’re willing to take. This low-risk/high-volatility combination is right in the sweet spot for an option-selling candidate:

Now that our underwriting work is complete, it’s time to set up the trade.

How To Structure The Trade

The first thing we must decide is for what length of time we’re willing to insure against downside share-price risk. This is known as the “option expiration date,” and it can range anywhere from zero days (options that literally expire the same day you sell them) out to multiple years.

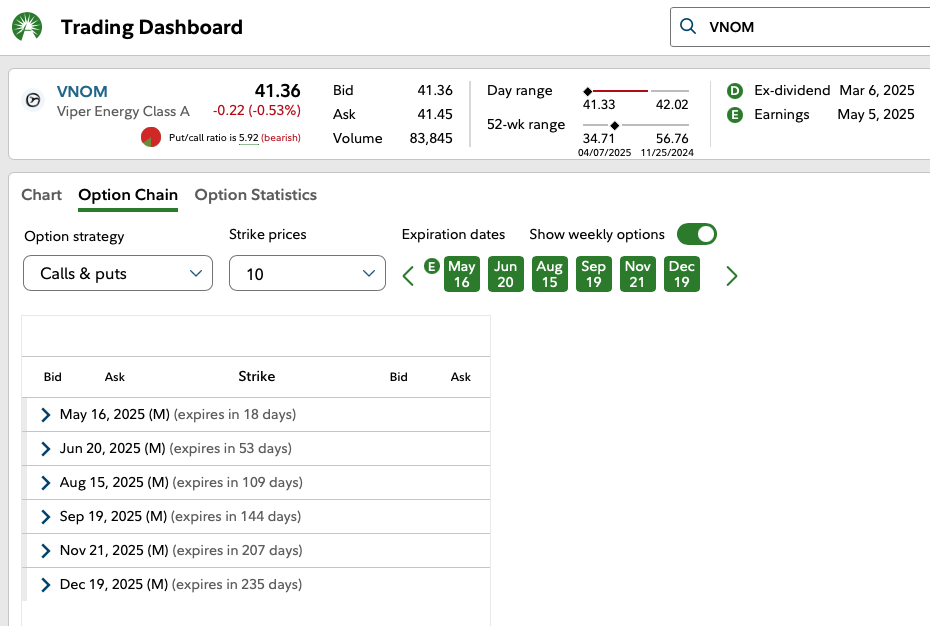

For this trade, we’re looking for a time horizon of roughly 60 to 120 days. To find the exact expiration date in this window, we navigate to what’s known as an “option chain” for VNOM shares. Here’s the snapshot of the options chain for VNOM puts in Fidelity’s Trade Dashboard:

For this trade, we’ll select the August 15, 2025, expiration – a 109-day range. Clicking the drop-down menu reveals the next component of the trade we must decide on: the strike price – the price at which the put-option seller will commit to buying shares on the date of the option expiration.

