Issue #23, Volume #2

“The fault, dear Brutus, is not in our stars, but in ourselves.”

– William Shakespeare, Julius Caesar, Act I, Scene II

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| Most people should never buy stocks… If there were such a man as Mr. On Average, he’d be a heck of an investor! But there’s not.… However, there is an asset class that is much better than stocks… You will never buy a stock again… Inflation stays sticky – in Japan and in the U.S… |

After working with investors for nearly three decades, I’ve reached a surprising conclusion:

Most people shouldn’t ever buy stocks.

I don’t mean they shouldn’t buy individual stocks. I mean, they shouldn’t own stocks, at all, of any kind, period.

They shouldn’t own stock mutual funds.

Or ETFs (exchange traded funds).

Or even index funds.

Yes, I am quite aware that, over time, common stocks will produce returns that are superior to every other asset class… on average.

Your focus should be on those last two words, “on average.”

If there were, in fact, a Mr. On Average, he’d be a heck of an investor! But there’s no such man.

And there’s a lot of sin hiding behind the myth of Mr. On Average.

Like many of life’s contests, the stock market is designed to look like a fair game, where everyone has a fair chance to win. And, in fact, because of tremendous gains to productivity and the resulting growth in corporate earnings over time, all investors win over time – on average.

And yet, in reality, for most people, the stock market is a rigged game that they cannot win.

That’s not because the stock market is a criminal conspiracy. It is because life is not fair – that’s the way God designed it.

Virtually all outcomes in nature are driven by “power law” dynamics. Vilfredo Pareto (say that 10 times fast!) was an Italian polymath. He studied engineering at the University of Turin in the 1860s, but later became a professor of economics at the University of Lausanne, in Switzerland. His most famous work was an 1896 study of land ownership across Europe, which revealed that about 20% of the people in each country owned about 80% of the land. He later discovered this same kind of distribution across all kinds of natural phenomena, like by counting peas in his garden. He found that 80% of all the peas came from only 20% of the pods. In 1916, he wrote The Mind and Society, a book that explained how there’s a naturally occurring elite across all of nature – a kind of hidden order to the world.

We find these “Pareto’s Law” effects across the financial markets.

It turns out that about 7% of all listed stocks capture more than 90% of all the returns. These “power law” winners end up generating virtually all of Mr. On Average’s results.

Brad Barber and Terrance Odean studied 66,465 individual investor accounts, at a large discount brokerage firm across five years in the 1990s. They published their findings in The Journal Of Finance (April 2000) in an article that pretty much summed up their conclusions: “Trading Is Hazardous To Your Wealth.”

In their study, the authors found that “on average” investors made 18% a year in stocks (it was a bull market!). But of course, there was no actual Mr. On Average. Instead, there were people who traded a lot… and people who traded a little. And all of the positive returns were in the 20% cohort that traded the least.

The people who traded the most actually lost 6.5% per year, even though stocks “on average” had gone up almost 20% a year!

John Coates’ 2012 book The Hour Between Dog And Wolf cites trader data showing top performers (10%-20%) account for 80-90% of profits in hedge funds and on trading desks.

So, yes, some people make a lot of money with stocks. But most people do very poorly, especially if they are active investors.

Even in mutual funds, which are generally held for the long term, you’ll find plenty of evidence that most people do poorly in stocks.

The seminal study on actual mutual fund investor returns is DALBAR’s Quantitative Analysis Of Investor Behavior (“QAIB”).

DALBAR is a Boston-based analytics company that’s been around a long time – it was founded in 1976. It produces high-quality research for the financial industry, including its most famous study, the QAIB, which has been running for 30 years.

The QAIB study shows investors’ actual returns don’t come close to matching the funds’ returns they invest in because of irrational behavior, namely, buying high and selling low. Actual returns for individuals – on average – are less than 6% a year, despite average fund results of almost 10%. And, once again, trust me, the “average” mutual fund doesn’t exist. A few funds perform very well. Most don’t. And Mr. On Average mutual fund investor doesn’t exist either.

