Issue #22, Volume #2

Avoid Asset-Heavy Investments

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| Warren Buffett’s worst investment and his best investment… 40% returns for 25 years – possibly the greatest single investment ever… Tariffs are coming, and they could be huge… Apple making a big bet on U.S. manufacturing, at a cost… |

Warren Buffett’s best investment ever wasn’t Apple.

On Saturday morning, I jumped out of bed like a kid on Christmas. It was the day Buffett had to “raise his skirt” and show the world what’s happening inside Berkshire Hathaway (BRK), which has become the world’s most important financial holding company.

I studied both his letter to shareholders and then the entire annual report, looking for details on Berkshire’s wholly owned subsidiaries. (Later that day, I met live with our Partner Pass members to share my findings. If you’re a Partner Pass member, click here to view that live presentation.)

Most investors still think of Berkshire as being a kind of “closed end” fund, where Buffett runs an insurance company and simply invests in stocks and bonds with the excess capital.

And that’s true – in part.

But, since around the year 2000, Berkshire has, more and more, invested huge amounts of capital directly in wholly owned businesses. These investments are much harder for outsiders to track. And Buffett’s track record in these large acquisitions is far from good.

Let me show you what I mean by describing Berkshire in some detail.

Today, with $614 billion in equity, Berkshire has more than 50% of its equity sitting in cash ($311 billion). The size of these cash holdings will be a huge drag on earnings, relative to Berkshire’s equity, if good investment opportunities don’t materialize quickly. (Buffett clearly thinks a crash is coming.)

However, Berkshire still owns $270 billion in equity securities, with about 80% of that capital invested into just seven companies: American Express (AXP), Apple (AAPL), Bank of America (BAC), Coca-Cola (KO), Chevron (CVX), Occidental Petroleum (OXY), and Kraft Heinz (KHC).

Now, wait a minute, Porter! You just told us that Berkshire isn’t just an insurance company and a stock portfolio anymore, but when you add up the cash ($311 billion) and the securities ($270 billion) you end up with $581 billion… which is 94% of Berkshire’s equity.

So, Berkshire is (94%) just an insurance company and an investment portfolio, right?

Nope.

The entire magic of Berkshire is that it funds its investments with “float” from its insurance companies.

Berkshire currently holds $174 billion (!) of insurance float – the money customers pay in premiums. These assets are technically liabilities. In reality, of course, these insurance premiums have been paid and must be available to be paid out in claims. But because premiums continue to grow, and because Berkshire’s underwriting is sound, the funds perform like a constantly growing account.

Since 1967, when Berkshire entered the insurance business, its float has grown at more than 20% a year.

In addition to this capital, insurance companies also legally defer taxes until policies are deemed “earned,” which provides Berkshire with another $150 billion (!) in tax float.

When you do all the math, and you include goodwill and other assets, and then you subtract all of the liabilities (like insurance and tax float)… you end up with around $350 billion in equity held in the insurance and portfolio side of the business, or a little more than half (57%) of Berkshire’s equity.

These assets provide excellent returns, in excess of 40% a year.

So, why is Berkshire’s overall return on equity (18%) so low?

The trouble with Berkshire has been its private investments, which now make up more than 40% of its equity.

Let me show you where most of the trouble resides: Berkshire Hathaway Energy (“BHE”).

Over the past 25 years, Berkshire has invested almost $100 billion into highly regulated energy companies, with a deliberate focus on wind and solar generation.

Keep in mind, that’s more money, in total, than it has made on its Apple stock. And so far, these energy investments have been, by far, the worst in Buffett’s long career.

Here are the numbers.

