The Combination Of Trump Tariffs And The DOGE Chainsaw

Today’s Lofty Valuations Could Take A Tumble

| Editor’s note: Porter is hosting a private dinner on Monday, March 3, at one of New York’s best and most exclusive restaurants in support of his longtime close friend, Whitney Tilson, who is running for mayor of New York City. Guests are asked to make a donation at this link to help support Tilson’s campaign to make New York City “safe and sane.” Porter, who keeps an apartment in New York, will be inviting a “who’s who” list of well-known NYC investors to the dinner. The location of the restaurant will come in response to the donation. Please RSVP before the end of business Friday, February 28, to join the group. |

This is Porter & Co.’s The Big Secret on Wall Street, our flagship publication that we publish every Thursday at 4 pm ET. Once a month, we provide to our paid-up subscribers a full report on a stock recommendation, and also a monthly extensive review of the current portfolio, as we share below… At the end of this week’s issue, paid-up subscribers can find our Top 3 “Best Buys,” three current portfolio picks that are at an attractive buy price. You can go here to see the full portfolio of The Big Secret.

Every week in The Big Secret, we provide analysis for non-paid subscribers. If you’re not yet a paid subscriber, to access the full paid issue, the portfolio, and all of our Big Secret insights and recommendations, please click here.

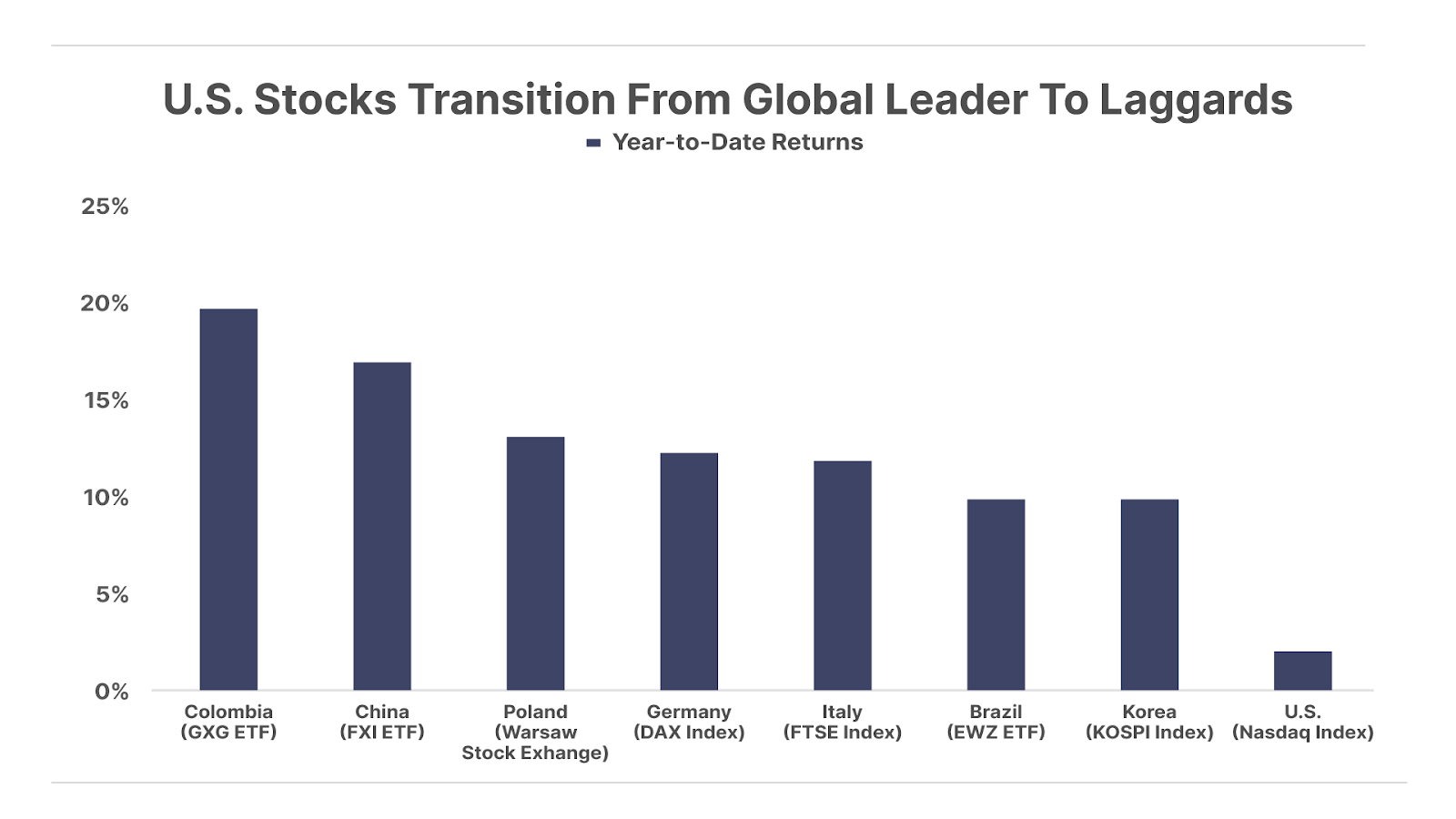

Over the first two months of 2025, the market has shifted away from the major investment theme that has dominated the past few years. That is the “U.S. exceptionalism” trade, whereby U.S. asset prices have soared while foreign stock markets remain depressed. This market dynamic has reversed to start the year, with foreign stock markets surging ahead of the lackluster returns in U.S. stocks:

This emerging trend goes against the consensus opinion following the election of President Donald Trump last November, which contended that the business-friendly administration would continue boosting the prospects of U.S. stocks over their foreign counterparts.

