Issue #127, Volume #2

When 30 Random Selections Outperformed The Stock Market

This is Porter’s Daily Journal, a free e-letter from Porter & Co. that provides unfiltered insights on markets, the economy, and life to help readers become better investors. It includes weekday editions and two weekend editions… and is free to all subscribers.

| When bonds outperform stocks… Any 30 bonds will do… Utilities, financials, industrials… When fund managers panic… The Day The Bull Market Dies… Buffett hoards (more) cash… Zombies come out and play… |

Editor’s note: Porter has turned today’s Journal over to Distressed Investing editor Marty Fridson.

Marty has a long background in trading, investing, and finance… Over a 25-year span with Wall Street firms including Salomon Brothers, Morgan Stanley, and Merrill Lynch, he became known for his innovative work in credit analysis. He is the author of The Little Book Of Picking Top Stocks – and as readers of his Distressed Investing advisory know, he’s also great at finding underpriced stocks.

Below, Marty serves up an analysis showing that when the market begins to panic, there is a massive supply of debt that gets sold way below their actual value – creating a rich environment for juicy returns.

Here’s Marty with the details…

Today, we’ll take a random walk through a field of distressed bonds.

Last week in the Daily Journal, I recounted how valuations of distressed debt got so far out of whack during the Global Financial Crisis that the safest of the lot – secured bonds of utility companies! – delivered a stunning 37% average return over a 12-month span. Way better and way safer than owning shares of a new technology company with wildly unpredictable earnings over that period.

But as it turns out, investors didn’t actually have to think that hard about which issues to buy. A completely random sample of 30 bonds doubled that 37% performance, returning a staggering 74% over the same period.

Here’s how I obtained that result: I used a list of bonds within the ICE BofA U.S. High Yield Index that were yielding 10 percentage points or more above U.S Treasuries on November 30, 2008. From that list I simply selected bonds #1, #11, #21, #31 and so on – not including more than one issue of any company – until I’d collected a total of 30.

Thirty is the number considered the minimum necessary for constituting a statistically valid test sample.

It was a very representative group that included Industrial, Financial, and Utility bonds. Ratings ranged from BB to CCC and the prices of the $1,000-face-value issues varied from $189 to $910.

Over the following 12 months through November 30, 2009, five (16.7%) of the bonds defaulted. Those all had negative returns, ranging from negative 27.27% to negative 93.52%. The majority of non-defaulting bonds – 13 out of the 25 – were downgraded, while only two were upgraded. Yet all of the 25 non-defaulting issues delivered highly positive total returns – big price gains on top of mostly double-digit yields – ranging from 16.48% to 533.33%.

But you might ask: wasn’t that 533.33% return a huge outlier that distorted the average? Okay, fair point, let’s leave it out. The remaining 29 bonds still averaged a not-too-shabby 57.80% return.

Of course, I’d never endorse a distressed-debt strategy based on picking bonds out of a hat. But in a 12-month period in 2008-2009, that simple-minded approach generated a bond return seven times as high as the stock market’s historical average. Just think what you might achieve with rigorous analysis of asset values, cash flows, debt covenants, and management teams!

The key point is that when distressed debt hits bottom, the odds on this famously high-risk asset class shift radically in favor of bondholders. Speculative-grade bonds, even some of the highest rated (BB), become available at prices that make improbably high aggregate returns not merely possible, but highly probable.

It’s not as if the high-yield portfolio managers don’t realize they’re selling bonds far below their true worth. After all, they got promoted to their jobs after demonstrating exceptional skill as credit analysts. But put yourself in their shoes, and suppose you’re managing a high-yield mutual fund as terrified fund holders are redeeming their shares on a massive scale. You have no choice but to sell some of these. To meet those redemptions, you have to sell bonds to raise cash.

But all the other high-yield funds are in the same situation. The only buyers are making obscenely low bids. Too bad. You have to sell.

What if no one wants to buy the troubled bonds you most want to get rid of? Tough luck. You’ll have to sell others, which have no realistic probability of defaulting anytime soon, at prices normally seen only on bonds that are flirting with bankruptcy.

There’s no certainty that the market collapse that we at Porter & Co. see on the near horizon will plunge the distressed-debt market into an abyss on the scale of what we saw in 2008-2009. But even in a run-of-the-mill cyclical bottom, the odds swing radically in favor of investors like subscribers to Distressed Investing who have two essential assets: Ready cash and the support of a research team with deep knowledge of credit analysis, bond covenants, and bankruptcy law.

This market may look unstoppable, but beneath the euphoria the same distortions Marty describes above are starting to build once again…

Insiders and big institutions are quietly heading for the exits (including Warren Buffett, as we report below)… even as retail investors keep flooding in at record levels. It’s the kind of divergence that only shows up at the end of a great speculative boom.

That’s why Marty recently sat down with Porter to create our newest broadcast, The Day The Bull Market Dies – to explain what’s really driving this split, and how the chaos that could crush thousands of U.S. businesses is creating a rare moment of opportunity for those who understand distressed assets.

He even shares his No. 1 bond to buy as the cracks under the surface grow wider. Go here to see it now.

THIS IS NOT A DRILL: Elon vs. Apple

🚨 For a limited time, you can learn how to get pre-IPO exposure to the company insiders believe could finally kill Apple’s stranglehold on wireless.

All it takes is a regular brokerage account — no Silicon Valley connection required.

The only catch? This video could vanish without warning.

👉 Watch now and get the free 4-letter ticker symbol before it’s too late.