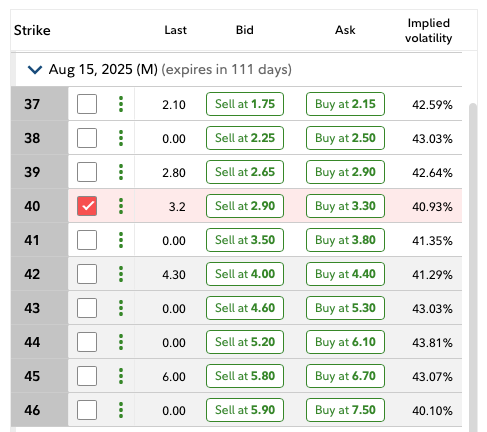

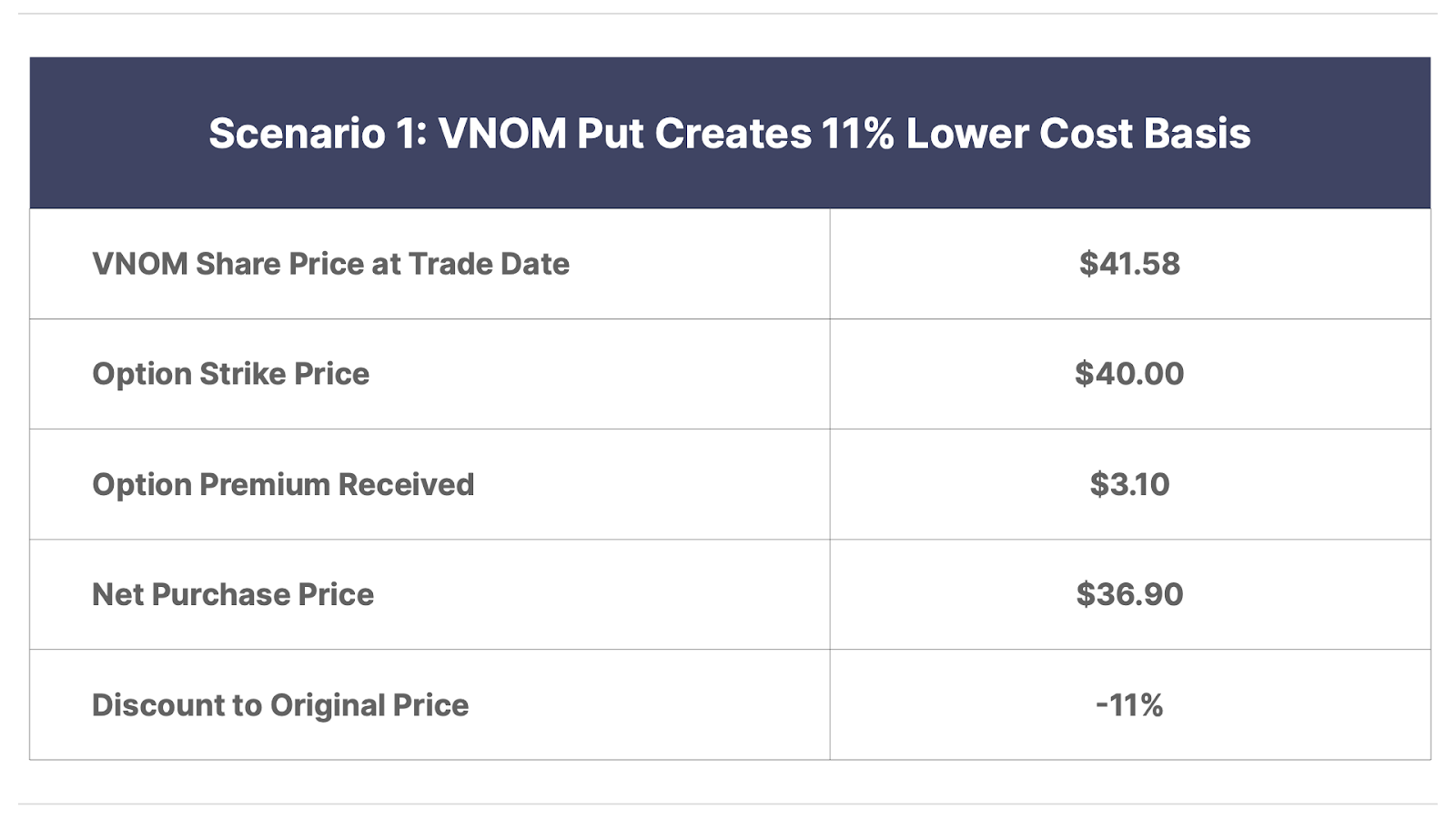

In this case, we’ll select the $40 strike price – a price we’re comfortable buying and owning shares of VNOM at for the long run. The table revealed from the drop-down menu on the August 15 expiration date shows the $40 strike put option trading at roughly $3.10 as of Friday’s closing price (taking the midpoint between the bid/ask):

The $3.10 option price represents the price you can sell puts for (as of Friday’s close) – cash you receive for assuming the risk of commiting to buy Viper shares for $40 on August 15. Note that the price of the option is quoted on a “per share” basis, but each option contract represents a commitment for 100 shares.

So each $40 put option contract represents a commitment to purchase 100 VNOM shares at $40 per share, or $4,000. This is known as the “notional value” of the contract. Likewise, the $3.10 option price will bring in $310 in cash for each put option sold (before trading fees).

This brings us to the final consideration before placing the trade: determining the number of contracts to sell. For this, we recommend sticking with the same position sizing limits or rules an investor uses when buying stocks outright.