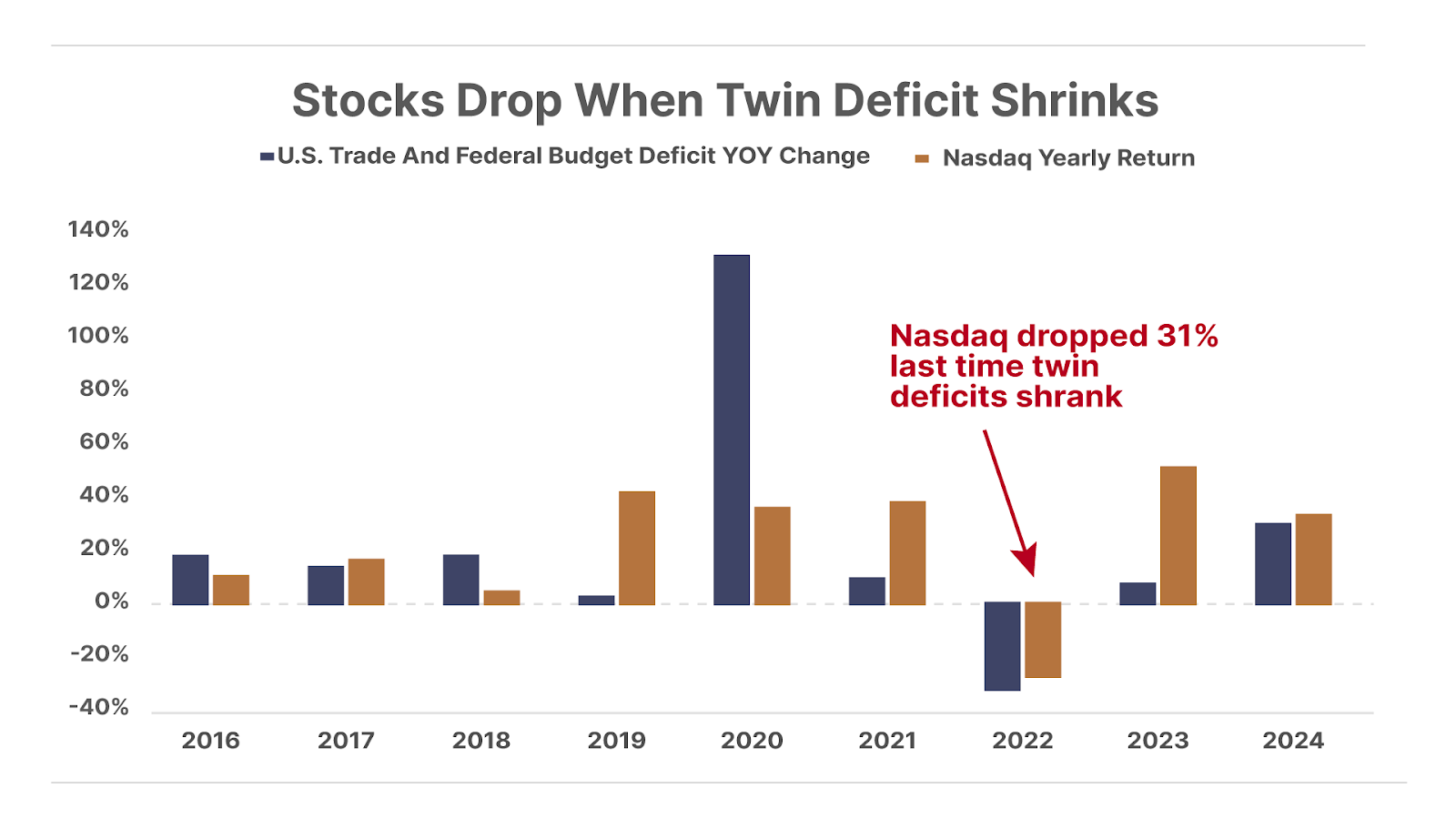

We see two key reasons why this could be just the start of the unwind of the American exceptionalism trade, at least in the near term: the coming decline in the U.S. trade deficit and ever-expanding federal government budget deficits. Together, they are known as the “twin deficit.”

The rapid expansion in the twin deficit has been a major driver of the inflation in U.S. asset prices. This inflationary process starts with America borrowing money, and then spending that money to acquire imported goods from its overseas trading partners. Those foreign trading partners then recycle the cash they receive back into U.S. asset prices. That’s the secret to how America turns newly printed money into an influx of cheap imports and a skyrocketing stock market. And when this virtuous cycle reverses, so too do U.S. asset prices.

The chart below shows this relationship in action, by comparing the change in the twin deficit with the yearly change in the Nasdaq Composite Index. Notice that in years when the U.S.’s twin deficit increases, stock prices rise. And the only year (2022) in the recent past when the twin deficit shrank, U.S. stock prices posted their largest decline since 2008:

The problem for American asset prices is that the Trump administration is looking to shrink both America’s trade deficit with the world and its own federal budget deficits. While this could be good for the U.S. economy over the long term, it could cause the sky-high prices of U.S. stocks to tumble in the near term.

In terms of the federal budget deficit, the biggest shock could come from Elon Musk and his Department of Government Efficiency (“DOGE”) taking a chainsaw to the U.S. federal budget deficit.

In just six weeks since Trump has taken office, over 200,000 federal workers have been laid off, and he’s only just begun, with some forecasts suggesting that the number could climb to 300,000 in the weeks ahead.

The ripple effects could spread far and wide. The Apollo Investment Group estimates that every federal employee released could lead to the loss of two private-sector jobs… as each federal job loss takes two supporting contractor roles down with it. So the estimated 300,000 federal workers cut could ultimately result in nearly 1 million total layoffs.

And with President Trump recently calling on Elon Musk to “get more aggressive” on spending cuts, it seems likely that the budget deficit could shrink, which it hasn’t done since 2022 (again, a year when stocks tumbled). Slashing the bloated bureaucracy of Washington, D.C. will likely be bullish for the long-term health of the U.S. economy. However, as with every economic restructuring, the short-term effect of a million job losses will lead to less spending and slower economic growth.