Three Things To Know Before We Go…

1. The U.S. strikes a trade deal with China… for now. On Saturday, the White House announced that President Trump had reached a “trade and economic deal” with President Xi Jinping of China. According to the announcement, the agreement includes Chinese commitments to take “significant measures” to end the flow of fentanyl to the U.S., suspend new rare-earth export controls, suspend all retaliatory tariffs, and purchase at least 12 million metric tons of U.S. soybeans. In return, the U.S. will lower tariffs on Chinese goods by 10 percentage points and extend the expiration of certain retaliatory tariffs until November 10, 2026.

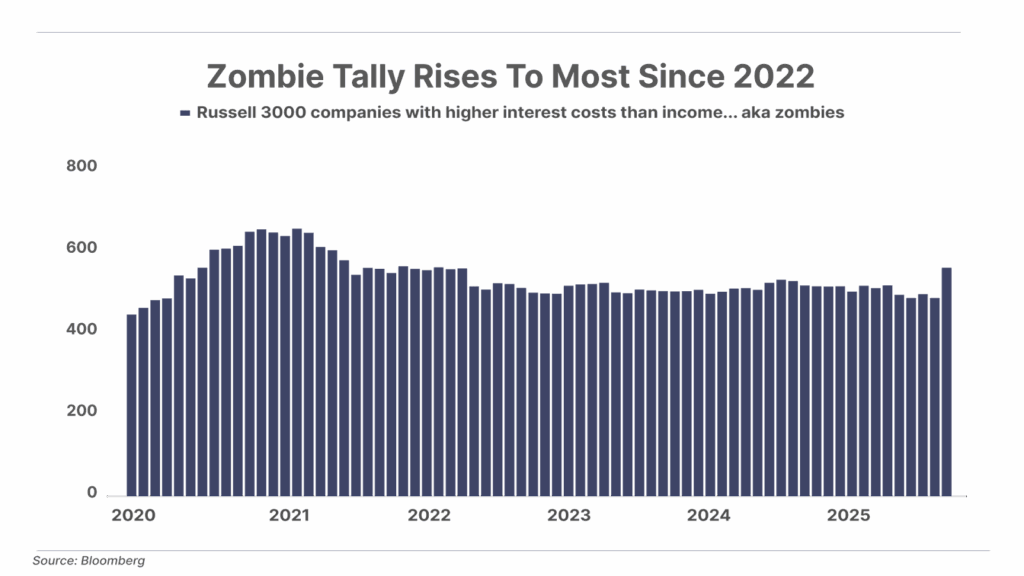

2. Zombie companies are on the rise. The number of zombie companies – firms that aren’t earning enough to cover their interest expenses – in the Russell 3000 index jumped to 639 in October – a 15% one-month surge and the highest level since 2022. Many of these companies extended their debt maturities at near-zero interest rates in the post-pandemic years, but are now getting crushed by higher funding costs and the added pressure of tariffs. Signs of financial distress are spreading.

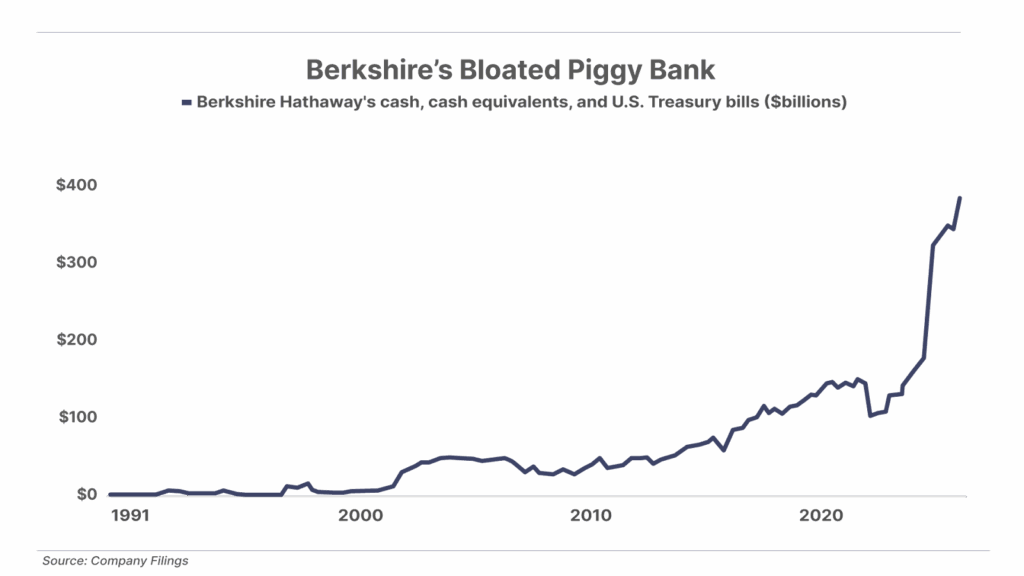

3. Berkshire continues selling stocks and raising cash. Warren Buffett’s Berkshire Hathaway released its Q3 financials over the weekend – reporting an impressive 34% increase in operating profit, driven by strong performance in its insurance business. But the thing that caught our attention was that Berkshire sold another $6.1 billion of stocks, marking the 12th consecutive quarter of net selling. This brought Berkshire’s cash pile to a new record high of $382 billion. Buffett – or his CEO successor – is poised to pounce on some deals when they emerge.

Tell us what you think of today’s Daily Journal or anything else that is on your mind: [email protected]

Good investing,

Martin Fridson

New York, New York

Please note: The investments in our “Porter & Co. Top Positions” should not be considered current recommendations. These positions are the best performers across our publications – and the securities listed may (or may not) be above the current buy-up-to price. To learn more, visit the current portfolio page of the relevant service, here. To gain access or to learn more about our current portfolios, call our Customer Care team at 888-610-8895 or internationally at +1 443-815-4447.