- MidAmerican Energy (2000): Berkshire acquired a 76% stake for $1.24 billion in equity (total deal $9 billion, including $7 billion debt assumed by MidAmerican)

- Northern Natural Gas (2002): Acquired from Dynegy for $1.9 billion ($950 million cash, $950 million debt assumed)

- PacifiCorp (2005): Acquired from ScottishPower for $5.1 billion cash, plus $4.3 billion debt assumed

- Kern River Gas Transmission (2006): Acquired for $960 million, all-cash deal

- NV Energy (2013): Acquired for $5.6 billion cash, plus $4.5 billion debt assumed

- Metalogic (2013): An oil and gas pipeline services company, acquired for $5.4 billion, all-cash deal

- AltaLink (BHE Canada, 2014): Acquired for C$3.24 billion (~US$2.9 billion at 2014 exchange rates, all-cash deal)

- Incremental ownership (2000-2022): Over time, Berkshire continued to buy out minority partners from various acquisitions, spending roughly $2 billion between 2000 and 2022.

- Greg Abel’s 1% stake (2022): $870 million cash

- Walter Scott’s 8% stake (2024): $2.37 billion cash plus $600 million note plus 1.6 million BRK.B shares ($737 million at October 2024 prices), total ~$3.71 billion.

In addition to these massive investments, Berkshire has also purchased billions in windmills, solar panels, and other capital projects ($49 billion).

Obviously, BHE paid for some of these capital projects with its own retained earnings ($36 billion), but those earnings couldn’t cover the entire cost of these projects.

I estimate Berkshire itself contributed at least another $12 billion for these capital investments.

When you add up all these numbers, it comes to $40 billion – just in equity, not including the total capital in these businesses ($236 billion).

And what have the returns on this equity been? Abysmal.

Buffett recently bought out his last partner in BHE (Walter Scott’s estate). The deal closed last October and valued BHE at roughly $48 billion. So… after 25 years… and after making seven major deals… Berkshire has seen its equity grow from $40 billion to $48 billion.

It would have done better in Treasury bills.

Let’s compare those numbers to the best investment Berkshire has ever made. And no, Berkshire’s best-ever investment wasn’t Apple.

In total, Berkshire invested $41 billion into Apple. It has received around $5 billion in dividends and it has been selling shares since 2020, with most of the sales occurring in 2024.

Total proceeds: $131 billion.

The remaining value of Berkshire’s 300 million shares is roughly $66 billion.

Total return: $162 billion (almost 4x initial investment).

Or, roughly, 30% a year.

Certainly not a bad outcome, but far from Berkshire’s best-ever investment.

(If you ever want to win a bet at a party, use this story. Not one investor in 10,000 will know the answer to this question.)

Berkshire’s best-ever investment was its $200 million purchase of Dun & Bradstreet (DNB) common stock, which occurred between 1996 and 1997. Berkshire paid around $7.90 per share, buying 25.2 million shares.

What, you’ve never heard of Dun & Bradstreet?

Given Buffett’s penchant for buying very long-lived assets, it won’t surprise you to learn that Dun & Bradstreet is one of the very oldest businesses in the United States. It was founded in 1841 as The Mercantile Agency. It has focused on owning and acquiring business data and analytics companies, doing business under a wide variety of brands, such as R.H. Donnelley.

You remember that name, don’t you? R.H. Donnelley began operations in 1886. Virtually every American over the age of 40 has used its products. Still doesn’t ring a bell? Remember the Yellow Pages? R.H. Donnelly was America’s leading publisher of Yellow Page business directories.

How did Buffett make a fortune in Yellow Pages? He didn’t.

In 1962 Dun & Bradstreet acquired another business-analytics and data business with a much more famous brand: Moody’s Investors Service. And in September 2000 (close to the peak of the famous tech bubble) Dun & Bradstreet decided to spin off Moody’s to unlock the value of the business, which investors had been ignoring because of the tech bubble. Berkshire received around 12 million Moody’s shares in the spinoff, or roughly 16% of Moody’s at the time of the spinoff. Buffett promptly sold his remaining Dun & Bradstreet shares (recouping his entire initial investment!) and bought more Moody’s shares aggressively, purchasing almost an additional $100 million worth.