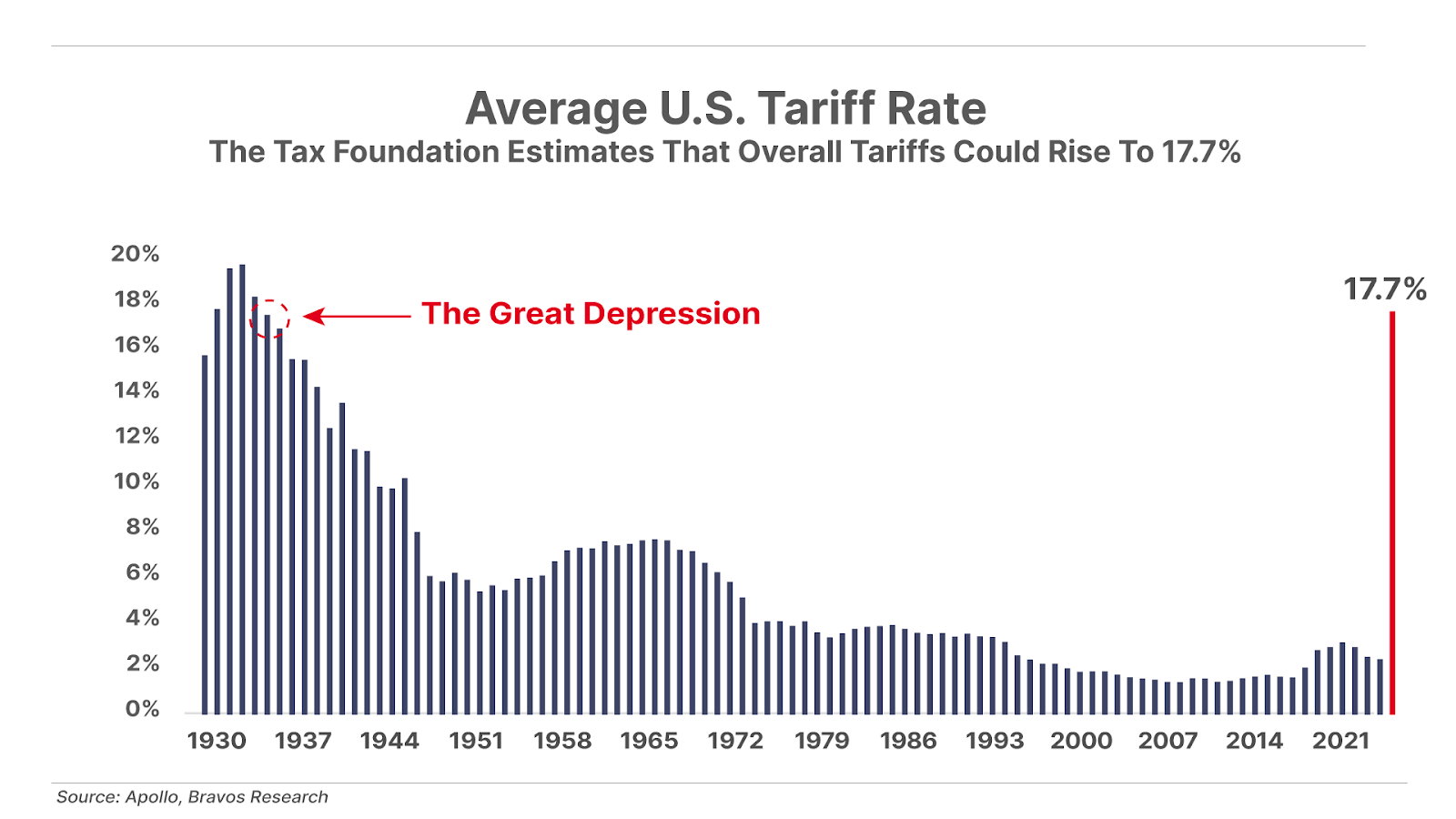

Meanwhile, the threat of new trade tariffs risks disrupting the virtuous cycle of America borrowing money to buy cheap foreign goods, and then having the proceeds flow back into U.S. asset prices. The Tax Foundation think tank recently estimated that tariff rates will rise to nearly 18%, which would be the highest level since the Great Depression:

While Trump hopes these tariffs will usher in a U.S. manufacturing renaissance by making foreign imports more expensive, history suggests a very different outcome. The U.S. economy has thrived in the post-World War II era when trade tariffs steadily fell, creating a thriving global trading environment that gave rise to an abundance of low-cost foreign goods. Reversing this process might encourage U.S. companies to build more factories domestically, but this will come at the cost of significantly higher prices for all Americans. We recently detailed the devastating effects of tariffs on the global economy, which you can read here.

As we explain in that report, tariffs are simply another form of taxation that shows up in the form of higher consumer prices. Legendary Wall Street trader Steve Cohen recently said as much at an investment conference last week:

Tariffs cannot be positive. It’s a tax. And you can imagine tit-for-tat if the U.S. implements a tax on somebody, they’re going to perhaps raise the stakes and raise their tax back.”