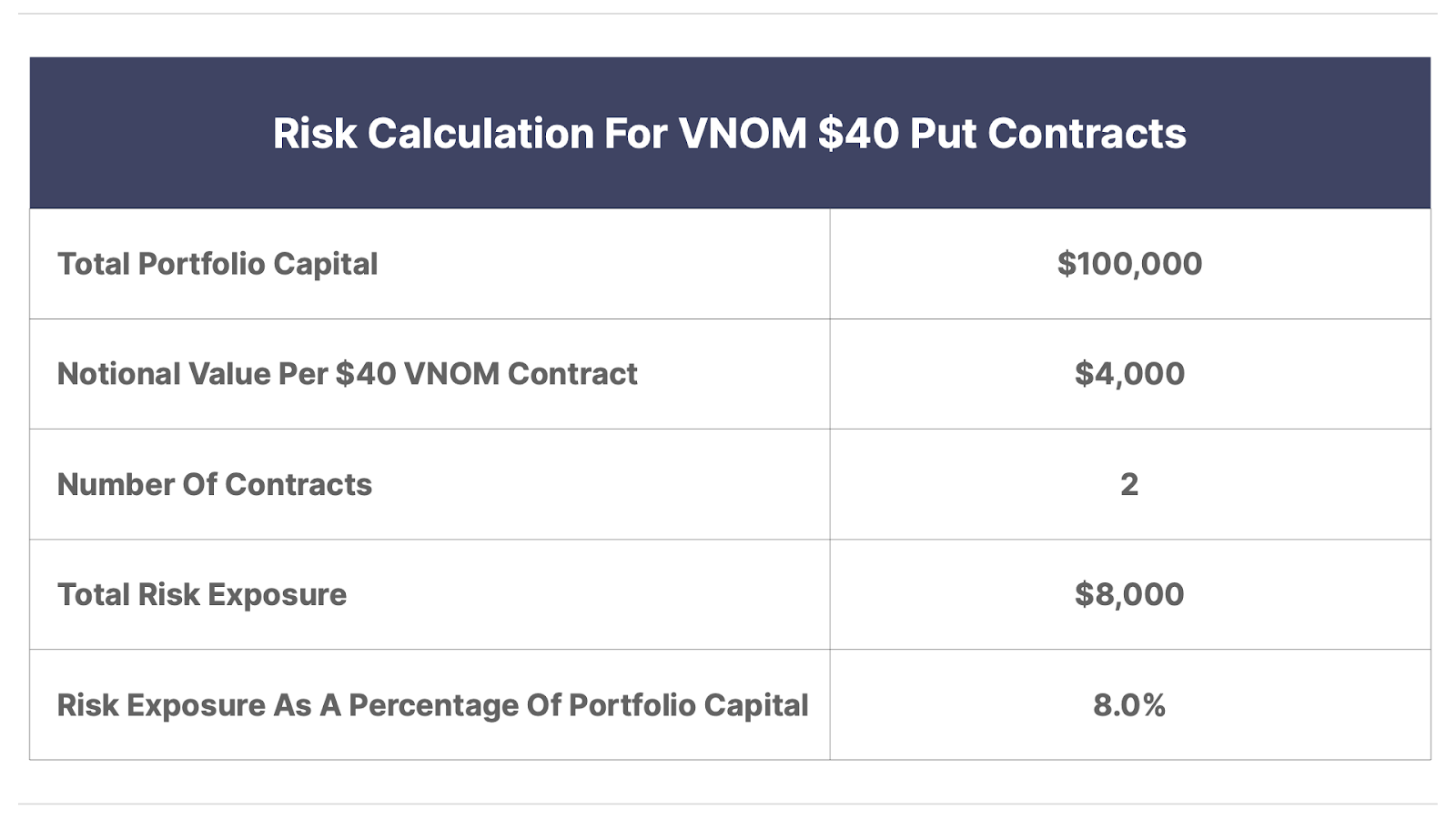

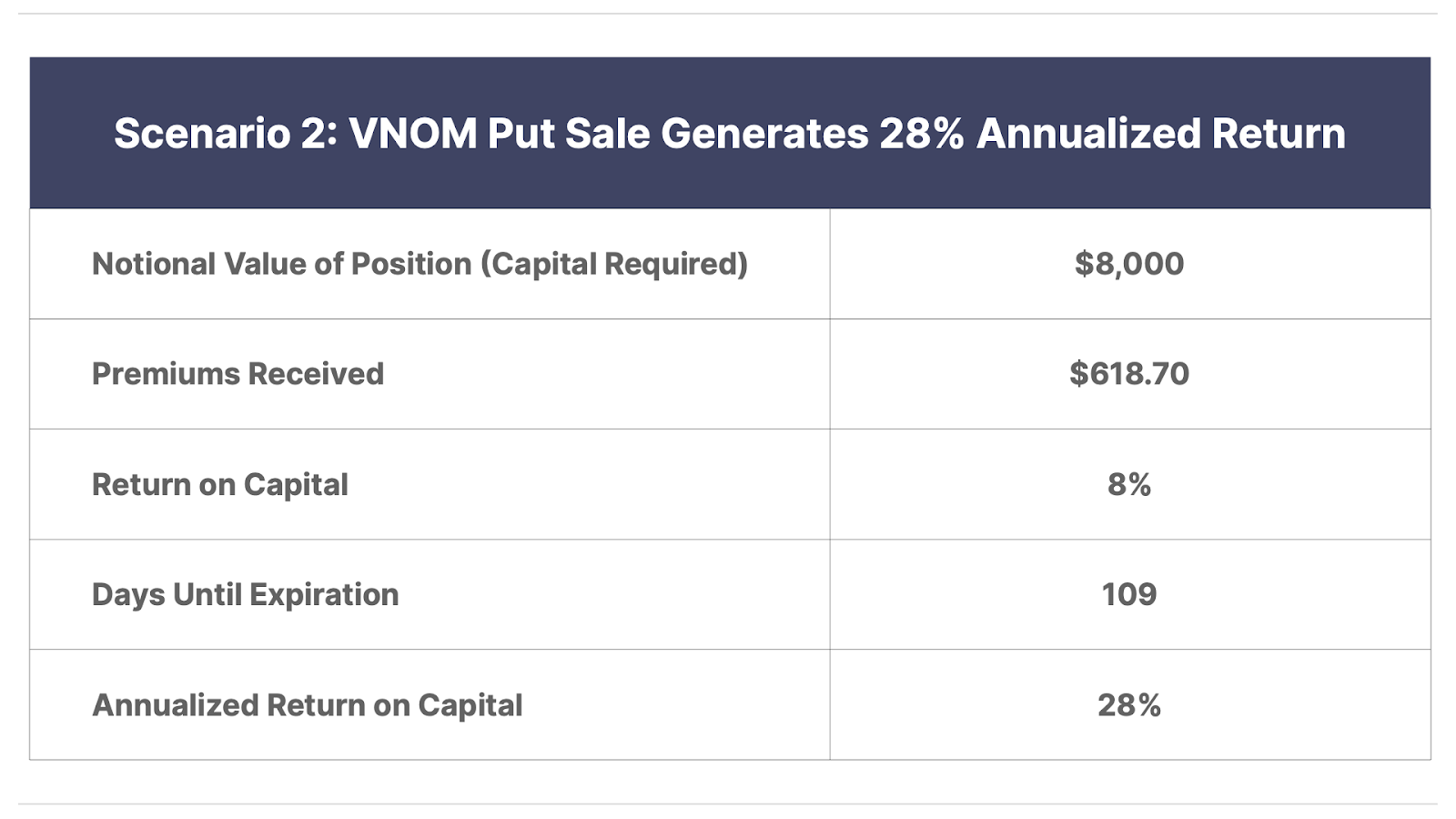

So for example, let’s imagine an investor with a $100,000 portfolio who typically puts 5% to 10% of their capital at risk in any single investment. In this case, the maximum number of $40 VNOM put contracts they should sell is two. That would represent $8,000 of risk exposure, or 8% of their total portfolio capital, as shown below:

We now have all of the key pieces of information required to place the trade, summarized below:

- Underlying stock: Viper Energy (Nasdaq: VNOM)

- Put-option expiration date: August 15, 2025

- Put-option strike price: $40

- Number of contracts: 2

To place the trade, navigate to the option-trading interface of your preferred brokerage and input each of these criteria. Here’s what this looks like in Fidelity, with all prices taken at the close of trading on Friday:

Note that making this trade will automatically result in $618.70 in cash premiums ($620 minus $1.30 in trading fees) deposited directly into your account. That cash is immediately available for reinvestment… and just like that, float is born.

After making the trade, assuming the contract is held until the August 15 expiration date, one of two things will happen:

- Shares of VNOM close below the $40 strike price, or “in the money.” In this case, the broker handling the trade will automatically replace each put option contract with 100 shares of VNOM, purchased at the $40 strike price, by the following trading day.

- Alternatively, shares of VNOM close above the $40 strike price, or “out of the money.” In this case, each put option expires worthless, and the contract disappears from your account, along with your commitment to purchase shares.