Most individuals, even when they buy mutual funds, will lose money in stocks.

Trust me, no one else involved in finance will ever tell you that very unpleasant truth. And, if you doubt me, then I challenge you to go ask your best local accountant how many of his clients that invest in stocks make money doing so. The answer: about 20%. Most of the people (80%) lose money or do very poorly.

There’s a simple explanation for all of this:

#1. Most people do not understand how risky individual stocks are. Rather than buying the proven winners, they take on huge risks when they buy new or emerging businesses in an effort to find the one company (out of thousands) that will be the “next” Amazon (AMZN) or Microsoft (MSFT). Meanwhile, the actual next Amazon and Microsoft are: Amazon and Microsoft!

#2. Most people (virtually everyone) that claims to be a “buy-and-hold investor” is actually a “buy-and-fold investor.” They love to brag about the stocks they own – none of which were purchased and held for longer than the five-to-seven-year average market cycle, because: they always sell at the bottom.

#3. The more stocks you buy, the worse your odds. That’s simply math: most stocks lose money over time. Ergo, the more times you roll those dice, the worse your odds become.

So… what should you do?

What if I told you there was a far better way to invest? It’s a way I’m 100% sure will lead to vastly better outcomes for virtually everyone.

In fact, it is virtually impossible not to make market-beating returns in these assets because they are so easy to understand.

Plus, this is an asset class that’s far, far larger than the stock market.

And, unlike stocks, these investments are made through binding legal contracts that have a firm value.

You don’t have to figure out what these things are worth. There’s a simple price tag.

And, here’s the very best part. These investments are actually guaranteed by law. Once you invest in these assets, you are guaranteed specific payments, at specific times, and you are guaranteed a total return on your investment, typically over a three-to-four-year period.

There are a few wrinkles, though.

First, there’s not nearly as much liquidity in these markets. And although some investors see this as a flaw, it’s actually a good feature. This will make it hard for you to trade, which makes it more likely that you’ll hold long enough to earn the high total returns that are possible.

Second, nobody is going to show you how to do this kind of investing. Think about that for a second. Why do you think there’s a huge industry that exists to “help you” buy stocks? If you’ve been at the poker game for an hour and you still don’t know who the patsy is, you’re the patsy.

And here’s the final wrinkle.

This is, almost entirely, a professional’s market. Very few individual investors are involved in this asset, mostly because none of them know anything about how to buy these assets. Most people know how to buy a stock. Most people know how to buy real estate. People even know how to buy cryptos! But nobody knows how to buy these.

Again, there’s a reason for that. Nobody ever talks about these assets on TV because the biggest institutions and the wealthiest investors in the world want to keep these incredible assets all for themselves.

But, on Friday, I’m going to teach you everything you need to know about these assets, including how and when to buy them.

And, after you see what you’ve been missing, I promise: you will never buy a stock again.