Today, Berkshire still owns 13.3% of Moody’s (Buffett sold 8 million shares during the 2009 crisis). And Berkshire has received almost $500 million in dividends over the last 25 years. Berkshire’s remaining stake (24 million shares) are worth around $11 billion today (36x his investment). That’s 40% annually for 25 years – and that math ignores that Buffett got his initial $200 million back after only three years.

That’s the greatest single investment I’ve ever heard of, given the constraints that it involved a large amount of capital (over $100 million), over a long period of time (25 years) into a large and well-known business.

If you want to become a great investor, just learn from these two investments – Buffett’s worst and his best.

Things that require constantly more capital to grow (like power generation and distribution) can’t compete, over time, with things that use intangibles (brand, customer lists) to grow.

It really is that easy.

Three Things To Know Before We Go…

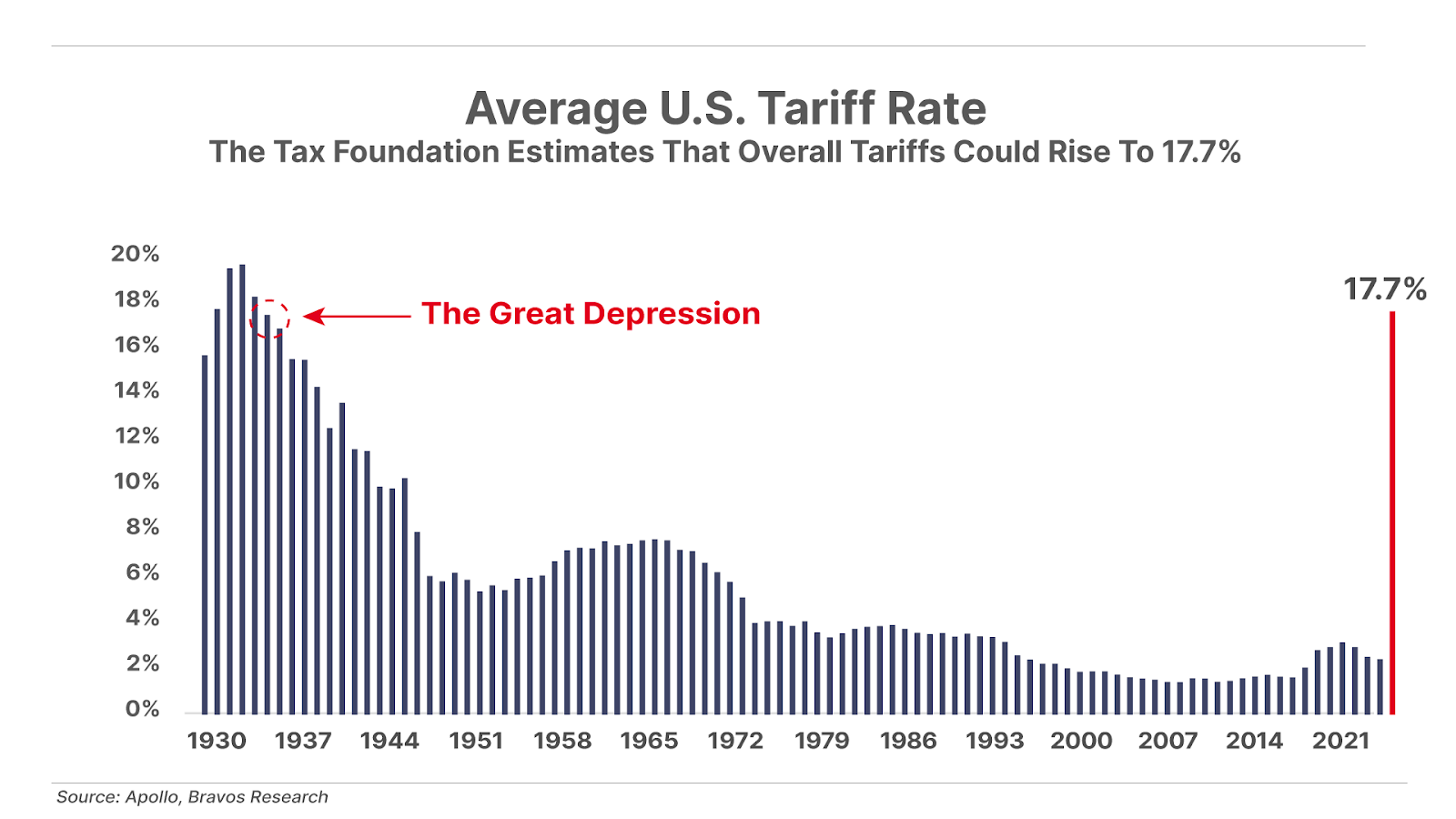

1. Trump tariff deadline with Mexico and Canada approaches. President Donald Trump’s 25% tariffs on Mexico and Canada, set to take effect on March 4, will apply to over $900 billion worth of imports, ranging from energy to automobiles, with additional tariffs on steel and aluminum to take effect on March 12. While ongoing negotiations could limit the scope of the tariffs, the Tax Foundation think tank estimates that the Trump administration will ultimately raise tariffs to nearly 18% – the highest levels since the Great Depression. As we’ve written before… tariffs are a terrible idea, and can only do damage to the American economy and consumers (how would you like to pay 18% more for… a whole lot of things you need to buy?)