In the first scenario, where shares of VNOM close below the $40 strike price by expiration, you’ll end up owning 200 shares at $40 each. However, after factoring in the $3.10 in premiums, this reduces your net cost basis down to $36.90. That’s a discount of 11% to last Friday’s closing price, and reflects a valuation of less than 14x last year’s free cash flow, and a 6.8% dividend yield: a price we’re happy to purchase shares of Viper Energy at and hold forever.

The second scenario, where the option expires worthless, results in a net gain of $618.70 of premiums (after fees). Assuming this is a cash account and no margin is used, your broker will set aside the full notional value of the trade ($8,000) as restricted cash for the next 109 days until the option expires. Thus we measure the premiums generated relative to the capital required to make the trade, which works out to an 8% return in 109 days, or a 28% on an annualized basis:

So to conclude… in one scenario, we get to acquire one of the world’s best businesses at an even cheaper valuation multiple than its already-attractive price of 15x free cash flow. Alternatively, we earn a 28% annualized return on invested capital – on par with some of the best-performing investors of all time.

And here’s the wonderful thing: the options market offers a virtually unlimited source of these same kinds of opportunities every trading day. Even when overall volatility in the market is low, there’s a constant source of option-trading opportunities in high-quality businesses, where the share price is experiencing higher-than-normal volatility. This can come from a one-time earnings miss, a cyclical downturn in the company’s industry, or any other number of temporary setbacks that don’t impair the long-term viability of the business.

In June we will be unveiling the Porter & Co. Trading Club, where we will offer subscribers opportunities such as this one outlined today… selling puts, selling covered calls, and offering trades that include a combination of both, plus more. Additional details will come in the next few weeks.

When options and other trading methods are included in your toolkit as an investor, it opens up a steady stream of opportunities to acquire stocks at cheaper prices or generate world-class returns on invested capital.

While trading options is not as easy as clicking the buy or sell button with normal stocks, we believe it’s well worth the extra effort to add this into your investing toolkit.

What do you think – would you ever consider trading options? Let us know below:

Three Things To Know Before We Go…

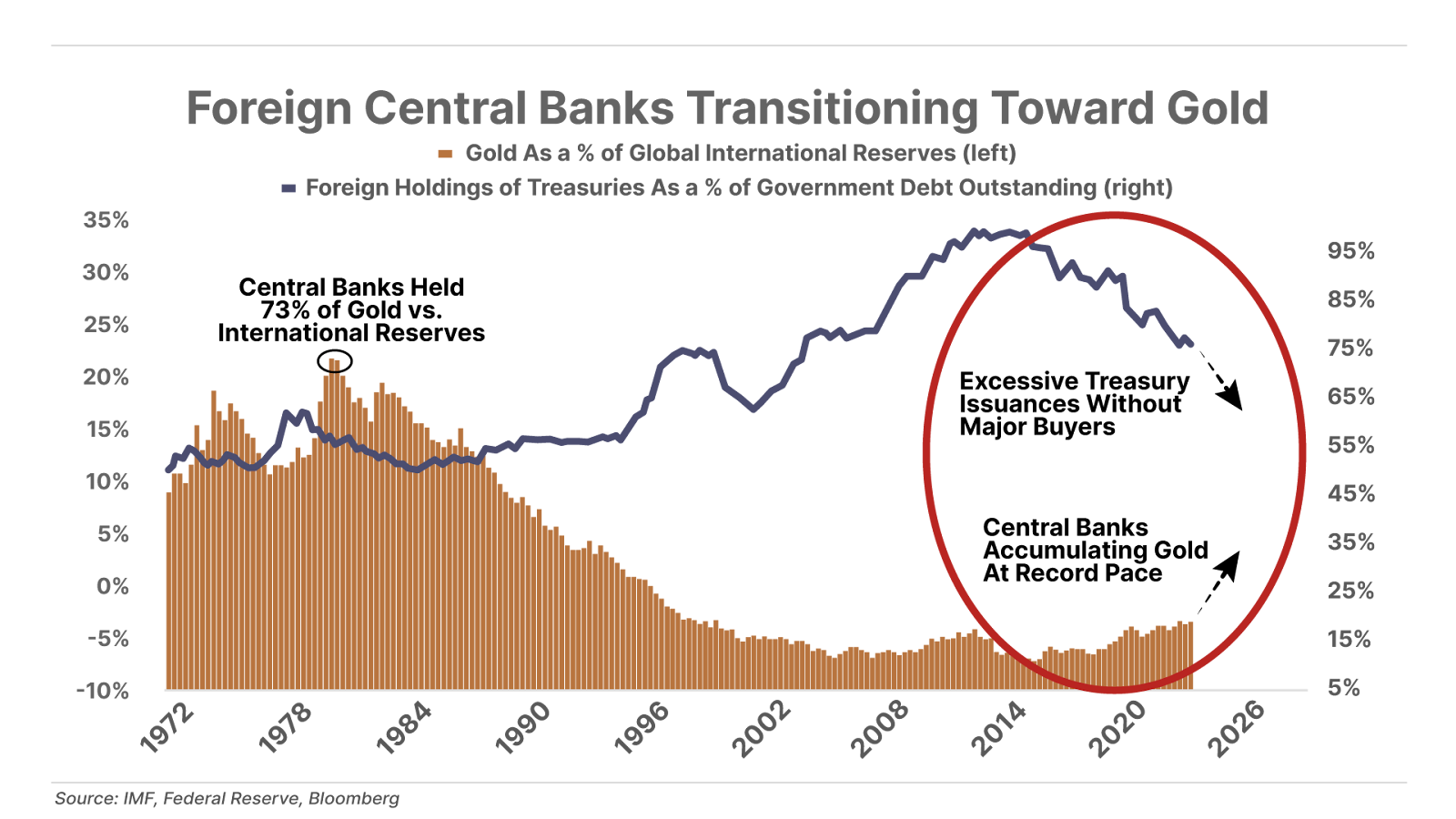

1. Foreign banks dump U.S. Treasuries. As uncertainty over President Donald Trump’s tariff policies shakes up markets, foreign-bank ownership of Treasuries has fallen to 23% – the lowest level in 22 years and down sharply from around 35% a decade ago. At the same time, central banks have been aggressively boosting their gold reserves, now at the highest levels in 26 years. The selloff in U.S. Treasuries recently triggered one of the largest two-week outflows since data tracking began in 2005. U.S. financial exceptionalism has begun unraveling – to the benefit of hard assets like gold.