Three Things To Know Before We Go…

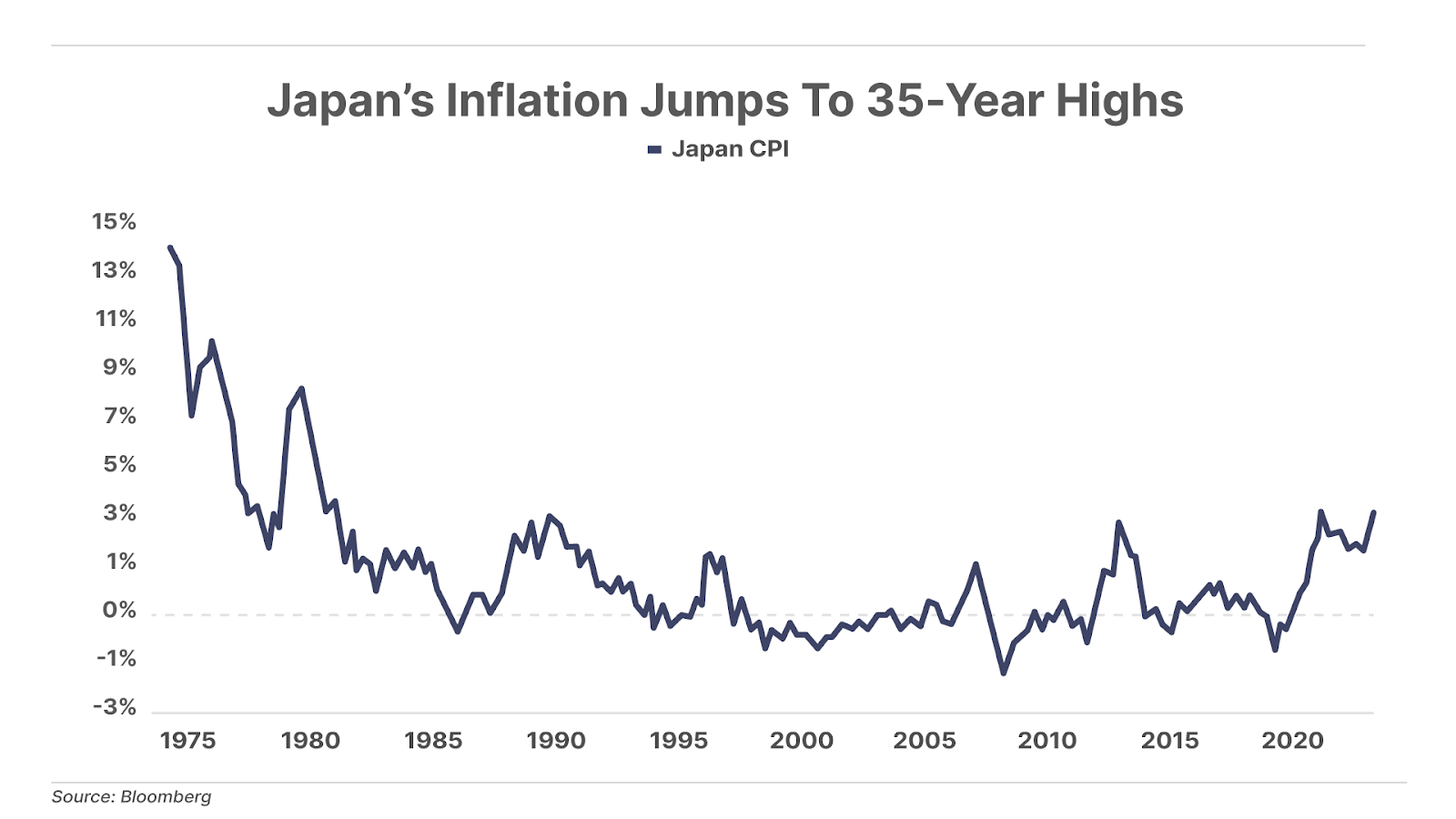

1. Stagflation risk in Japan. Inflation in Japan jumped to 4.0% in January, hitting levels only reached one other time in the last 35 years. Meanwhile, economic growth there slowed to 0.1% in 2024, just above recessionary levels, and a marked slowdown from the 1.5% growth in 2023. With inflation stuck for 34 consecutive months above the Bank of Japan’s 2% target, and economic growth stalling out, the Japanese economy risks a period of stagflation (stagnant economic growth and sticky inflation).