Cohen’s Point72 Asset Management family office has ranked among the top hedge fund performers in recent years thanks to his bullish stance on U.S. markets. However, he noted at last week’s conference that he’s shifted to a bearish stance due to the confluence of risks from tariffs and a sharp reduction in government spending:

I’m actually pretty negative for the first time in a while. It may only last a year or so, but it’s definitely a period where I think the best gains have been had and wouldn’t surprise me to see a significant correction.”

The Trump tariffs couldn’t come at a worse time, with inflation moving higher. The consumer price index (“CPI”) reading for January came in at a 3% annualized rate, the highest pace in 18 months, and well ahead of expectations.

And consumers aren’t happy about it. The University of Michigan consumer sentiment index dropped nearly 10 points to a 15-month low of 64.7 in February. The top concern among surveyed households was persistent inflation continuing to erode their purchasing power. The survey data revealed that consumer inflation expectations over the next year jumped to 4.3%, up a full percentage point from the 3.3% year-ahead inflation expectations from last month. Perhaps even more concerning, the five-year inflation expectations rose to 3.5%, or the highest level of the last 30 years.

This is a big problem for the Federal Reserve. The longer that inflation remains high, the more high-inflation expectations become entrenched in consumers’ minds – a key factor that fueled the 1970s inflationary outbreak, which caused a lost decade for the U.S. economy.

Even before tariffs risk sending consumer prices higher, pinched consumers have pulled back on spending. The signs of a tapped-out consumer are showing up in the earnings reports of U.S. consumer businesses, ranging from quick-service restaurants like McDonald’s (MCD) and Starbucks (SBUX) to snack makers like Hershey (HSY) and PepsiCo (PEP). Now, this weakness is showing up in the broader macroeconomic data, including overall U.S. retail sales, which plunged by 0.9% in January for the largest monthly decline in two years.

The downbeat consumer is even starting to impact business at discount retailer Walmart (WMT), which until recently was a big winner from stretched household budgets, as six-figure earners traded down. But Walmart’s latest Q4 earnings report indicated that even these high earners might have exhausted their spending power, when the company issued 2025 sales guidance that fell short of Wall Street’s expectations, sending shares down by double digits. This followed a lackluster Q4 earnings report from McDonald’s, which posted its largest sales drop since the pandemic.