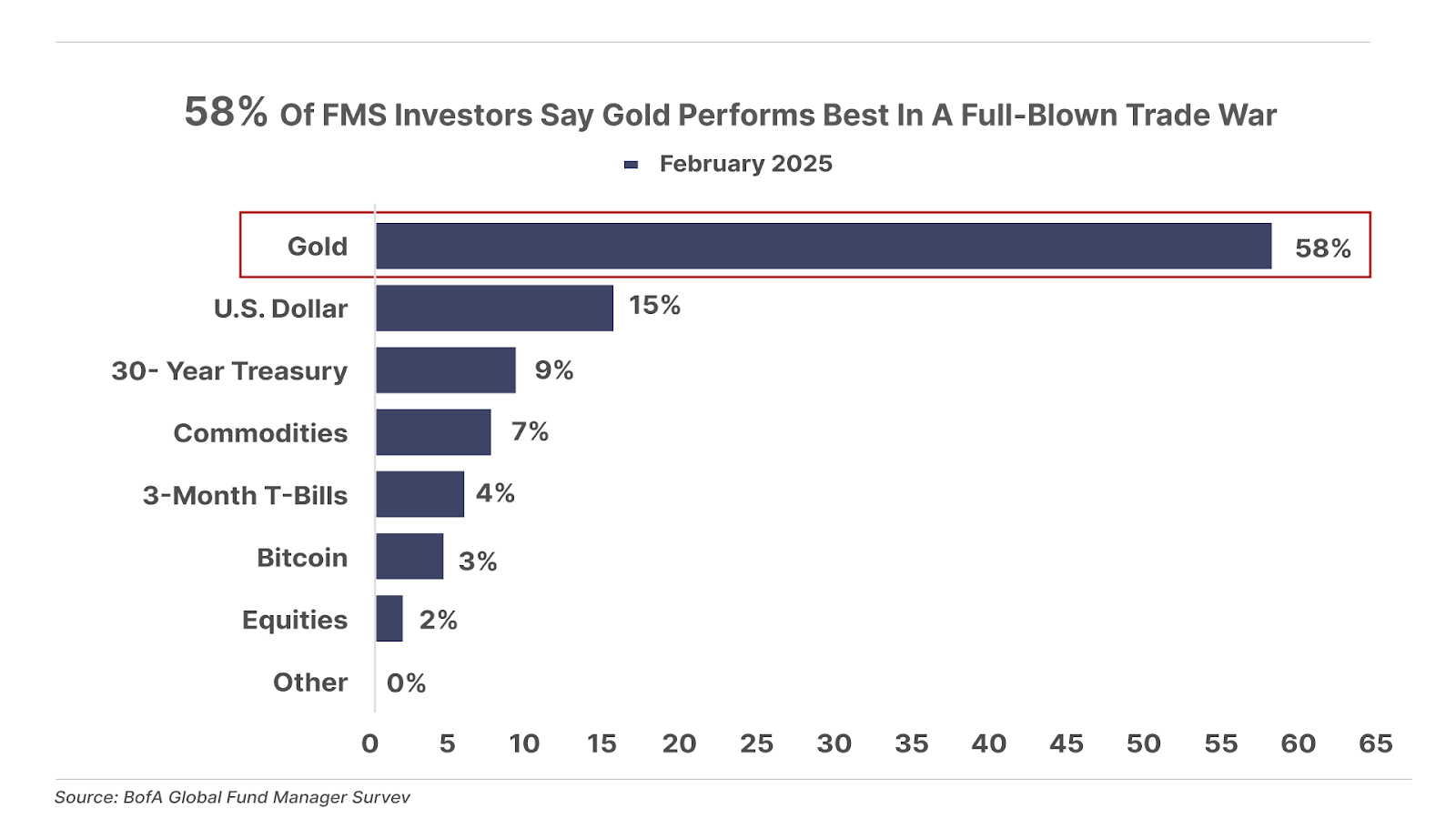

2. Gold is benefiting from trade-war fears. Gold is continuing its record rally, hitting a new intraday day high above $2,956 per ounce this morning. This is occurring despite expectations that a trade war would also lead to a stronger U.S. dollar, which would typically present a drag on gold prices. Additionally, nearly two-thirds of participants in Bank of America’s latest fund manager survey (“FMS”) believe gold is likely to continue to outperform all other assets should a full-blown trade war break out.

3. Apple’s $500 billion U.S. spending spree. Apple (AAPL) announced today it plans to invest $500 billion building new U.S.-based manufacturing and job-training facilities over the next four years. This would cause Apple’s annual capital expenditures to surge 10-fold from $10 billion to $125 billion. It would also wipe out all of Apple’s free cash flow, leaving little for future share buybacks. As we detailed last week in The Big Secret On Wall Street, Apple’s $100 billion of annual share repurchases have been the major driver of its earnings-per-share growth in recent years. We can’t help but wonder if investors will be willing to pay 35x earnings for a company with little to no earnings growth.

Poll Results… Will Buffett Outperform The S&P?