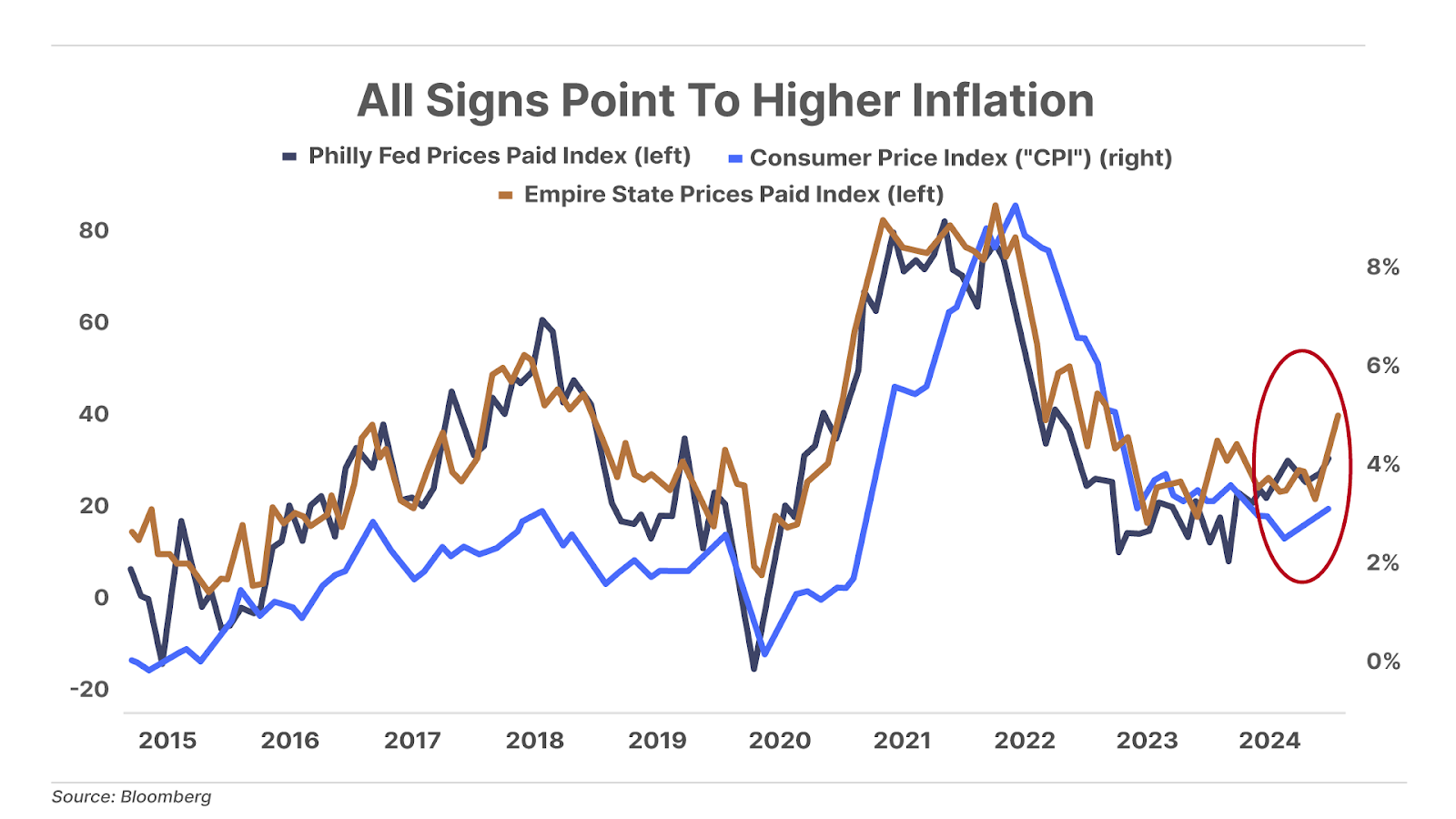

2. More troubling inflationary signals in the U.S. As we wait for Friday’s report on the personal consumption expenditures (“PCE”) price index, we’re already seeing signs that higher prices are likely in the months ahead. Two recent regional surveys – the Philadelphia Fed Manufacturing Business Outlook Survey and the New York Fed Empire State Manufacturing Survey – both showed that manufacturing costs moved sharply higher in February. As shown below, these indicators suggest headline consumer price inflation could rise back above 4% over the next several months.