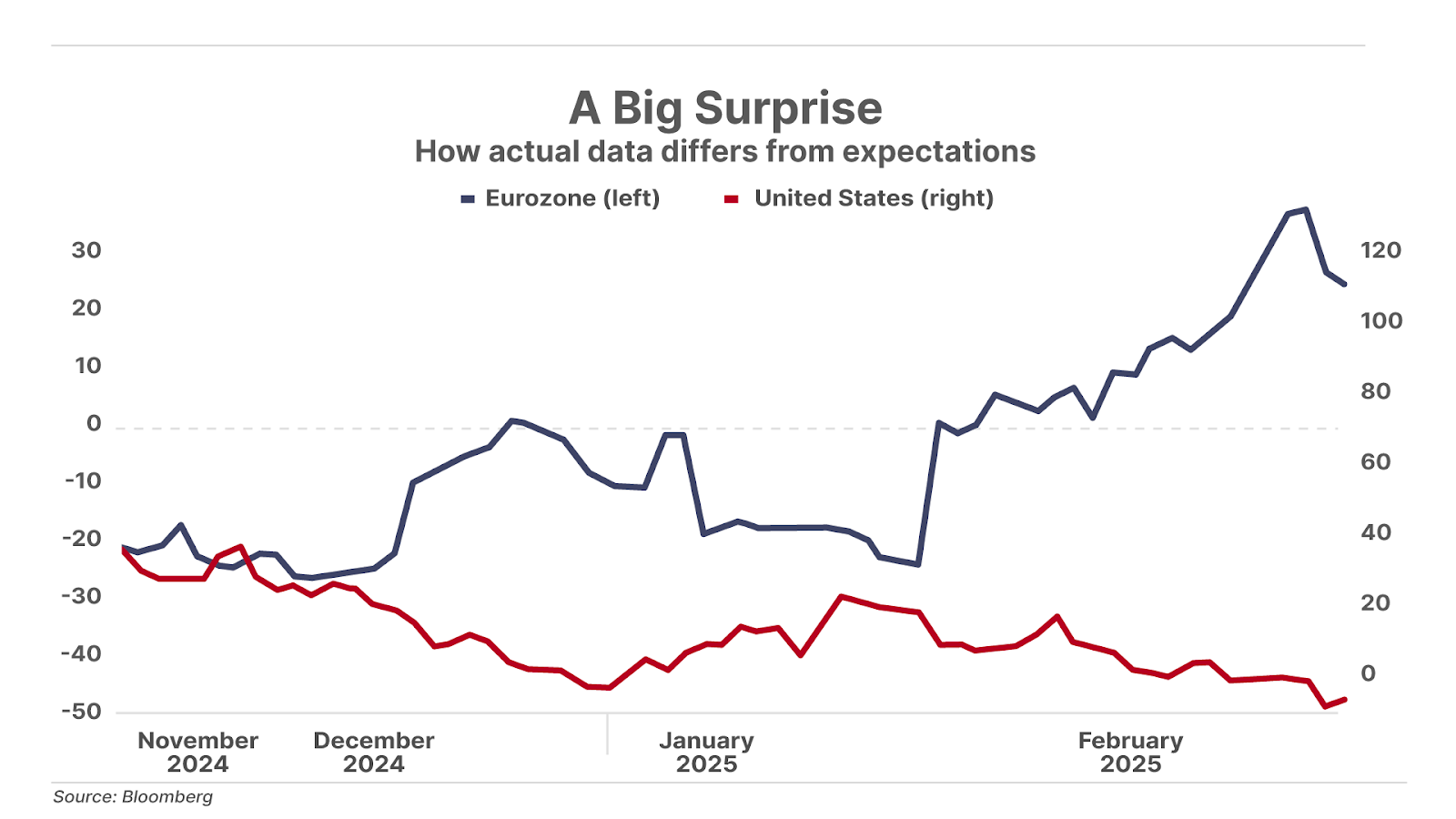

Consumers struggling to afford Walmart or McDonald’s bodes poorly for the rest of the economy. Ever since the peak of U.S. growth optimism following Trump’s election, the economic data has come in weaker than expected, as measured by the Citi Economic Surprise Index, which measures incoming economic data relative to market expectations.

The chart below shows the index peaking at +43 (with data coming in above expectations) shortly after Trump’s election. It has since moved to -8, as more economic data are coming in below expectations. At the same time, foreign economies are showing the opposite trend of improving economic surprises. This includes the Citi Economic Surprise Index for the Eurozone, which has recovered from -20 to +22 over the same period:

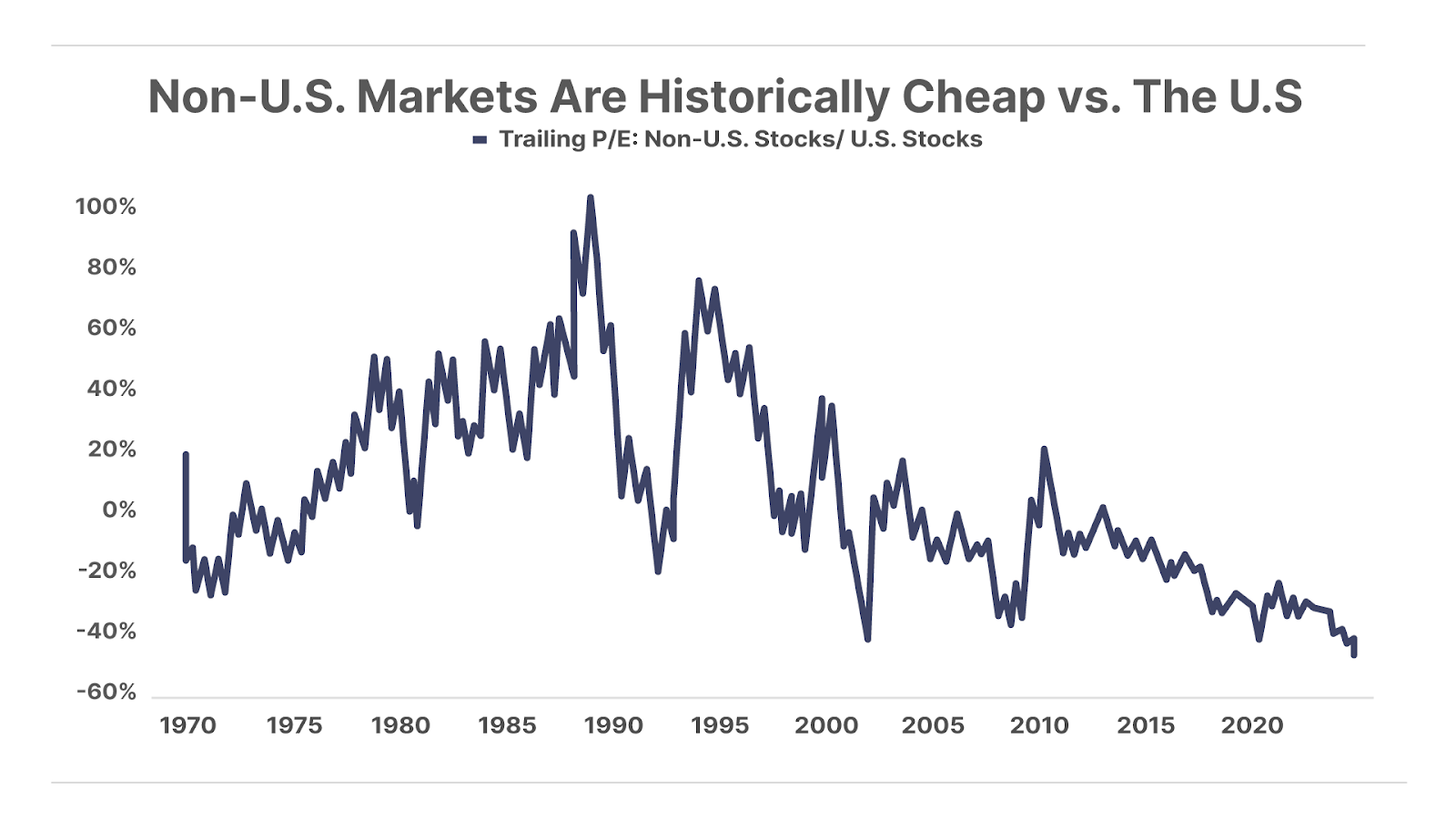

Meanwhile, even as the growth outlook for the rest of the world improves relative to the U.S., investors have priced U.S. stocks at near-record high valuations, while leaving foreign stocks for dead. The chart below shows the valuation spread between U.S. and non-U.S. stocks falling to a discount of 46%, or the cheapest relative valuation of non-U.S. stocks going back to 1970:

The bottom line: There is a growing risk of U.S. economic and earnings growth coming in below the lofty expectations currently priced into the U.S. stock market. We have noted for the past two years growing consumer weakness, and now, the Trump administration’s trade and fiscal policies will likely add further pressure on the U.S. economy. Specifically, Trump’s policies aimed at narrowing America’s twin deficit – even if positive for America in the long run – will come with the side effect of reversing the flow of both capital and consumer goods into the U.S. economy that has boosted economic growth and stock prices in recent years.

Thus, investors in the U.S. stock market should exercise extreme caution and maintain a healthy cash position in order to buy U.S. stocks at lower valuations when the excessive optimism about the American exceptionalism trade shifts to fear.

In the meantime, there are many U.S. and international companies already in The Big Secret On Wall Street that we believe will thrive in this environment.

In this issue, we’re reviewing several of these businesses. This includes an update on one of our latest “Best Buy” recommendations, where we explain why this business can thrive regardless of new trade tariffs, and a company that can capitalize on the improving growth rates in overseas markets.

We’ll also dive into one of our favorite foreign stock holdings, which owns a portfolio of world-class brands that dominates its market. The shares have been beaten down on overblown fears of the death of a vice that humans have indulged in for thousands of years, giving investors the chance to buy at a decade-low valuation.

Plus, we provide an update on the shares of a fast-food chain that recently sold off on slower-than-expected growth, even though it remains one of the fastest growing large-scale food chains in the world. We also provide an update on the bonds of a beaten-down commodity producer that’s weathering a deep bear market in prices of one of the world’s most critical elements.

Finally, we cover the latest results from an up-and-coming consumer brand that’s in the midst of recovering from a growth slump. We make the case for a breakout year for this company, driven by its rapid expansion into international markets plus a recent acquisition that will cement its status as the fastest growing new entrant into a highly profitable industry.

This content is only available for paid members.

If you are interested in joining Porter & Co. either click the button below now or call our Customer Care team at 888-610-8895.