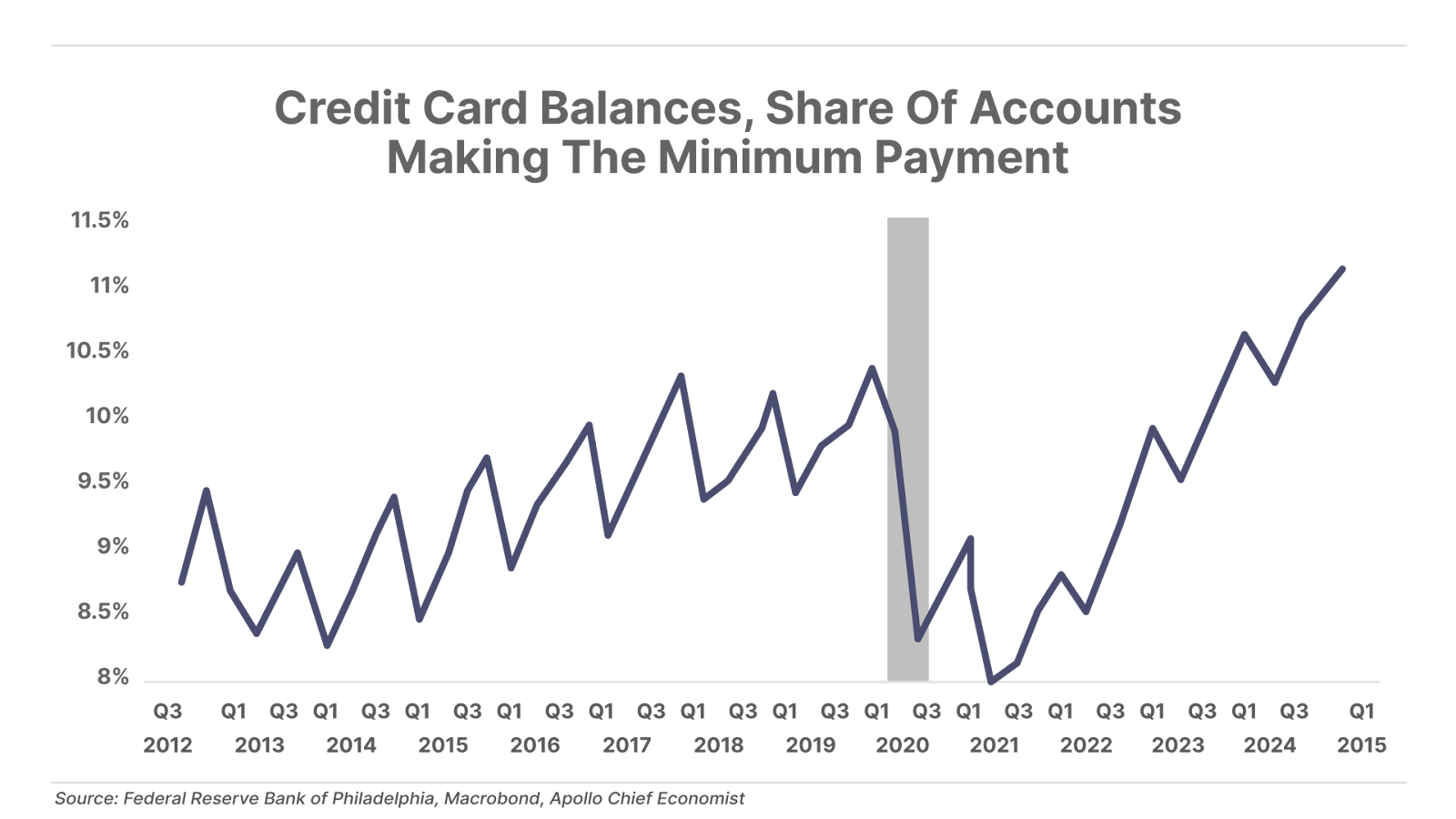

2. Consumer stress is rising. A recent survey from online loan marketplace Lending Tree found that 25% of buy now, pay later users are funding grocery purchases with these loans, nearly double the number from just one year ago. Separately, data from the Federal Reserve shows a record-high percentage of U.S. households are making only the minimum payment on their credit cards. These data points suggest a growing number of consumers are struggling to keep up with rising prices and higher interest rates, even before the full impact of tariffs takes effect.