3. Little to cheer about at Home Depot. Mr. Market applauded Home Depot’s (HD) Q4 earnings released yesterday – pushing shares up 3% – but stagnant sales and declining earnings in 2025 suggest the rally may be short-lived. Home Depot’s same-store sales (“SSS”) declined in eight consecutive quarters, but rose in Q4 2024 with modest SSS growth of 0.8%. SSS are expected to grow by just 1% in 2025, while overall revenue is projected to rise by 2.8%. However, when adjusted for inflation (running at 3%), this represents no growth at all, and the company anticipates a 3% drop in earnings for the year. Because of continued high interest rates, demand for home improvement has waned, as projects that might’ve been financed a decade ago are too expensive today.

And one more thing… Mason Sexton Visits The Black Label Podcast

Yesterday we released the latest Porter & Co. Black Label Podcast – Porter and co-host Aaron Brabham welcomed financial analyst Mason Sexton (this month’s Porter & Co. Spotlight guest) to the show. Mason takes a different approach than most financial analysts… he shared some key dates for dramatic market changes ahead, discussed how moon cycles give insights about the future, and he revealed a big prediction for President Donald Trump this April. Watch the latest episode here.

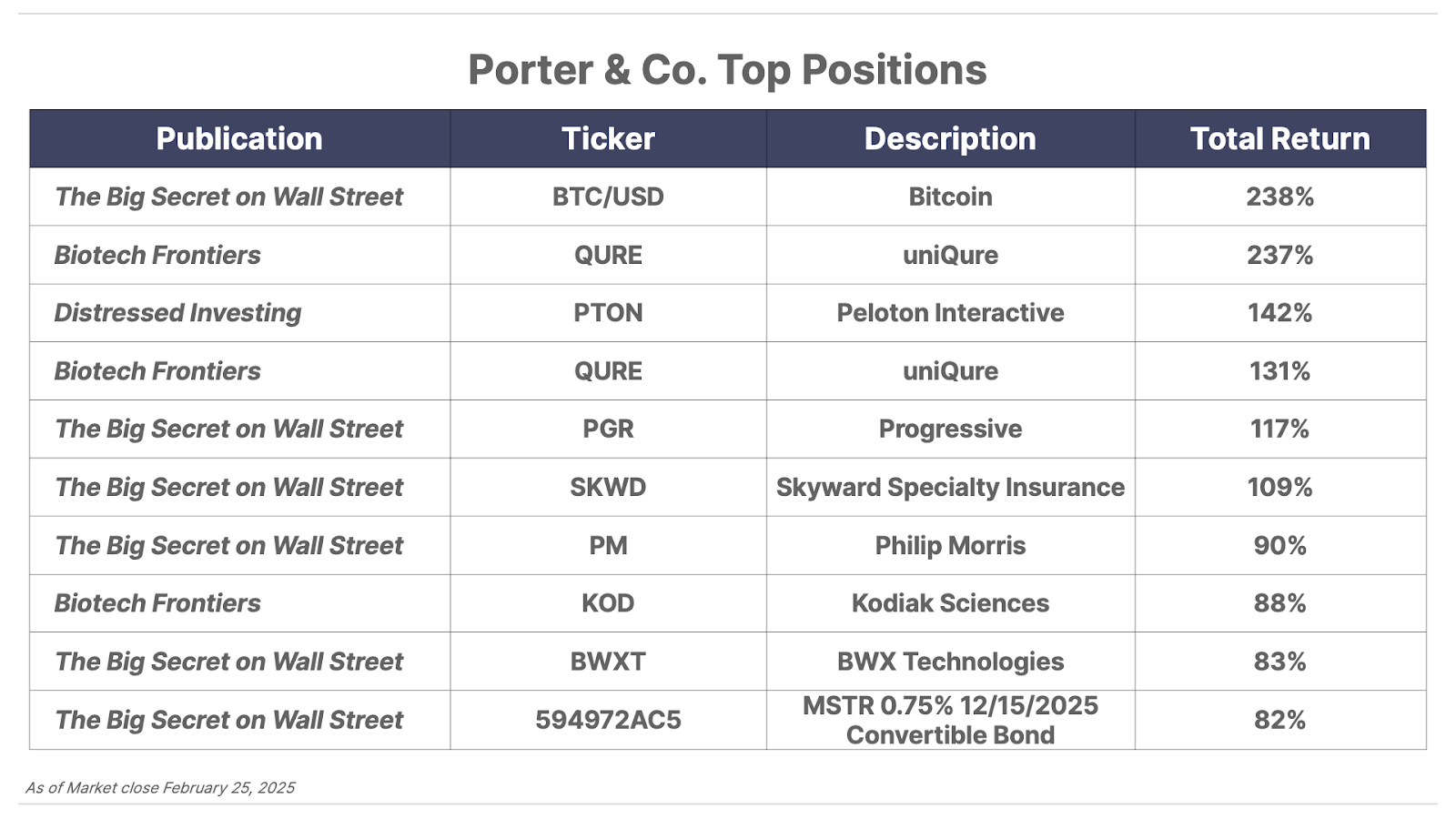

And also… Welcome To The Top 10, Philip Morris!

Even though most stocks are a lousy investment, there are exceptions… In every issue of Porter’s Daily Journal, we publish the 10 best-performing positions in the portfolios of our different publications (see below). And recently, a new name appeared on the list – one of Porter’s all-time favorite stocks, nicotine brand Philip Morris International (PM).

Investors in the original Philip Morris turned every $1 invested into around $2.6 million from 1925 until today, a 16% annual compound return for almost 100 years. No other business even comes close to generating so much wealth.

We’ve been recommending Philip Morris to our subscribers almost since day one of Porter & Co. In September, we asked Daily Journal readers which stock, Philip Morris or Magnificent-7 darling chipmaker Nvidia (NVDA), would perform better over the following decade, and 71% of respondents chose PM… and so far, they’re right: Since then, PM shares are up 24%… and Nvidia, 13% (the S&P 500 is up 8.6%).