At the end of Porter’s Friday Daily Journal, in which he reviewed the performance of Berkshire Hathaway – explaining that the energy and railroad holding are hurting the company’s overall performance – we asked in our reader poll: “Do you think Warren Buffett’s Berkshire Hathaway will outperform the S&P 500 over the next five years?” And the result is resounding, with 68% of survey takers choosing “no.”

Coming up this week: The bottom line on inflation

The big number that analysts are watching this week – the January personal consumption expenditures (“PCE”) price index , the gold standard measure for inflation – is released on Friday. Both headline PCE (includes volatile food and energy prices) and core PCE (excludes them) are expected to have risen (0.3%, up from 0.2%) month over month. GDP for Q4 2024 (released Thursday) is projected to have grown by 2.3%, after a 3.1% increase in Q3.

In case you missed it…

What’s rotten about Apple (AAPL)… and what you should buy instead: Thursday’s issue of The Big Secret on Wall Street…

Porter reveals Warren Buffett’s biggest mistakes: On Saturday, Porter hosted a live webinar for Partners only, where he unpacked the latest Berkshire Hathaway shareholders letter. Partners can see the full recording here. He also devoted Friday’s Daily Journal to a review of Berkshire’s performance over the years.

Our Saturday and Sunday editions of the Daily Journal tracked the latest new stock buys and concentrated bets of some of our favorite fund managers… revealed why the government’s official inflation statistics can’t be trusted… and much more.