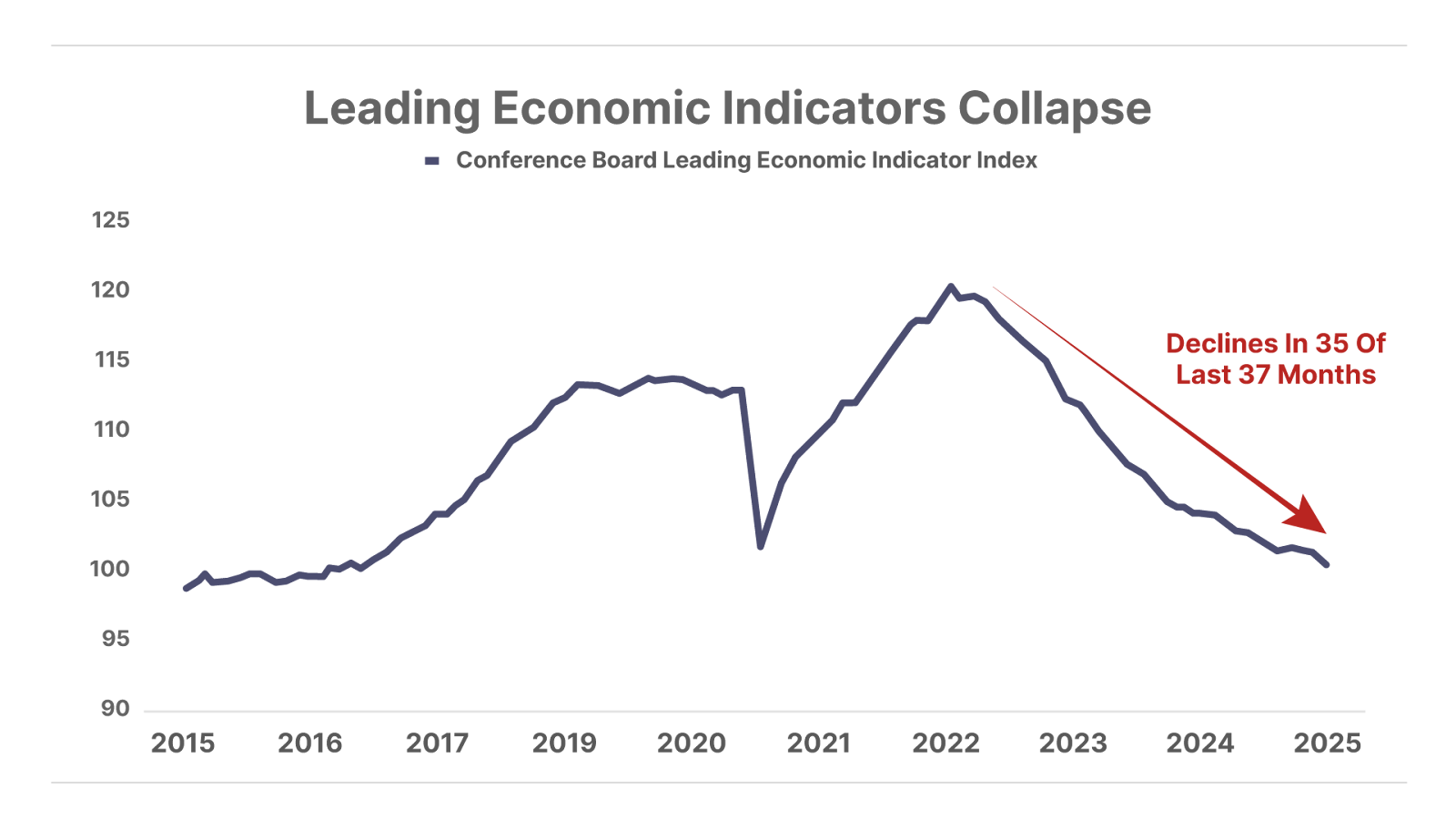

3. Leading economic indicators collapse. The Conference Board’s Leading Economic Indicators index, which contains 10 macroeconomic data series designed to anticipate future trends in economic growth, has now declined for 35 out of the last 37 months. The index is down 16% since its December 2021 peak, marking the largest drop since the Global Financial Crisis. This trend points toward a sharp slowdown in economic growth, and potentially a recession.

And One More Thing… Erez Kalir Talks Biotech On Black Label Podcast

On Friday, we released the latest episode of the Black Label Podcast – a provocative, no-holds-barred space where Porter and co-host Aaron Brabham talk about markets, politics, and life with a series of very special guests. This month’s special guest, Biotech Frontiers editor Erez Kalir, discusses what he finds curious about Trump’s policies and also what he calls “the paradox” related to biotech investing today. Plus, Erez and Porter talk about how they met… Click here to get the full podcast now.

Good investing,

Ross Hendricks

Houston, Texas

P.S. Trump Stunner: “First 4-Term President Since FDR”?

Could President Trump be heading for a FOURTH Presidential Term?

Former Presidential Advisor, Jim Rickards, says, “I know this may sound crazy. But if Trump runs in 2028 – as planned – it could lead to his fourth round as President.”

Whether you agree or not – this story has serious implications for the economy and the stock market.

It all ties back to a recent decision Trump made – which could hand him immense support unlike anything we’ve seen in a century.

For the full story, click here.

Mailbag

Porter, I have read you since 2019, and remember that property-and-casualty (P&C) insurance is the sector that you said you would want your kids to master.

The P&C sector is now the one I am invested in the most heavily. Thanks for the invitation to the Kinsale dinner, but would not be able to accept your invitation. I would however be very interested to know what you say there.

Alain R.”

I just wanted to say thank you for being kind enough to let us know about Kinsale Capital in the Daily Journal on Wednesday. I had never heard of it before.

I looked into the company and decided to buy a few shares. I plan to use it as a compounding vehicle over the coming decade, so will be buying more regularly and on weakness.

Brendan V.”

Porter’s comment: For anyone thinking about owning shares of Kinsale Capital, you’ll want to be at our special Porter & Co. cocktail reception and dinner presentation on May 21, in Richmond, Virginia, where I’ll teach you everything I know about property-and-casualty investing. Click here to join me.

Hi Porter: I have been with you on gold during the past decade plus, enduring many barbs from long-stock-only types until 2024-2025.

What are your thoughts on silver, as the gold-silver ratio crosses 100? This ratio seems out of whack, and the question is: does it correct from a big move up in silver or a fall in gold prices?

Tom D.”

Porter’s comment: Well done!

There’s certainly a good case to be made about the price of silver following gold higher, but I don’t make that case. Why not? Because I don’t have to… I’m willing to take 400% to 500% every decade buying gold. If that’s not enough for you, then you can take more risk and buy silver.

My thinking is: gold has been a reserve asset for 4,000 years and central banks continue buying it.

I don’t see any buying silver.

Now, if they started to do so, I completely agree with you… silver would skyrocket.

But, I don’t have to make that bet.

So, I don’t.

As always tell us what you think: [email protected]

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447.