And please, tell us what you think: [email protected]

Good investing,

Porter Stansberry

Stevenson, MD

P.S. Nostradamus was one of a kind.

And in the realm of technology, George Gilder is a modern-day prophet in the same vein.

He’s predicted everything from the rise of the microchip to personal computers, iPhones, Netflix, cryptocurrencies, and more – often years before anyone else.

I’ve been following his work for close to 30 years… and he’s had an extraordinary impact on my life. (Having George speak at our Porter & Co. conference was one of the greatest thrills of my life… very rarely do your heroes turn out to be even more incredible when you meet them!…)

When I was in my early 20s, George helped shape my understanding of supply-side economics… the inherent morality of capitalism…and the dangers of collectivism.

He also helped lay many of the foundations for my first newsletter, as it was his research that opened my eyes to the inevitable dominance of the internet.

George has the incredible ability to envision what the world will look like five, 10, and even 20 years down the line… and being so close to the mark it’s uncanny.

When I want to know where the world is going, George Gilder is one of the first I turn to.

Which is why, when George shared his latest prediction with me – what he calls “The $59 billion ‘New You’ Revolution” – I asked if I could pass it along to my readers.

It’s a breakthrough new technology that George believes has the potential to revolutionize medicine more than antibiotics, X-rays, and anesthesia… combined.

Here at Porter & Co., we’re not in the business of predicting the future. Frequent readers know that we mostly focus on identifying world-class “forever” companies that are overlooked or undervalued.

And we also know that intelligent speculation about the future, especially in the tech field, can deliver phenomenal returns (see my 1990s recommendations of Amazon, Adobe, Texas Instruments, and others).

And like I said, there is nobody better at seeing the future than George Gilder.

George’s presentation is here… you won’t be disappointed.