To subscribe to The Big Secret or become a Partner Pass member, as always, call Lance James, our Director of Customer Care, at 888-610-8895 or internationally at +1 443-815-4447, for more information on becoming a subscriber.

Good investing,

Porter Stansberry

Stevenson, MD

P.S. Mason Sexton is not everyone’s cup of tea.

His approach to market analysis is highly unorthodox. It’s extremely controversial. Here at Porter & Co. we’ve heard from people who love Mason… and from people who very clearly don’t love him.

The angle of Mason’s work is something that you’ve almost undoubtedly never seen anywhere else… even if you’ve been reading investment research for a very long time.

Whatever your opinion (and if you don’t have one, I urge you to watch this presentation), it’s difficult to argue with success. Whatever your feelings on his methodology, Mason manages to nail it. Every. Single. Time.

In other words: Mason is uncannily right, with uncanny frequency. And if you’re looking for insight on what’s happening next in markets, that’s mighty helpful.

For example… in October 1987, 11 days before it happened, Mason predicted that the stock market was about to crash.

In March 2008, called the bottom of the Global Financial Crisis crash.

And in early 2020, he warned that the top was in, and that it was time to sell… right before the Nasdaq collapsed by 36% in the COVID crash.

And now… Mason believes that something big – very big – is brewing in markets. And that it’s going to happen within the next two months.

So big… that Mason is calling it The Prophecy. He reveals in a special interview what he sees happening… when it all will start… and what you can do to prepare.

Mailbag

Readers replied to two presentations Porter put out last week regarding Warren Buffet and Berkshire Hathaway. In Friday’s Daily Journal, Porter dissected the performance of Buffett’s Berkshire holdings. He then did a live-streamed analysis in a Partners-only presentation on Saturday afternoon, reviewing Buffett’s annual letter to shareholders, which had been released earlier that morning. He made three points in the Journal, which he echoed again in the live event:

- “Since 1999, Buffett has underperformed the S&P 500 10 times on an annual basis. And that’s going to occur more and more often – no matter who is running Berkshire.”

- “Buffett has long held Malthusian ideas about population and resource scarcity.”

- “The energy assets and the railroad need to be spun off – as quickly as possible.”

The first letter is from Tim P., who writes:

Excellent insight into Warren Buffett. I was blown away to learn of his Malthusian ideas and his resulting push for abortion and poor investments in energy.

I’m adding Buffett to my list of billionaires pushing hare-brained initiatives like Bill Gates (humans need to start eating bugs, population control like Buffett, etc.) and George Soros (attempting to tear down the fabric of the country via unfettered immigration, criminal justice ‘reform,’ etc.). It’s like they lose their common sense once they get rich.

Thank you for continuing to publish insights not found anywhere else.”

Porter’s comment: The late Charlie Munger, Berkshire’s long-serving vice chair, always said, The hard part isn’t making the money. It’s staying sane.

And I can tell you, that’s true.

Thank you for taking the time today to look at Berkshire Hathaway.

I will be watching this presentation again many times.

Superb analysis, never thought about spinning off the railroad and energy business but it makes sense from a valuation standpoint as well as setting the stage for the retirement of Mr. Buffett.

John D.”

That was a great analysis on Berkshire. It really hit home for me. I worked for a very large electric utility that installed windmills. They did so because they received a very large production tax credit. Our corporate rate dropped to around 10% to 12%. The windmills could not compete on their own without the tax credits. I really enjoy your work.

Hipolito C.”

I just want to say I really enjoyed the podcast and hold roughly around $150,000 of BRK-B stock so I wasn’t sure if you were recommending selling it or holding until maybe that special dividend. I put stop losses on 90% of my stocks so not really worried about losing a lot of money on the shares as I probably made 20% a year on his stock for the last three or four years. But I do agree with you and just became a Partner Pass member and am trying to keep up with all your recommendations and material to read. Thank you.

Jeffrey F.”

Porter’s comment: As you know, we can’t give individual investment advice, but just ask yourself: Why isn’t Buffett buying his own stock?